$ALCLA French microcap freight forwarder Clasquin and analysis of 1H 2023 results

$ALCLA French microcap freight forwarder Clasquin and analysis of 1H 2023 results

How is the small French freight forwarder navigating the normalization of the shipping rates post COVID era

Normalization of the maritime container freight rate

Clasquin is an asset lite freight forwarder and about 50% of the gross profit is coming from the maritime business.

The maritime shipping business has experienced a very strong boom and bust cycle within 3 years due to the unique logistic issue faced during the COVID era. The maritime shipping rate has come down to pre COVID rate in the recent 6 months.

All figures in this article are in euros

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. Please refer to the disclaimer at the end of this article for more details.

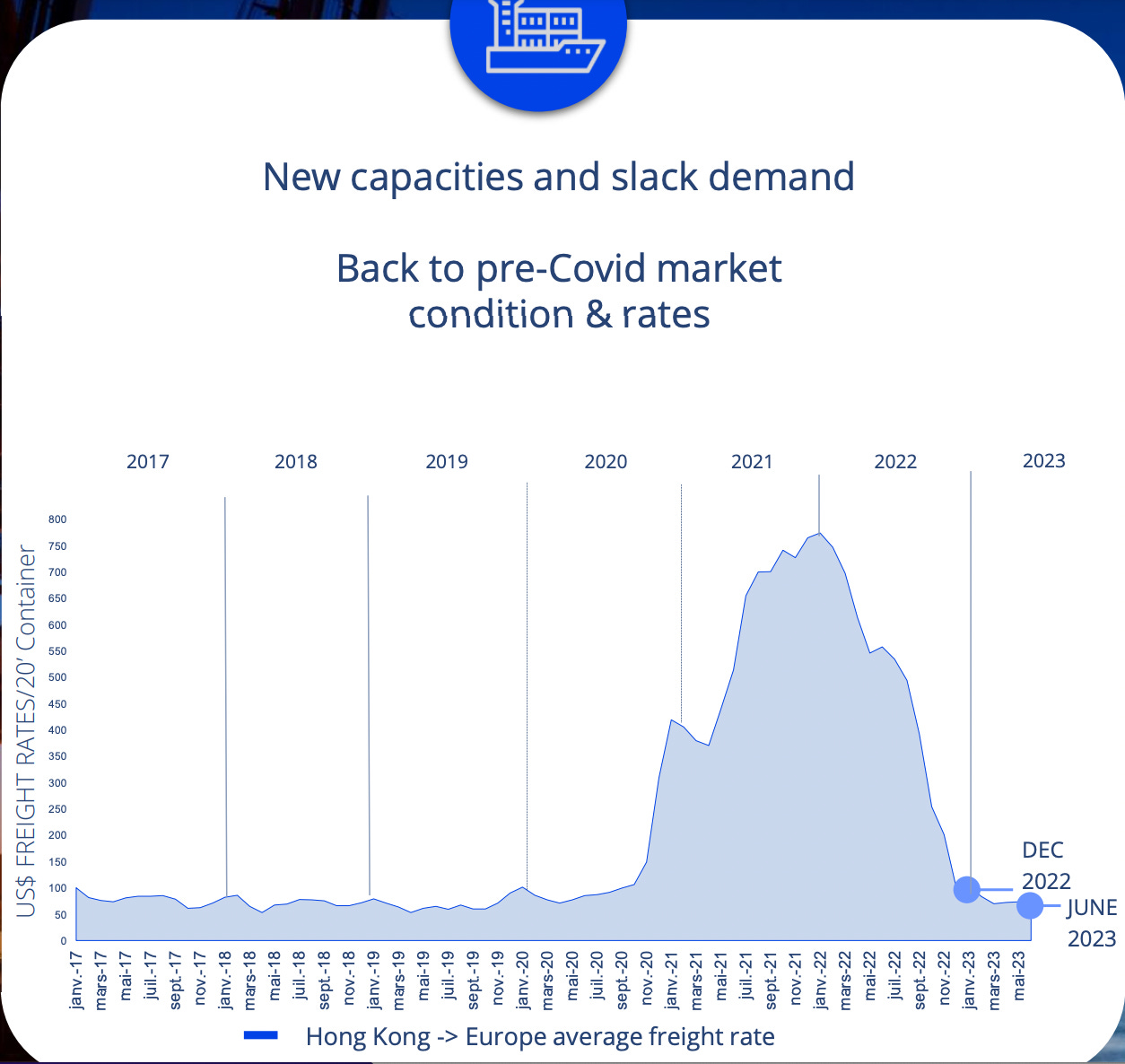

The following figure comes from the latest Clasquin investor presentation where it shows the freight rate of containers from Hong Kong to Europe. We can observe than since December 2022, the freight rate has come down to 2017-early 2020 level.

Another data point is to look at AP Moller Maersk latest results, the second largest ocean shipping company. AP Moller Maersk has seen its Q2 EBIT margin collapsing by 73%, going down to almost pre-COVID rate and a margin to 13.6% (down from 49%).

A similar sharp drop in profit can be seen accross all shipping companies - Hapag-Lloyd has published EBIT numbers down -83% for Q2.

Besides the sharp rate drop, global volume is down 4.3%.

But shipping companies are asset heavy business, so the freight rate impacts directly their operating income.

So how does this impact asset lite freight forwarder like Clasquin?

Maritime freight forward rate

As a freight forwarder, Clasquin gets a commission for each shipment handled and the gross profit per shipment does not fluctuate as much as the more cyclical freight rate. For more on Clasquin, please refer to deep analysis of this company here:

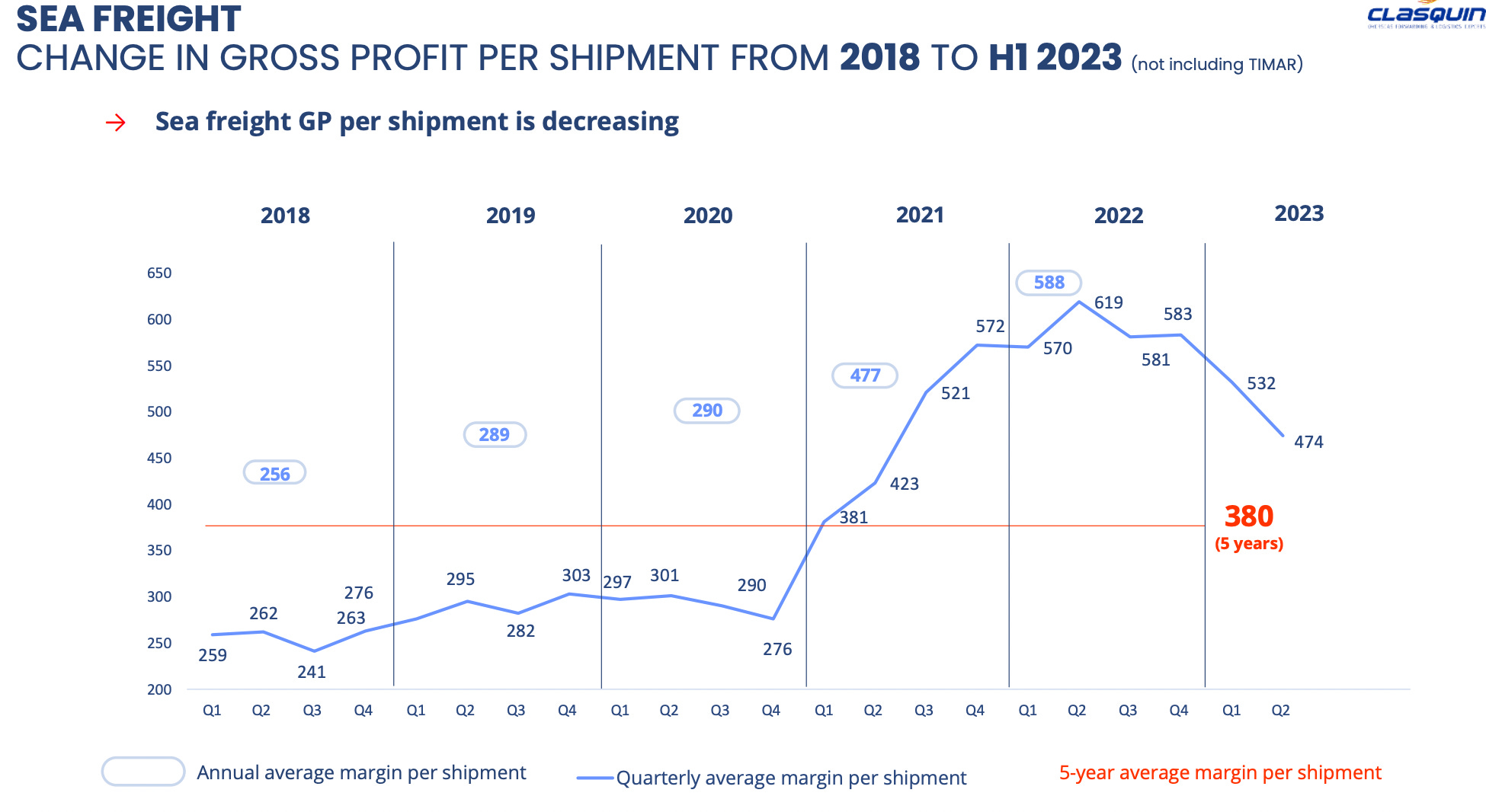

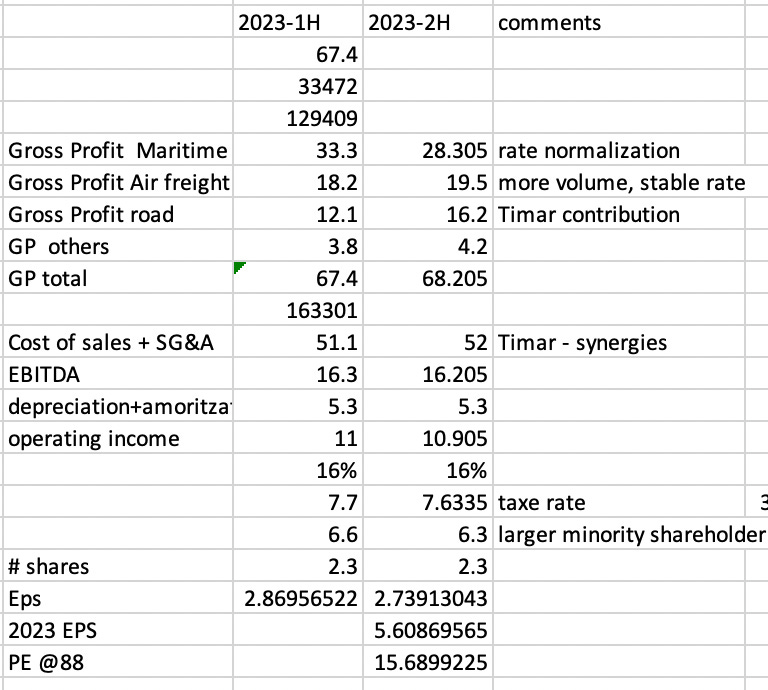

Below is the gross profit (net commission) that Clasquin gets for each shipment. From Q42021 to Q4 2022, it was hovering around 570 to 620 range. Since then, it has come down to 532 euro in Q1 and 474 euro in Q2. The 5 years average is 380euros. The gross profit per shipment has reduced by 11% sequentially from Q1 to Q2. We should expect the same downtrend in Q3 and Q4.

Normalization should continue in 2H 2023, with two 10% reduction according to the trendline, resulting into a 15% reduction of the GP in 2H for the maritime component versus 1H2023.

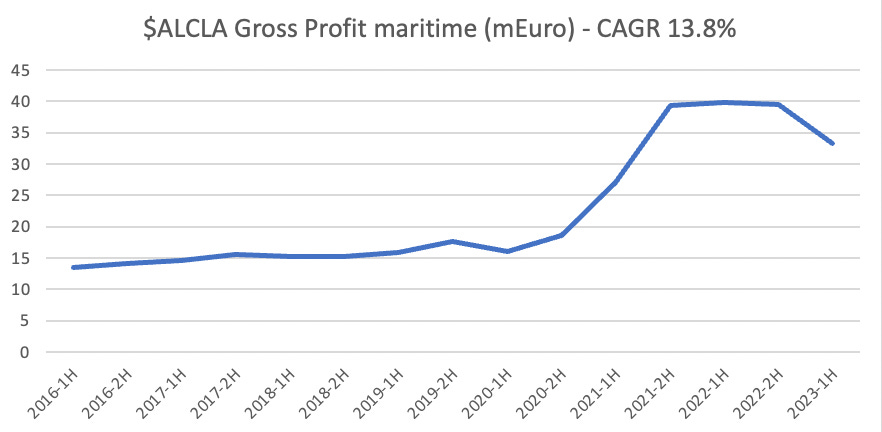

The following shows the gross profit from the maritime segment. 1H2023 had gross profit at 33.3m euro. A 15% reduction in commission rate should get us at a 28m euro range.

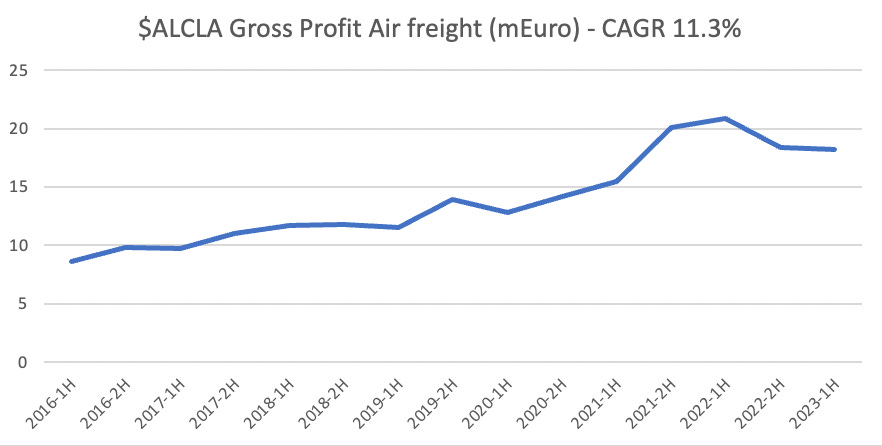

Air Freight rate stabilization

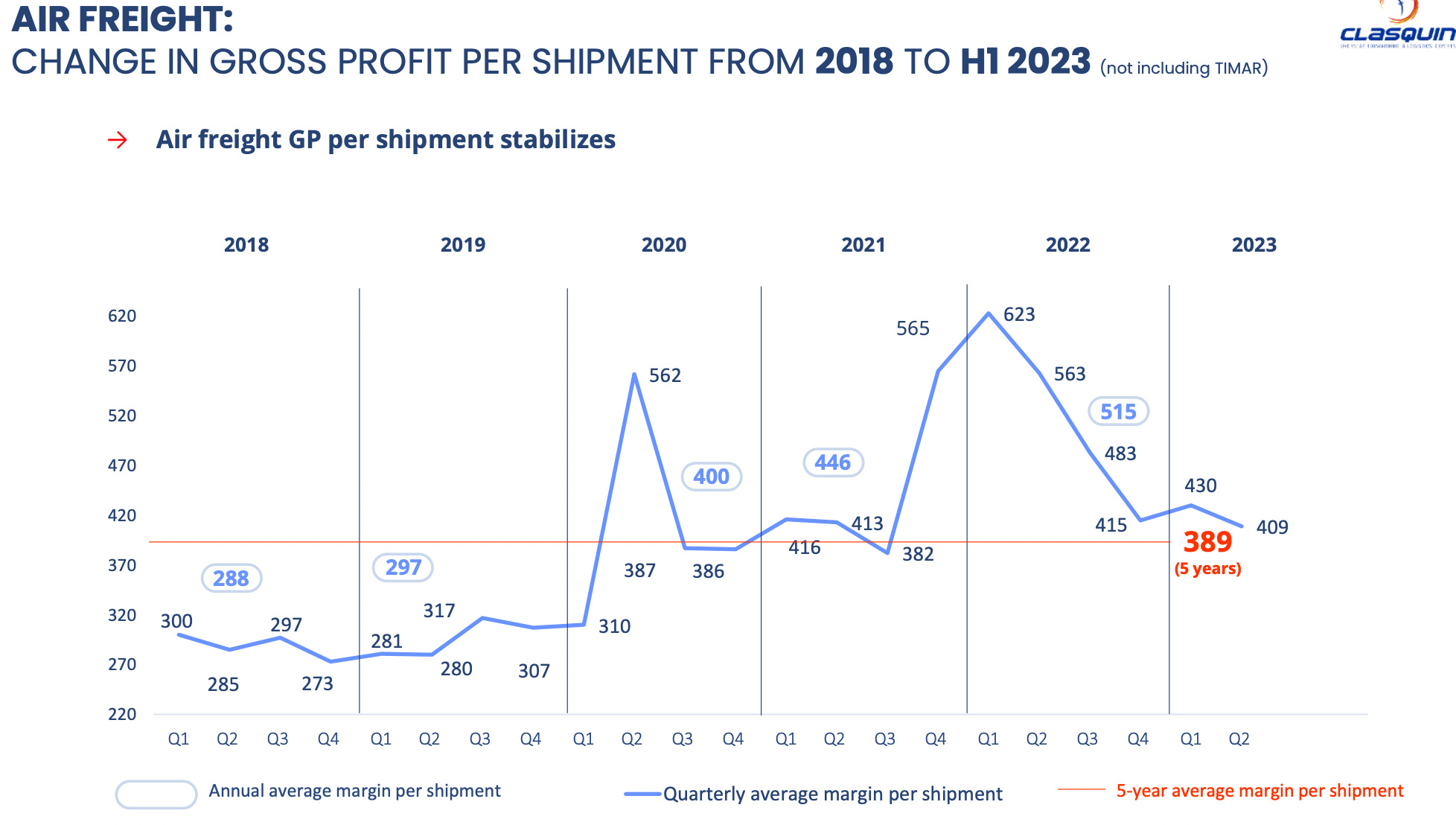

The air freight rate has been stable for the last 3 quarters and are pretty close to the 5 year average.

On top of that, Clasquin is gaining market share in this segment, with the number of shipments up 20.5% versus prior year. Assuming that gross profit per shipment remains stable, we should see an increase in gross profit with continued shipment growth sequentially.

The following shows the historical air freight contribution to the gross profit.

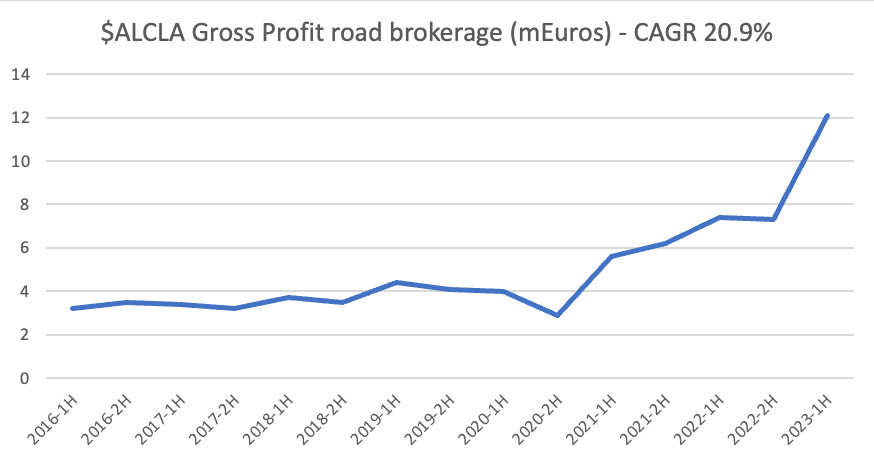

Road brokering and Timar contribution

Clasquin has acquired Timar, a Morocco based operation effective on April 2023. The company is mostly active in road brokerage. Timar contribution to the gross profit on road brokerage was 4.1mEuro in Q2. For the 2H 2023, contribution should be of 2 quarters. As such, road brokerage should be at 16mEuros.

The following shows the historical contribution of the road brokerage business to the gross profit.

Expense side

The expense side - even with the 3 acquisitions done in the last 12 months, has not raising significantly in the last 2 semesters. So we should expect cost control in the second half should maintain the expense line to about the same with a small increase for the addition of Timar for 2 quarters. Some synergies should keep expense line under control.

Estimates for 2023

Based on the following assumptions, I am forecasting that gross profit to remain about the same as 1H2023 and net income slightly lower.

Gross profit of the maritime business will be lowered due to continued downward pressure of the logistic maritime freight rate as per trend.

Gross profit of the air freight business should be slightly up due to increase volume and market share gain and price stabilization

Continued momentum on volume for road brokerage plus the contribution of Timar over 2 full quarters should see a good uptick on the gross profit.

Expense side should increase somewhat due to the overhead of Timar over 2 full quarters. Some synergies should lower the expense line.

The portion of earnings to minority shareholders will increased as Clasquin was not able to get the approval from all the shareholders of Timar. Clasquin has 66% of the shares of Timar. Timar is actually trading at 556 dirham, higher than the offer of 450 made by Clasquin. Timar is currently valued at 16mEuros. I would think that Clasquin will make an offer to the other shareholders at some point to fully consolidate the company.

My model is in line with the average earning estimates of a few brokers following this stock.

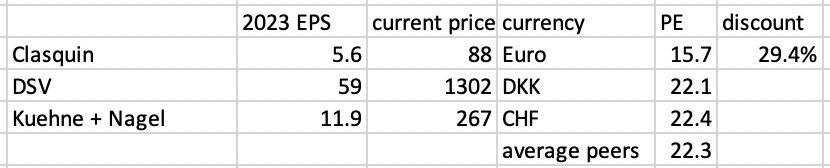

Peers comparison

At a price of 88 euros, Clasquin is trading at 15.7x my earning estimates for 2023.

If you look at the 2 closest peers, Kuehne + Nagel has earned 7.20 CHF in the last 6 months, is expected to earn 11.9 CHF in 2023 and is trading at 267 CHF or 22.4x earnings.

DSV has earned 30.50 DKK, is expected to earn 59 DKK in 2023 and is trading at 1301 DKK or 22x earnings.

So Clasquin, even if it is trading at 11% higher that when I originally published in July, 6th, is still trading at a significant discount of almost 30% to peers.

I prefer Clasquin over DSV and Kuene + Nagel for the following reasons:

Trades at a 30% discount to Peers

its a microcap with lots of room left to grow both geographically and in density including the Africa trading routes

Can do small bolt-on acquisitions of local SMEs - too small for large cap

Addresses niches with pricing power (high value items)

Net profit should grow with scale faster than gross profit - G&A overhead, new offices startup costs. Clasquin is finally reaching a certain scale.

Shareholder friendly (large payout dividends) and founder with 40%+ ownership

The balance sheet is pristine with a net cash balance of 3m (subtracting long term debt) which should allow to do bolt-on acquisition.

Thanks!

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested