A timeline of the Top 15 Holdings and the 50% drawdown Test!

A timeline of the Top 15 Holdings and the 50% drawdown Test!

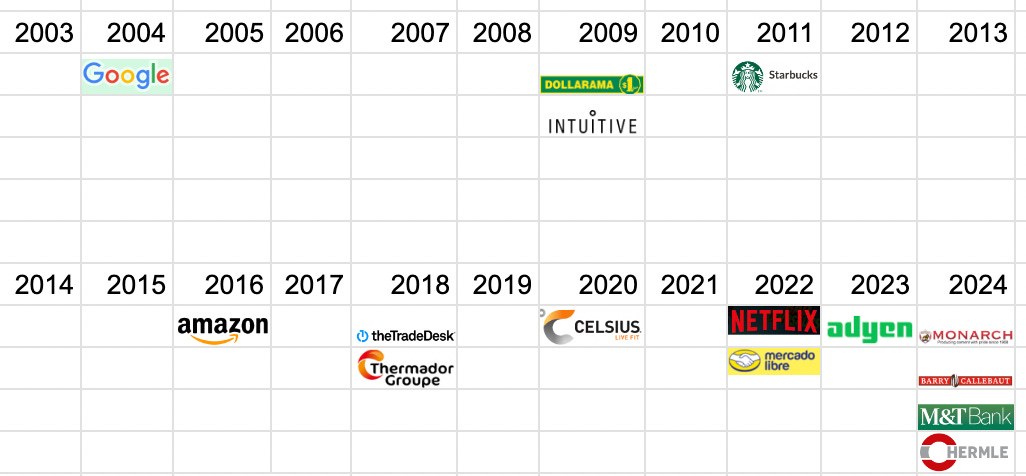

The following chart shows a timeline based on the year of acquisition of the current top 15 holdings

The following chart shows a timeline based on the year of acquisition of the my current top 15 holdings. As one can judge not many positions have survived the test of time.

The article constitutes my personal views and is for entertainment purposes only. The main goal of this article is to log my personal views. Nothing in this article or these posts in this blog should constitute an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

The 2003-2013 era:

Only 4 positions purchased prior to 2014 remain now. In the first 4 months I sold 5 positions purchased during this period (2003-2013) namely Fastenal, FDS, Nike, HIFS and Logistec. The last one was a buyout, and the first 3 were large cap compounders that had provided respectable returns. However, I believe at current price they are fairly valued or over valued and I can achieve better returns with the new positions. In the case of HIFS, clearly the company lacks the ability to provide good return in time of high interest rate, and this is not something I want to gamble on - as whether interest rate will return to 2% in the mid term. Inflation may be something that is here to stay with us for a long time, and all my holdings should be thriving in a high or low inflation environment. In contrast, MTB bank’s management (a new position but an old name - I first purchased MTB bank in 2001) has shown an excellent ability to navigate in a changing interest rate environment. MTB has generated record earnings in 2023. Based on the last 12 month, the bank is trading at less than 10x GAAP earnings which is much less than historical valuation.

The early year cleanup has allowed me to make place to newer players (Monarch cement, MTB Bank, Barry Callebaut and Hermle). I will provide the rational behind the purchase of Monarch cement, Barry Callebaut, and Hermle in the coming weeks. Lets just say that these are quality company with strong moat each operating in a industry that is promising. Monarch cement is in the infrastructure business, which had and will continue to have strong tailwind in the USA. Barry Callebaut is the leading sourcer and producer of chocolate, which is an industry with had a strong tailwind in the last 50 years both in terms of pricing and volume. Hermle is a leading manufacturer of high end 5 axis CNC enjoying fat margins and is positioned to benefit from the strong trend of automation manufacturing.

an individual investor that I admire has an excellent piece on his blog on this company: Analysis on HermleMy hope is that I bought these high quality companies at low price and that these companies will be over performing their respective industry and will stay in this portfolio for the next 10 years. But I do not kid myself, I am sure that in 4 years from now, only a few will remain.

For the 7 holdings purchased in 2022, 2023 and 2024, the jury is still out. Based on the previous 4 year period 2017-2020 period, only 3 positions (Tradedesk, Thermador and Celsius) have remained. In 4 years for now - I would be surprised that more than 40% of these names would still be there.

The 50% Drawdown Test

I personally think that in order for me to consider whether a position is a long term large holding that is compatible with my character and my circle of competence, it must have been tested by the 50% drawdown test. I believe, that the ultimate test is when a holding which represents a significant position is currently suffering a major drawdown of 50% or more from peak, and I am actually not doing a thing about it and I am not loosing sleep about it.

Ask yourself this question, how many large positions in your portfolio has suffered a 50% drawdown? What was your reaction at the time? Are you afraid that maybe you are wrong? Again this has to be a significant holding. Do you want to trim? Or do you want to add more so that you can average down in the hope that it will rebound quickly? Do you think that the fundamental headwind is more than temporary? Do you think the company has been permanently damaged. Are you confident of the management?

If any questions triggered a strong emotional reaction? This stock may not be for you and this may not be a long term position for you. This is nothing personal. Some stocks fits your personality as well as your familiarity of the industry. Find the stocks that fits your personality and your deep knowledge and keep those for a very long time. I need to reiterate that this holding must be significant when the drawdown starts.

If we take Google purchased in 2004, Google has suffered 2 major drawdowns of 50%+. This first one in 2007 to 2008, where the stock went from 695$ (pre 40x split) to 300$. I never sold a share neither buy one, and I didn’t loose sleep. I never questioned whether google has lost their moat and so on. The drawdown might have been related to the fear related to the emergence of mobile internet combined with the GFC if I recall. Most of the revenue at the time was related to PC web browsing.

The emergence of AI has caused the second 50% drawdown combined with the 2021 tech euphoria and subsequent burst. I did look very carefully at this one. I did worry a bit about the change. I spent a few weeks studying the side effect of AI, chatGBT/Bing combo etc.. but at the end I was totally confident that things would work out fine. One year later, I have seen how formidable the advanced gemini product is compare to other AI - I am using advanced Gemini all the time for my investment analysis. Google AI capability will be intertwined in the current google offering and I do not fear AI anymore. In any case, Google pass the 50% drawdown with flying color twice.

Amazon did pass the 50% drawdown test in 2022. I did see a 20% position cut in half. I actually never worried a iota on this one. The post covid effect and the related slowdown in e-commerce was just making Amazon moat larger as other e-commerce platform were scaling back.

Starbucks did suffer a 45% drawdown from 124$ to 70$ in mid 2021 to mid 2022). I did actually increase significantly my position in Starbucks during the drawdown, so I did reacted to the drawdown. To my defense, Starbucks was not a top15 position at the time, and I felt that I was finally given the opportunity to increase my stake. The same happen to Adyen in 2023, during the 2023 50%+ drawdown. I do think that in order to truly test my behavior in front of Adyen and Starbuck collapsing, both positions should have been significant enough position at the beginning of the collapse. I would say that SBUX 0.00%↑ and ADYEN have pass the test halfway. I believe a true 50% drawdown where I see a large holding collapsing 50% and I do nothing will be the ultimate test.

Tradedesk did suffer a sharp drawdown in 2022, and I did nothing except watching loosing 60% of its value. This one has been tested fully.

In summary, I would invite you to visit your portfolio and look for 50% drawdown of significant holding. A drawdown that is painful. For these one tested by fire successfully, earmark these stocks in some way. These stocks are meant for you. If you can’t find one, ask yourself why? You may not have found the correct set of stocks yet for you.

The same exercise where you watch yourself selling a position after a 20%, 30%, 40% drawdown can also be very instructive. These stocks should be earmarked negatively. They are not meant for you. I have a long list of stocks and industries. Those stocks I do not touch anymore! They should be totally removed from your watchlist. They are not meant for you. It is much easier to change your portfolio stock profile than your character.

Wow, honest and all kudos for trying to identify biases inside and how to harness them!

The 50% drawdown test is excellent! I've experienced it at the end of last year, but in a microcap. That's a lot harder to hold than a Google or Amazon. The perceived moat and quality of the company matters a lot. Great article!