$ILP Ilpra a growing Italian microcap food packaging manufacturer in a competitive market

$ILP Ilpra a growing Italian microcap food packaging manufacturer in a competitive market

Ilpra is an Italian based company specialized in packaging machine in the food industry. I was attracted by the top line growth and the low valuation and this is the result of my analysis.

Background

Ilpra’s high top line growth of the last few years combined with a low PE (PE ranging between 10-15) has originally attracted me. In the Spring of 2023, I purchased a tracking stake - a very small position - to force me into investigate the company. The fact that almost all documentation is in Italian in an industry that I am not familiar didn’t help so I kept pushing the investigation further and further until the last few weeks.

The following is the result of my investigation.

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

All currencies are in Euros.

Initial Investment Criteria

As mentioned in the previous analysis regarding Aplisens, there are a few key criteria that must be checked before I decide to invest in a company:

An industry I understand and/or a clear understanding that the company has a moat in the industry

Top line growing at a 10-15% rate or more

Positive operational leverage: A top line growth translates into an equal or larger rate of increase in profit.

Skin in the game

Attractive shareholder yield through buyback, dividends or accretive acquisitions

Acceptable RoIc which allows to grow without leveraging the balance sheet

Under-followed company priced at a PE below the growth rate

The Packaging Food Industry

This industry consist of selling off-the-shelf or custom machines to food processor., Since this is not a product targeting directly the consumer, it is always difficult to understand the dynamic involved in a B2B industry. When I invest in B2C company like Starbucks, Campari, Google, Amazon or Netflix, it is much easier to understand the dynamic between suppliers, customers and so on. For B2B business, the business must be very understandable (i.e Logistec or in a business that I am familiar with - in my case as a system/SW engineer like a business like AWS or the recent industrial sensor product company Aplisens.

Although i understand the underlying technology related to the the automation of food processing at high level, this is not an industry I have worked in as a system engineer or investigated previously in a previous investment. It is outside my current circle of competency. Especially the dynamics between the suppliers of Ilpra and the targeted customers.

If an industry is outside my circle of competency, then the moat criteria becomes essential.

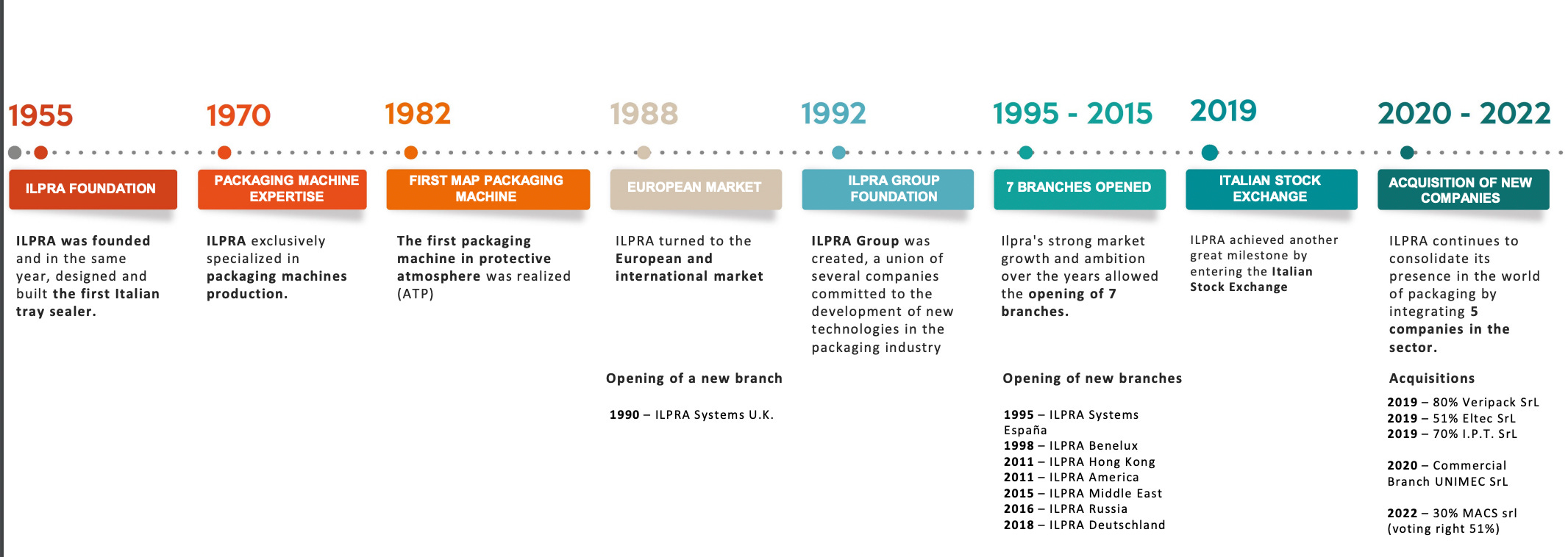

Ilpra has been producing tray sealing machine since 1955, so were they able to create a moat in this business?

Moat in Tray Sealing Machine?

History on Ilpra: Ilpra has designed the first italian tray sealer machine in 1955.

Still today 70% of sales is related to the tray sealer machinery as show in their 2019 IPO slides

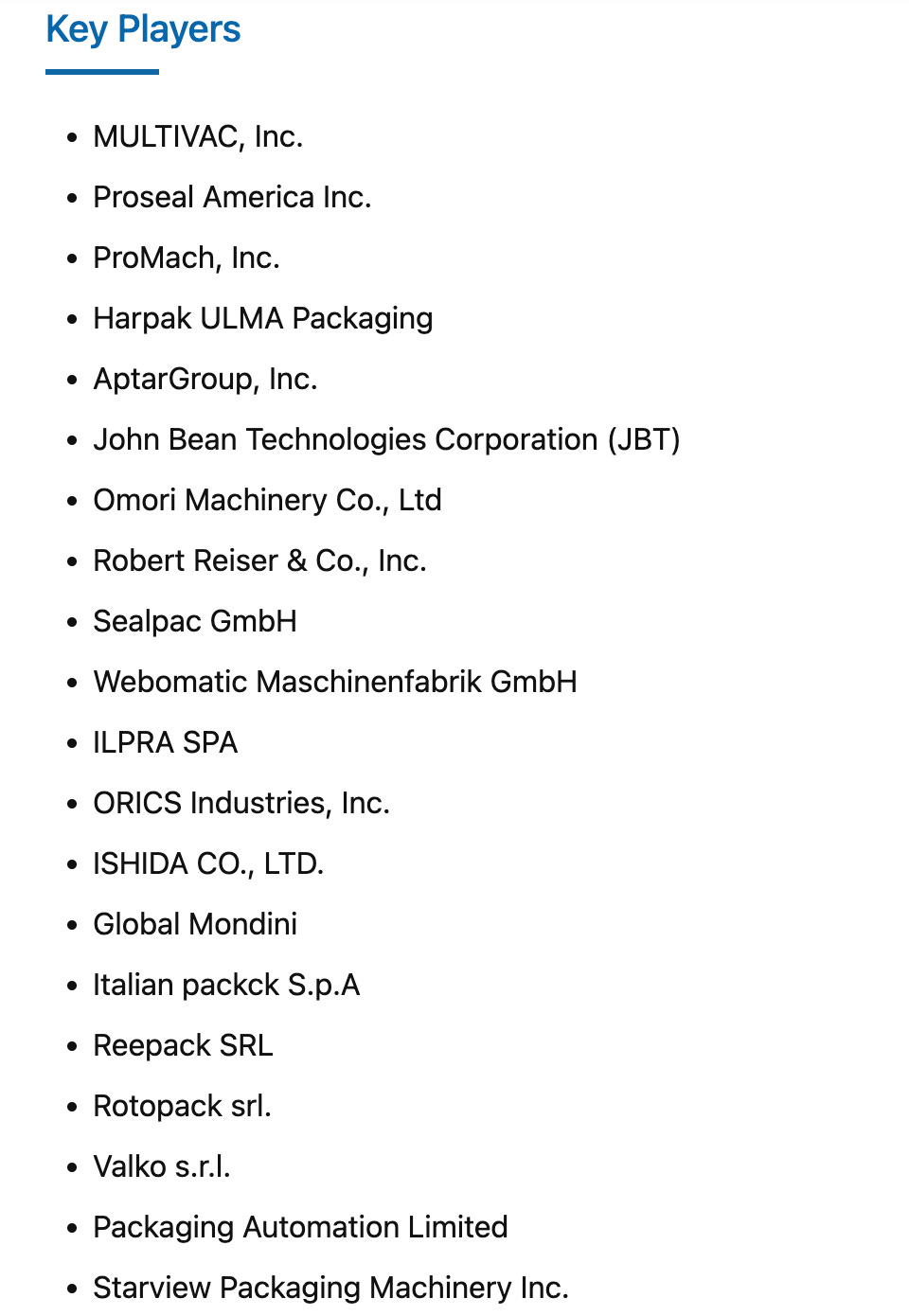

So if we focus on the tray sealing machine vendor, here are the top vendors according to a market research from Future market insights.

So all these companies seems to be offering similar products with limited product differences. This is a commoditized product line with focus on customization. A lot of customization means only one thing to the bottom line, limited economy of scale and margin that are capped on the upside. Customization is typically priced at cost plus. Customization is done at a small profit margin as no salesman wants to risk of loosing a sale by charging big extra for customization especially in a competitive market.

If you look at the home market, the situation is a little bit better and here is what Ilpra had to say in their 2018 prospectus:

Within the national territory, the market segment in which the Group operates is characterized by considerable fragmentation and does not reveal a significant direct presence of other comparable players for the range of services offered and size of the company measured in terms of turnover. In fact, from an analysis carried out by the Company it emerges that the majority of companies identified as possible competitors, around 40 companies, have a turnover of less than 5 million Euros and are mainly focused on serving the domestic market.

Still, in Italy where the company has operated for more than 70 years, they were not able to achieve total dominance with 40 competitors to the company product. To be fair, in the tray sealing machine market they are probably #1 or #2 in this specific market of Italia, but still it is a very competitive market with 40 competitors. In the RoW, things are even worse.

I also suspect that most of the vendors are using common technology enablers provided by Mitsubishi, Siemens or Rockwell Automation. These suppliers are mentioned by Ilpra. Ilpra has a special collaboration with Mitsubishi. Ulma Packaging, another competitor is using exclusively Rockwell Automation software and solution.

Personally, I think that if we want to find some moat in this fragmented industry, one must look one level further in the chain and look at the underlying technology developed by Rockwell Automation or Mitsubishi.

Actually investigating a company like Rockwell Automation could be interesting as a next step to better undertand the industry. Rockwell Automation should be playing a key role in the reshoring and automation trend in general.

Top line growing at a 10-15% rate or more

Sales of Ilpra has been growing steadily at a CAGR of 19% since 2016. Ipra has made several acquisitions since the IPO, so the growth might have been accelerated by the acquisitions. However, Ilpra does not disclose organic growth versus growth from acquisition. This is something they should improve upon.

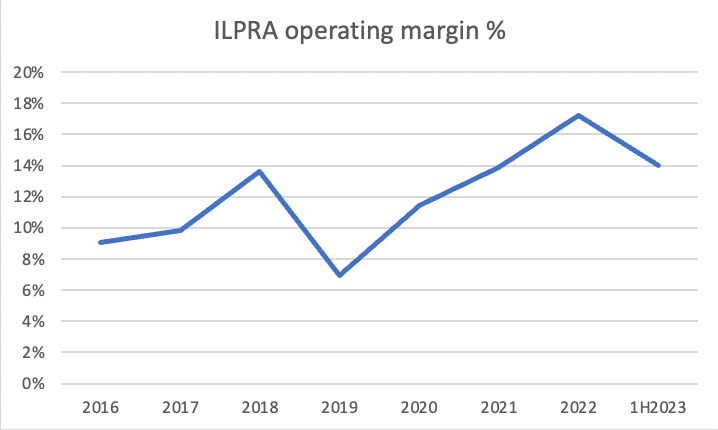

Profit and operating income margin

Profit and operating income margin have grown more rapidly from the 2016 level. 2019 had a bad year with a sharp drop in earnings. 2022 seems to be have exceptionally good in terms of margin based on 2021 result and the first half of 2023.

Skin in the game:

The current CEO - of 65 of age - controls 71% of the company. He did sell 8% of the company in early 2023. This is something to worry about a bit.

Attractive shareholder yield

Most of the funds generated from the business has been funneled to the increase working capital needs to support the growth in sales and some acquisitions. The ratio of sales to inventory is quite significant based on the latest semester.

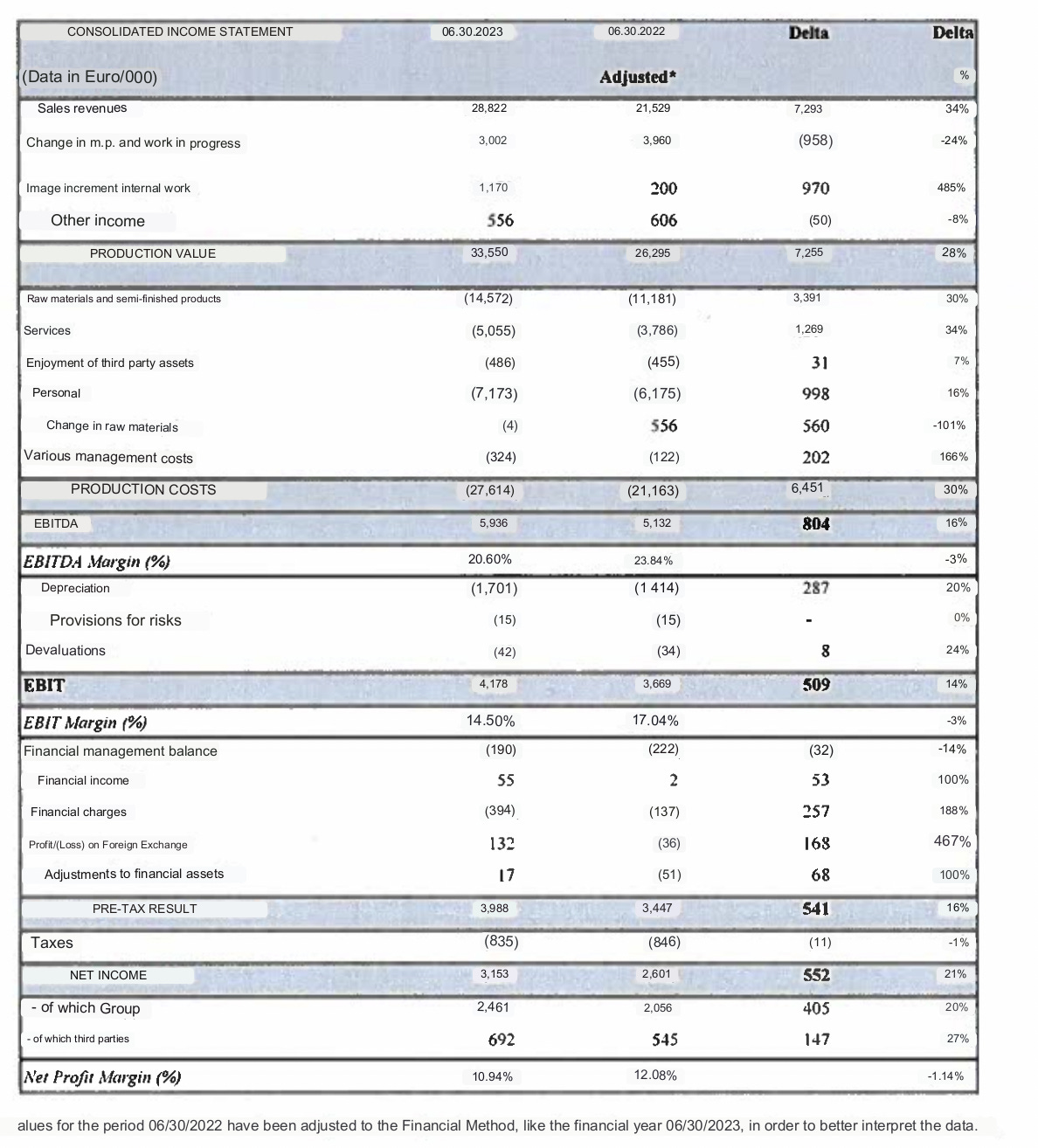

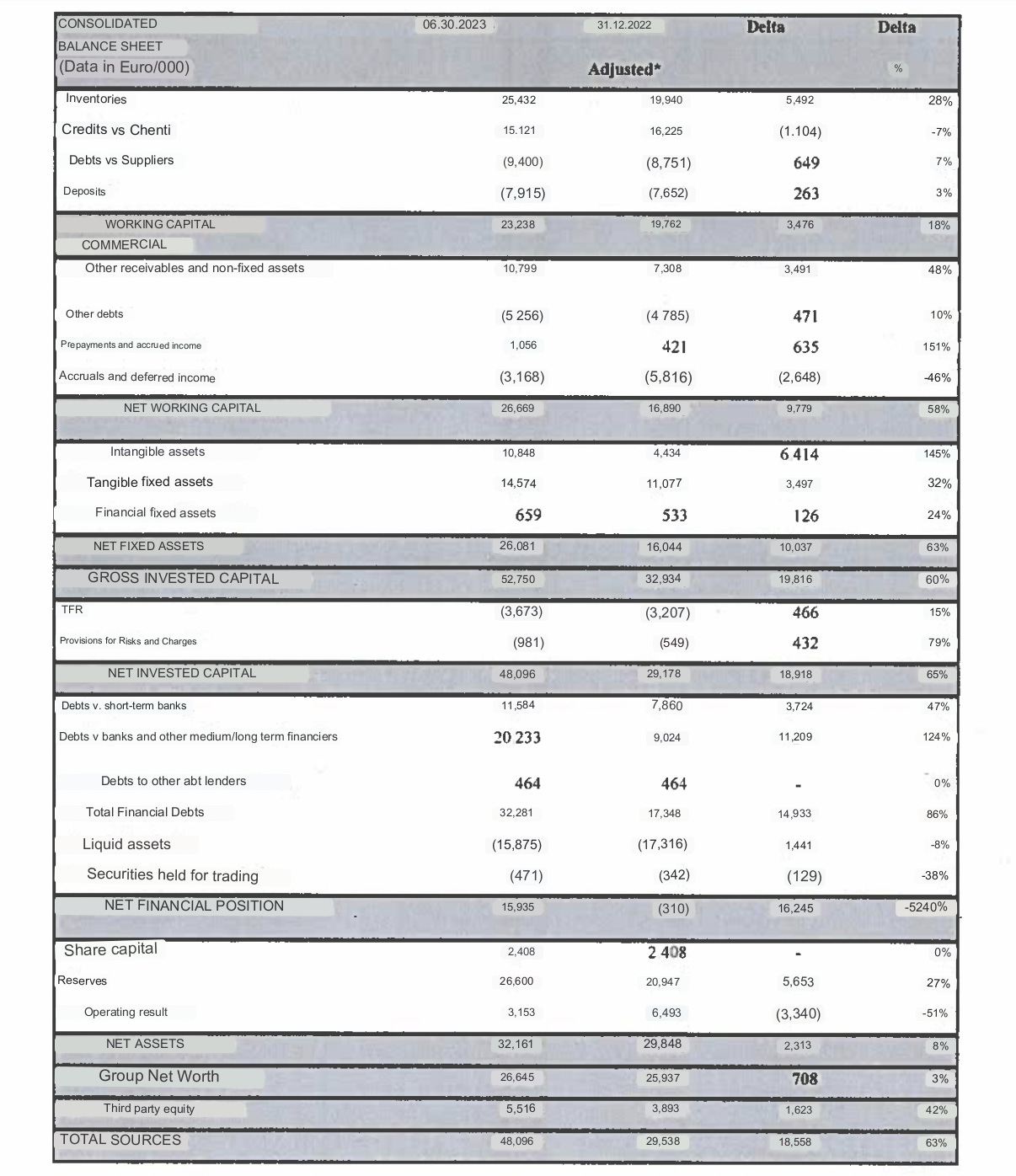

You can find the latest financial statement as of June 2023 below:

Inventories has risen by 5.5m in the last 6 months to 25.4m.

Gross invested capital due also to acquisitions and plants upgrade have risen to 52.7m. Debt has risen significantly in the short term, so all the profits are funneled in the business and more.

Ilpra has also given a small dividend of 0.12 per share or 2.25% at the current price for 2022.

Acceptable ROIC

For ROIC we will take the NOPAT/Invested Capital definition.

NOPAT=Net operating profit aftertax.

(Net operating income - tax) / Gross invested capital for the last 12 month.

ROIC = 9m-1.8m/52.7m= 13.6%.

This ROIC is acceptable for a 10-15% grower. However, current trend of growth at around 20%-30% is not sustainable, thus the increase in debt.

As an investor, with a ROIC of 13.6%, one should not pay up for a growth higher than the ROIC. Higher ROIC would be required to pay for a higher growth. In other words, the Company’s cannot generate sufficient profit to sustain a higher growth over the long term without levering the balance sheet too high.

Priced at a PE below the Long term growth rate

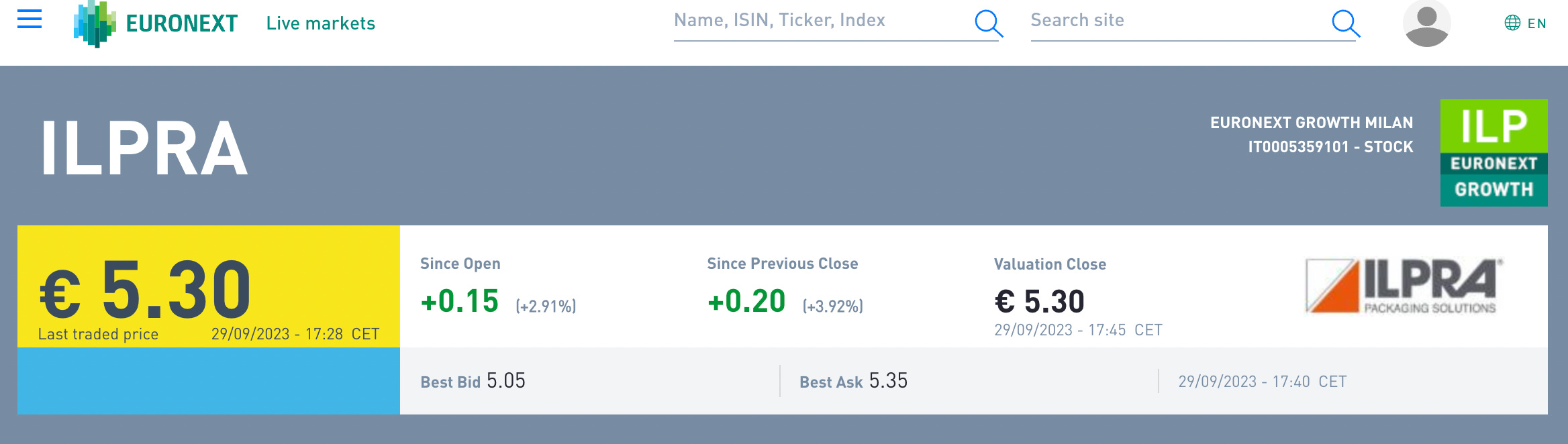

ILPRA currently trades at the Euronext Growth Milan stock exchange. Last trade at the time of writing is 5.30. Trailing 12mo EPS is 0.466, so it is currently trading at a low PE of 11.35.

The sustainable long term growth rate according to the latest ROIC is around 14%. So the PE is priced below the LT growth rate. The CAGR of sales since 2016 is 19%. So 14% should be achievable. So ILPRA is priced attractively.

Red flags from 1H 2023

Inventory has grown way too fast (by almost 30%) in the last 6 months. The ratio of inventory to the last 12mo sales is now 159 days or 5.2 months. The company has very long lead time to delivery and is trying to compensate by increasing inventory.

EBITDA margin went down from 23.6% in 2022, to 20.6% while sales has grown very quickly. This is worrisome since an increase of sales should increase the utilisation rate of the fixed assets (plants, machines) used to produce goods. This means that the variable costs (labour, raw materials, supplier components) are a large component of the cost. Looking at the latest result, we can observe that cost of raw materials and semi finished product (30% incr.) and cost of services (34% incr.) have increased faster than production sale. I suspect that the production is highly dependant on parts from suppliers and raw materials and highly labour intensive and custom made. This need to be improved.

Summary

The following shows my assessment based on the current analysis of Ilpra. 5 criteria out of 8 are passing. From a valuation (cheapness factor) and growth point of view, the company is passing. Since I do not have a clear understanding of the industry dynamic and the main product line (automatic tray sealer) seems to be in a very competitive market almost commoditized, I will pass for now. I would also like to see significant improvement in the next semester in terms of cash management (reduction of inventory) and cost efficiency (improvement of margin). Synergies from acquisitions should be Even in competitive market, a moat can be build by being a low cost manufacturer due to scale or innovation. I do not believe this is the case here at the moment.

Next steps:

I will investigate further the players providing the underlying technology of the food packaging industy, namely Rockwell automation and Mitsubishi.

If you have more insights in this industry or wish to provide another point fo view, feel free to send your comments below

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested.

I looked at them recently. What ultimately made me pass on them was their decisions continue operating in Russia. It’s only 2% of their revenues, but they talk about the difficulties of keeping it running the significant risk with supplying the branch. It just seems like bad allocation to not sell or dissolve it