Infrastructure: North American Cement and Aggregates Producers Review

Going though key operating Indicators and valuations of North American peers to Monarch Cement i.e. producers of cement and aggregates: Vulcan, Martin Marietta, CRH, Summit Materials

In the last article, I went over Monarch cement’s impressive operating performance in the last 10 years. The industry as a whole is benefiting from a strong tailwind in renewed demand for infrastructure materials and in contrast to other commodities, aggregates and cements must be produced locally due to the relative importance of the transport cost versus the commodity cost. This industry is capacity constraint due to the though environmental regulations and the local political refusal to build de novo sites (not in my backward phenomenon). As such this industry benefits from strong pricing as demand increases.

The article constitutes my personal views and is for entertainment purposes only. The main goal of this article is to log my personal views. Nothing in this article or these posts in this blog should constitute an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

I have identified a list of public company pure plays of aggregates and cement producers with a majority of sales in North America. This is the list with market cap in billion USD:

Vulcan Materials: $34B

Martin Marietta Materials : $35.7B

Monarch Cement: $0.7B

CRH plc (CRH): $56B - 65% of sales NA

Summit Materials: 6.9B$

I excluded Cemex, Holcim and Buzzi Spa since USA/CAN represents less than 50% of sales. I excluded Eagle Materials, since more than 50% of operating profit is coming from the gypsum wallboard segment. The gypsum wallboard market is related to the construction market solely and is outside the scope of this article (cement and aggregates). Gypsum wallboard is a lighter commodity with a relative price to weight much higher, which allows to be shipped farther compare to aggregates and cement which must be produced locally.

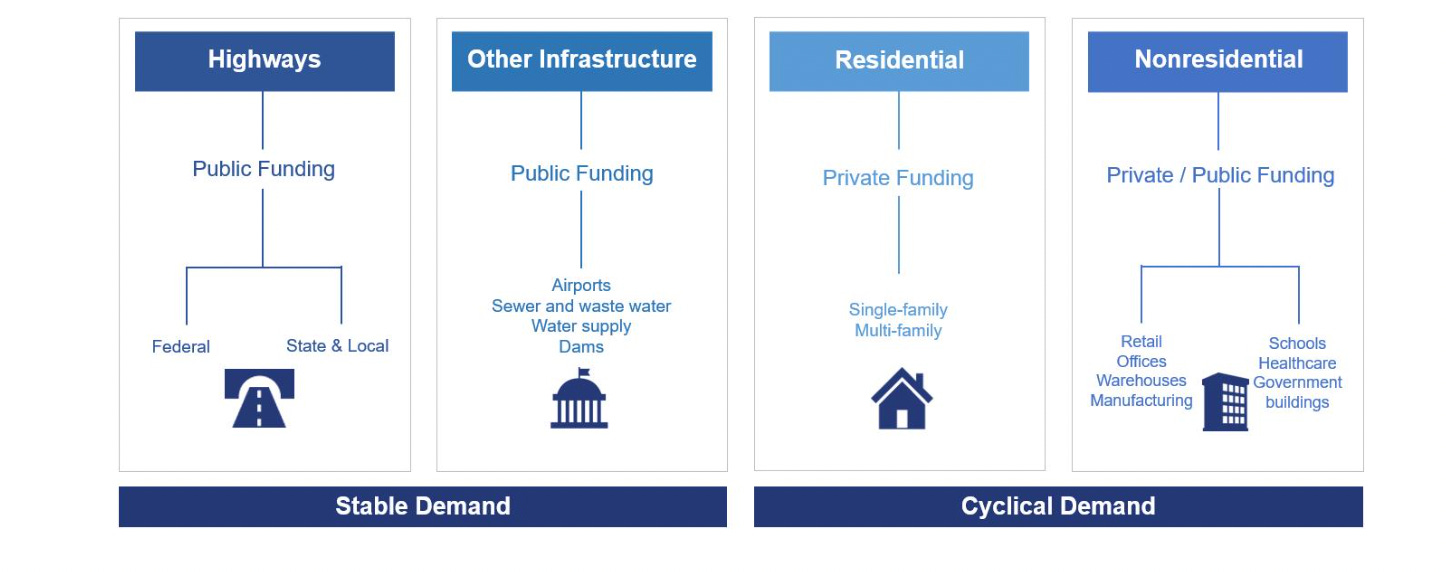

Aggregates end-market

Construction aggregates are used ubiquitously in many industries

base material underneath highways, walkways, airport runways, parking lots and railroads

Aid in water filtration, purification and erosion control

Raw material used in combination with other resources to construct many of the items we rely on to sustain our quality of life, including:

houses and apartments, roads, bridges and parking lots, schools and hospitals, commercial buildings and retail space, factories, sewer systems, power plants, airports and runways

The end market of aggregates is split into cyclical and non cyclical end market. Public funded infrastructure (highways and airports, sewer, water supply, dams, etc) provides stable demand. Residential and non residential are cyclical. The two cyclical can be countercycle with one to each other and can provide a balance demand overall. For example, residential construction did slowdown in 2023 due to the higher interest rate for mortgage, but the current strength in new manufacturing construction in US related to the manufacturing reshoring, is providing a counterbalance to the weaker residential market.

Why North America? The reshoring tailwind

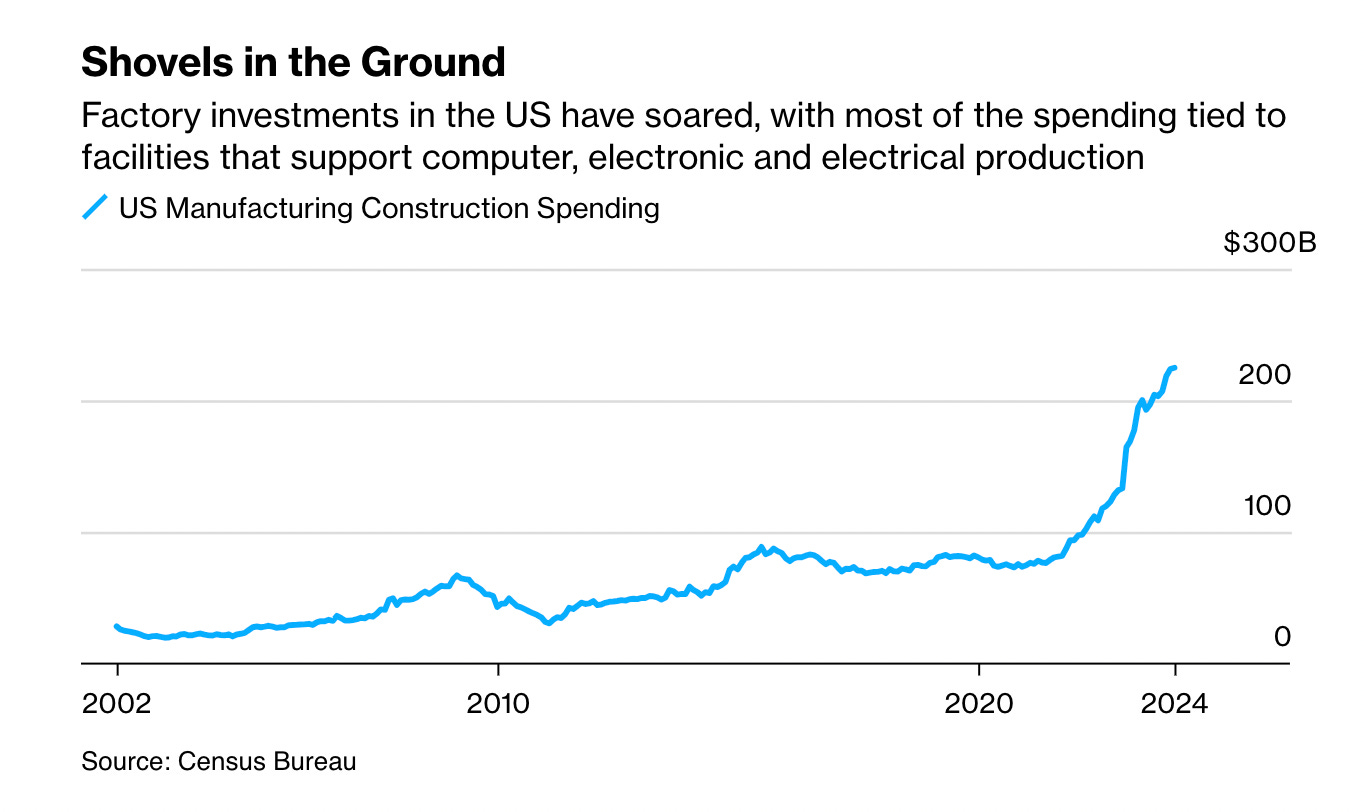

Monarch Cement is operating in US, so I initially started this article to assess peers in the same market. One of the attraction of Monarch Cement is that it is operating in the US which is seeing a revival on infrastructure investment. Manufacturing Reshoring is a strong positive trend. Many large companies are bringing manufacturing operations back to the US from overseas locations. This trend is fueled by the desire to establish a more resilient supply chain. The supply shock have been problematic for many companies during COVID-19. Over-dependence to China supply and the political tension between the two countries including trade barriers have been strong factors. Government incentives such as the infrastructure act and the CHIPS act are also fueling the reshoring effort. There is to a lesser degree rising costs overseas and consumer preferences. This is not wishful thinking, as factory investments in the US have soared in recent years as shown in the figure below.

Each new factory requires a lot of concrete and aggregates.

Vulcan Materials

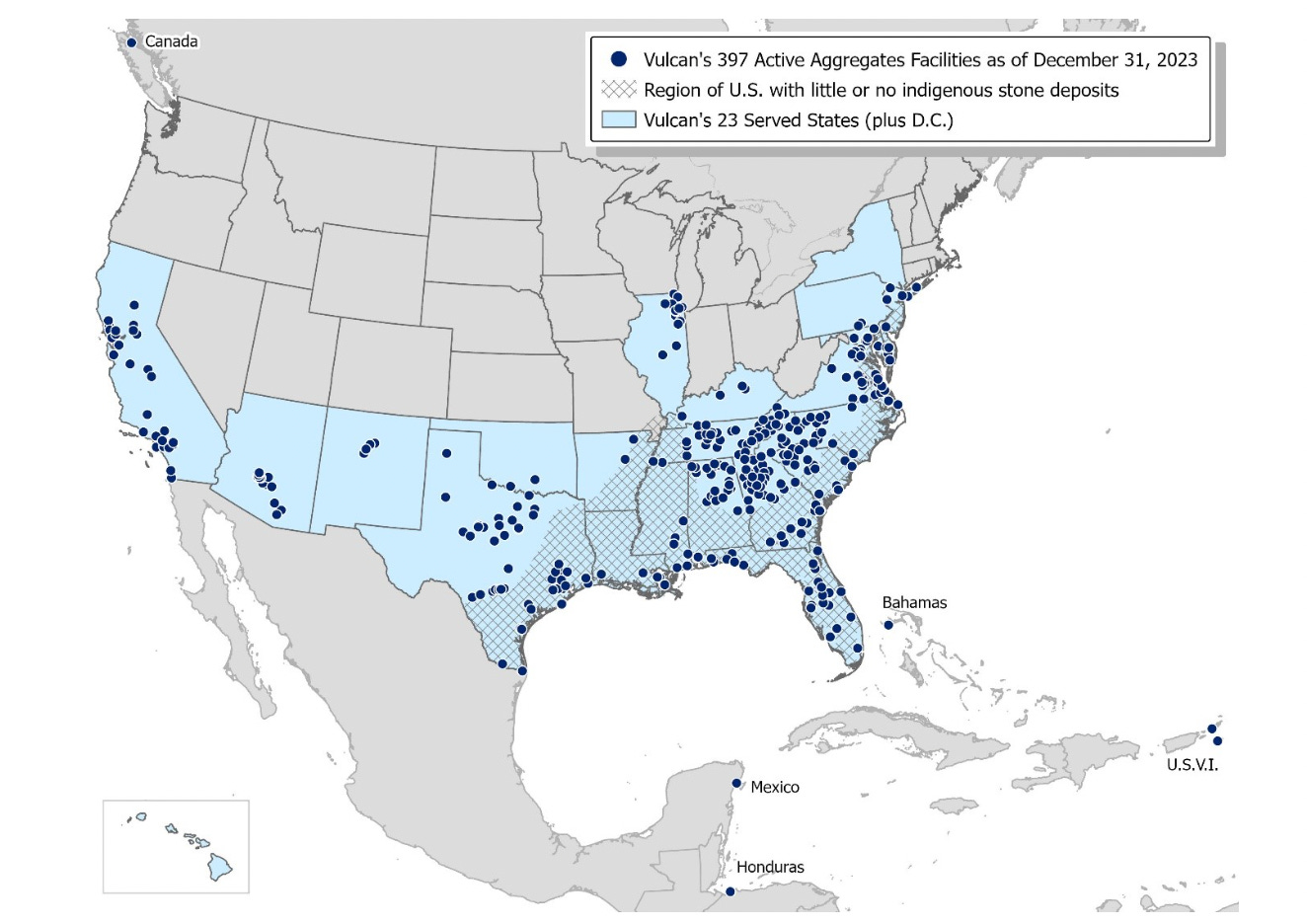

The largest producer of aggregates for the construction industry in US. 89% of gross profit (and 69% of sales) is coming from the production of company owned aggregates quarries: crushed stone, sand, and gravel. The company has 397 quarries in 23 states in US. The rest of sales is from downstream products such as asphalt (16% of sales ) and ready-mixed concretes (15% of sales). It does not own any Portland cement plant.

Acquisition based growth

Since getting approval to start a new aggregate open pit operating is a very long and difficult process, Vulcan has relied mostly on acquisition to expand its footprint:

Since becoming a public company in 1956, Vulcan has principally grown by mergers and acquisitions. In 1999, we acquired CalMat Co., thereby expanding our aggregates operations into California and Arizona and making us one of the nation’s leading producers of asphalt mix. In 2007, we acquired Florida Rock Industries, Inc., expanding our aggregates business in Florida and our aggregates and ready-mixed concrete businesses in other Mid-Atlantic and Southeastern states. In 2017, we acquired Aggregates USA, greatly expanding our ability to serve customers in Florida, Georgia and South Carolina. In 2021, we acquired U.S. Concrete, enhancing and expanding our aggregates-led business in attractive growing metropolitan areas.

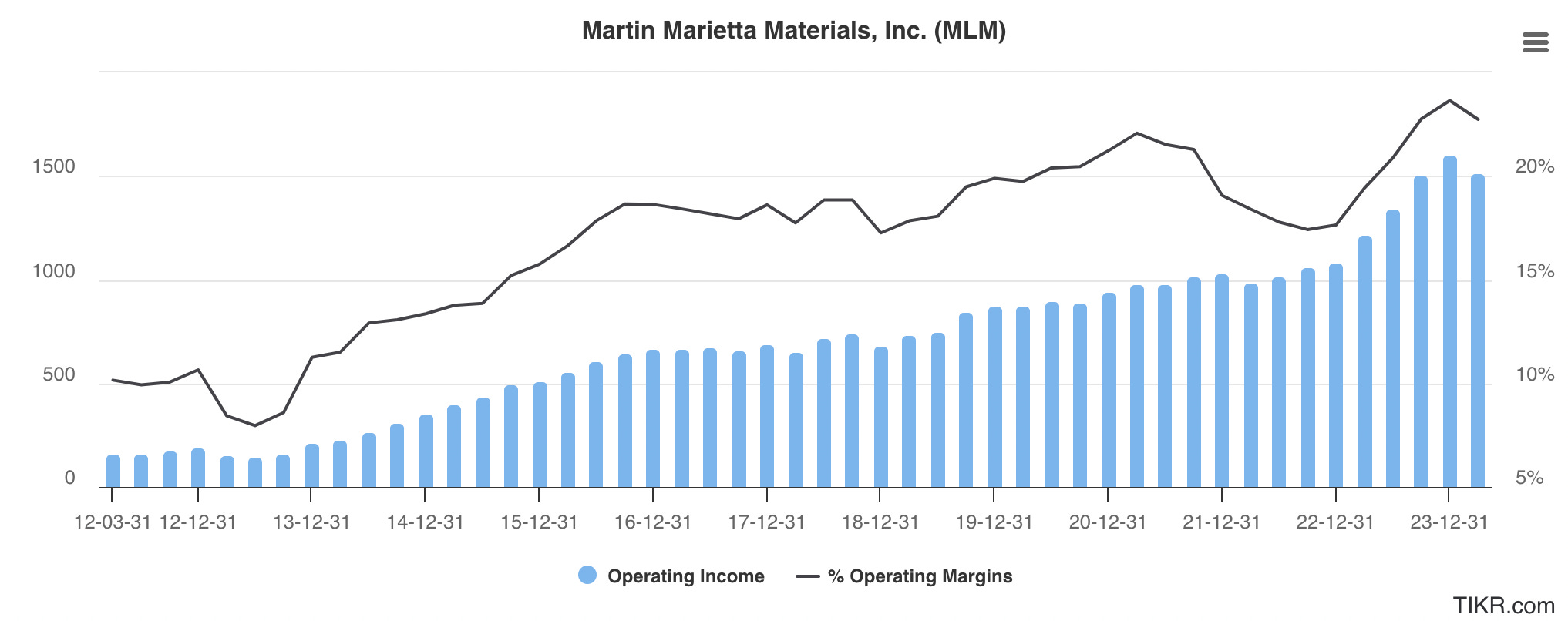

Martin Marietta Materials

Martin Marietta supplies aggregates (crushed stone, sand and gravel) through its network of approximately 360 quarries, mines and distribution yards in 28 states, Canada and The Bahamas. Martin Marietta also provides cement and downstream products and services, namely, ready mixed concrete, asphalt and paving, in vertically‐integrated structured markets where the Company also has a leading aggregates position. Specifically, the Company has two cement plants and several cement distribution facilities in Texas; ready mixed concrete plants in Arizona and Texas; and asphalt plants in Arizona, California, Colorado and Minnesota. Paving services are located in California and Colorado. Martin Marietta has been making several large acquisitions but have been selling part of the acquired assets (often ready-mixed and cement plant) to focus on aggregates production.

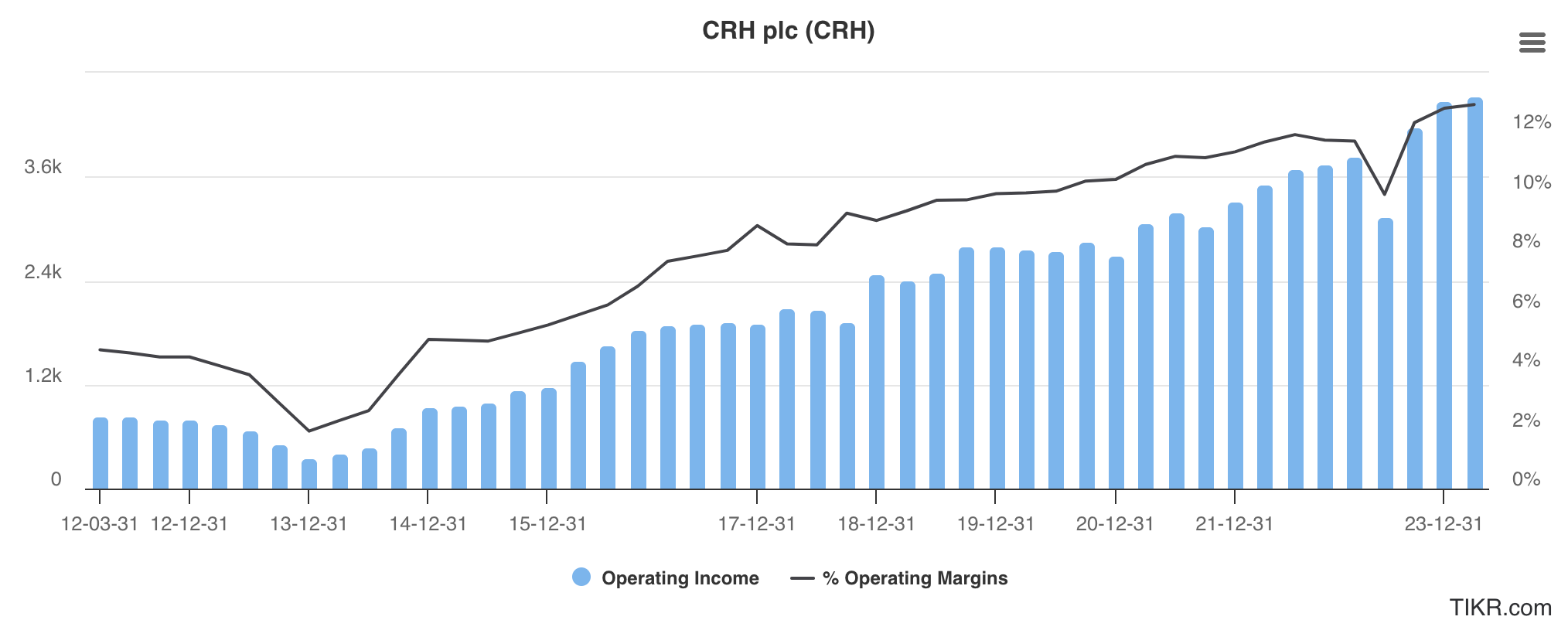

CRH

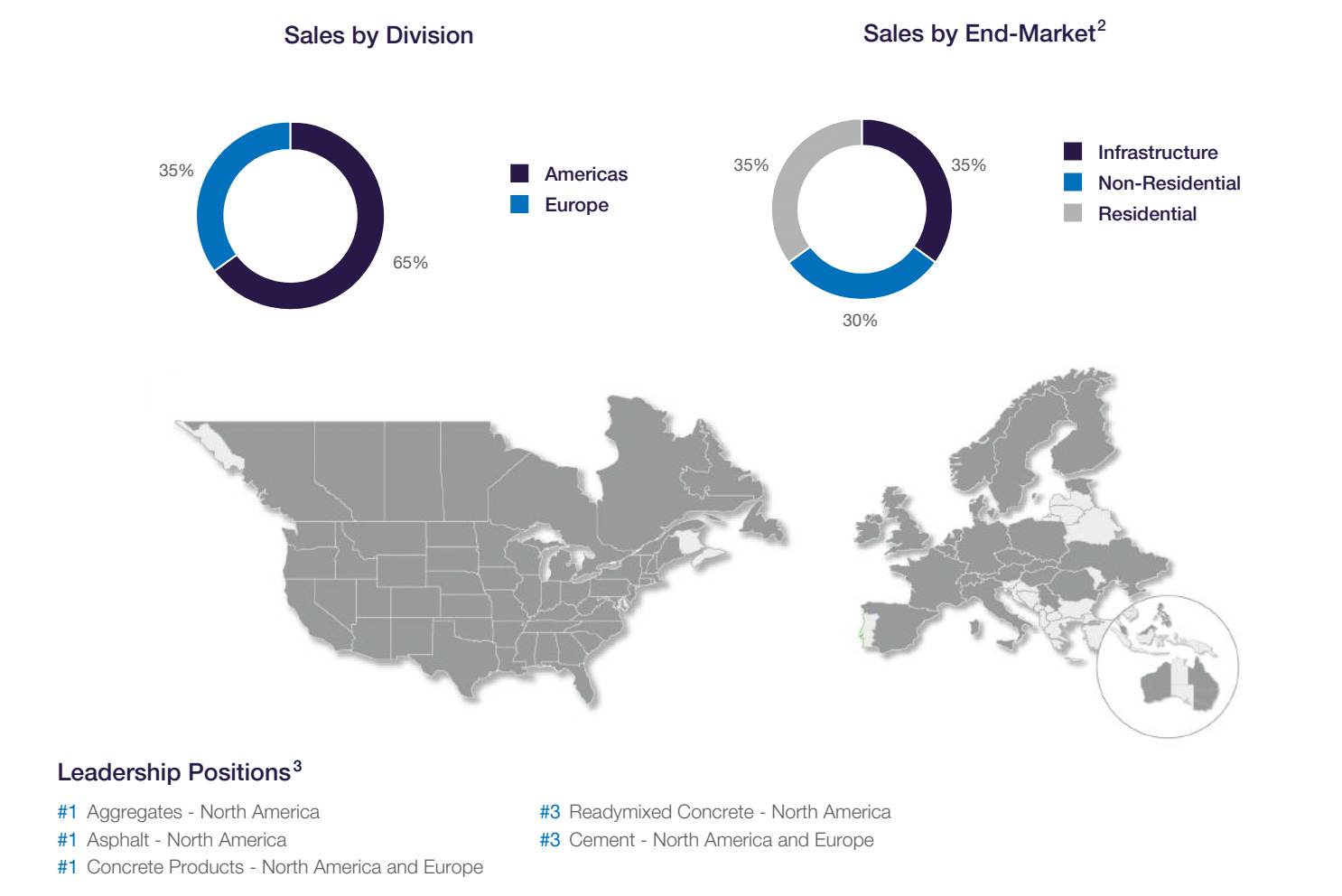

NA segments currently represent approximately 65% of sales and 75% of Adjusted EBITDA. End-market is split equally between infrastructure, non-residential and residential. CRH is the #1 producer of aggregates in NA but in contrast to Martin Marietta and Vulcan, they hold a significant position in the cement production. They actually bought Martin Marietta’s cement operations in South Texas for $2.1B. They are the #3 Cement producer in Europe and NA.

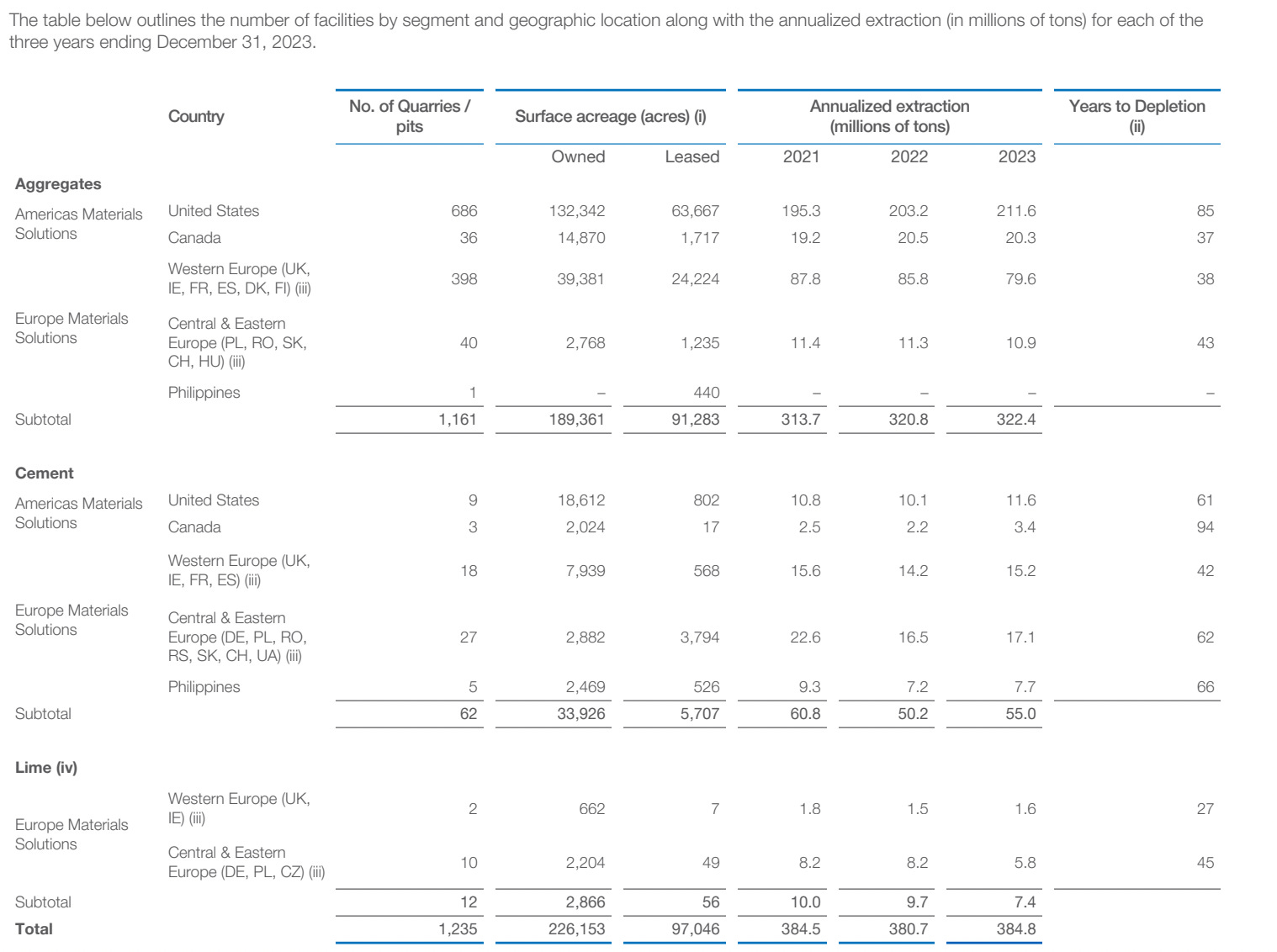

As shown below, CRH is the largest aggregate producers in NA with 686 quarries in US and 36 quarries in Canada. It operates 12 cement plant in NA and 18 cement plants in Western Europe. It is a minor player in aggregates in Europe with only 40 quarries.

Mineral quarries in US and in Canada. Stronger presence in the North states than Marietta and Vulcan.

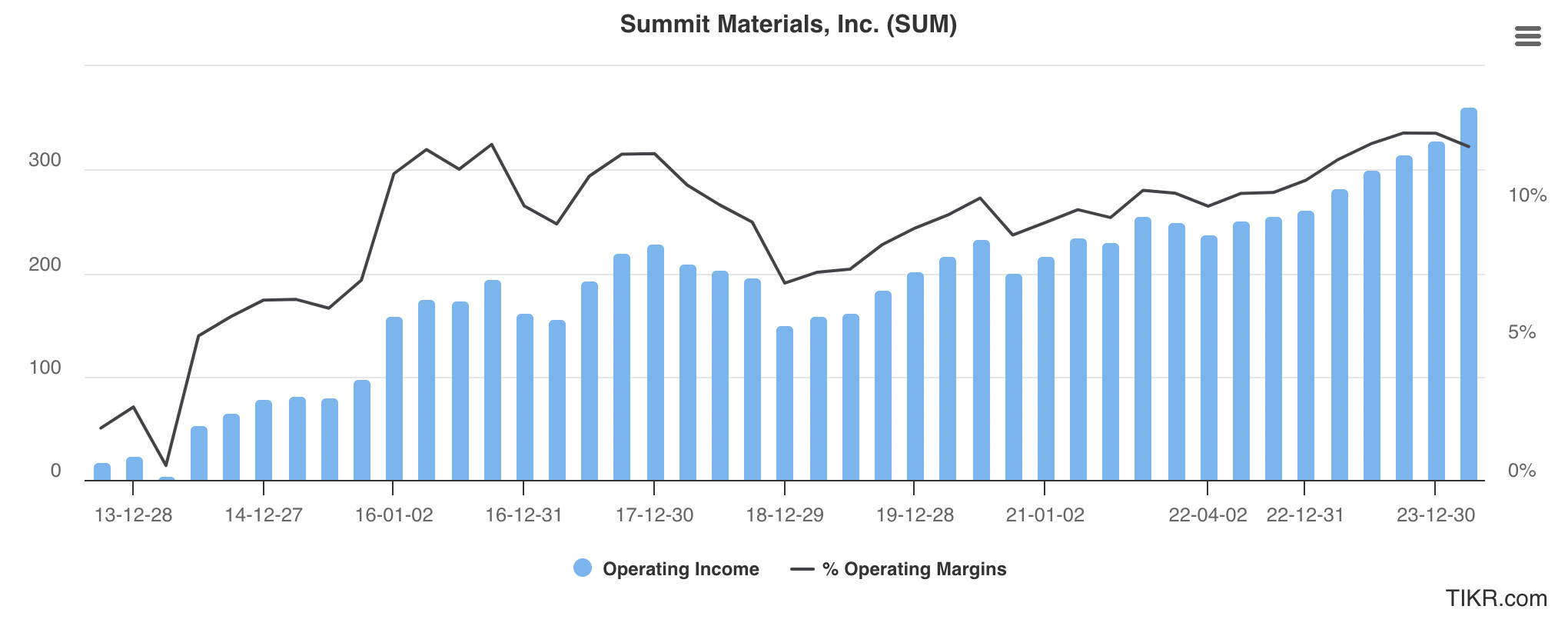

Summit Materials

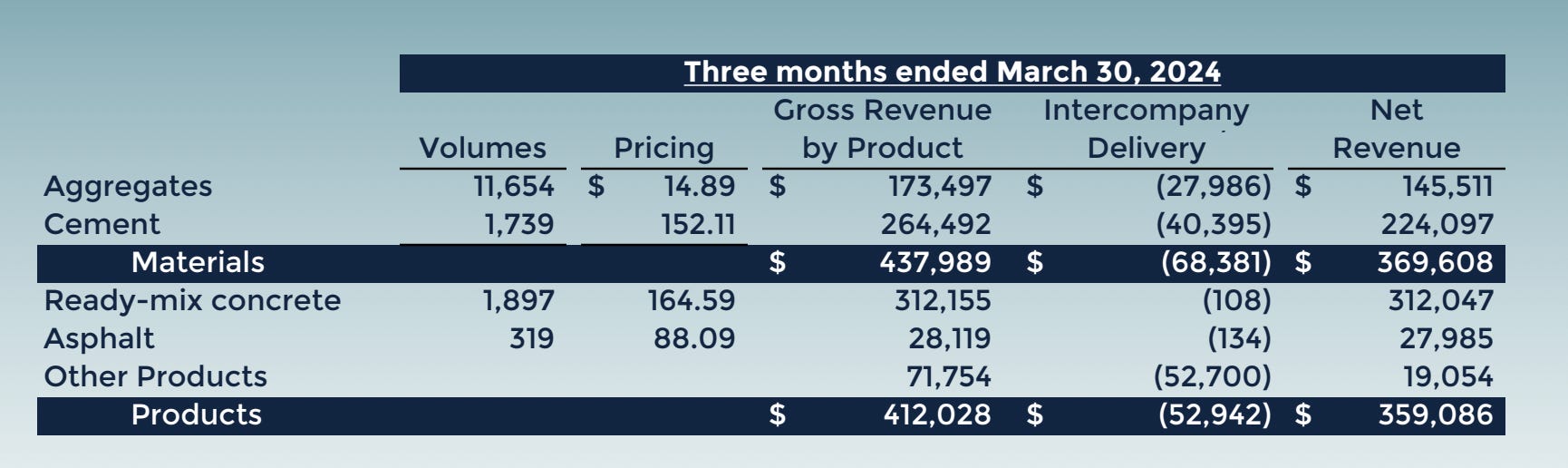

Summit is much smaller than the previous companies. It is a good size aggregate producers and has 6 cement plants. Upstream Aggregates represents about 20% of sales, cement 30% and lower margin downstream product the other half.

Historical sales

Lets compare sales and gross margin for the North American cement and aggregated producers:

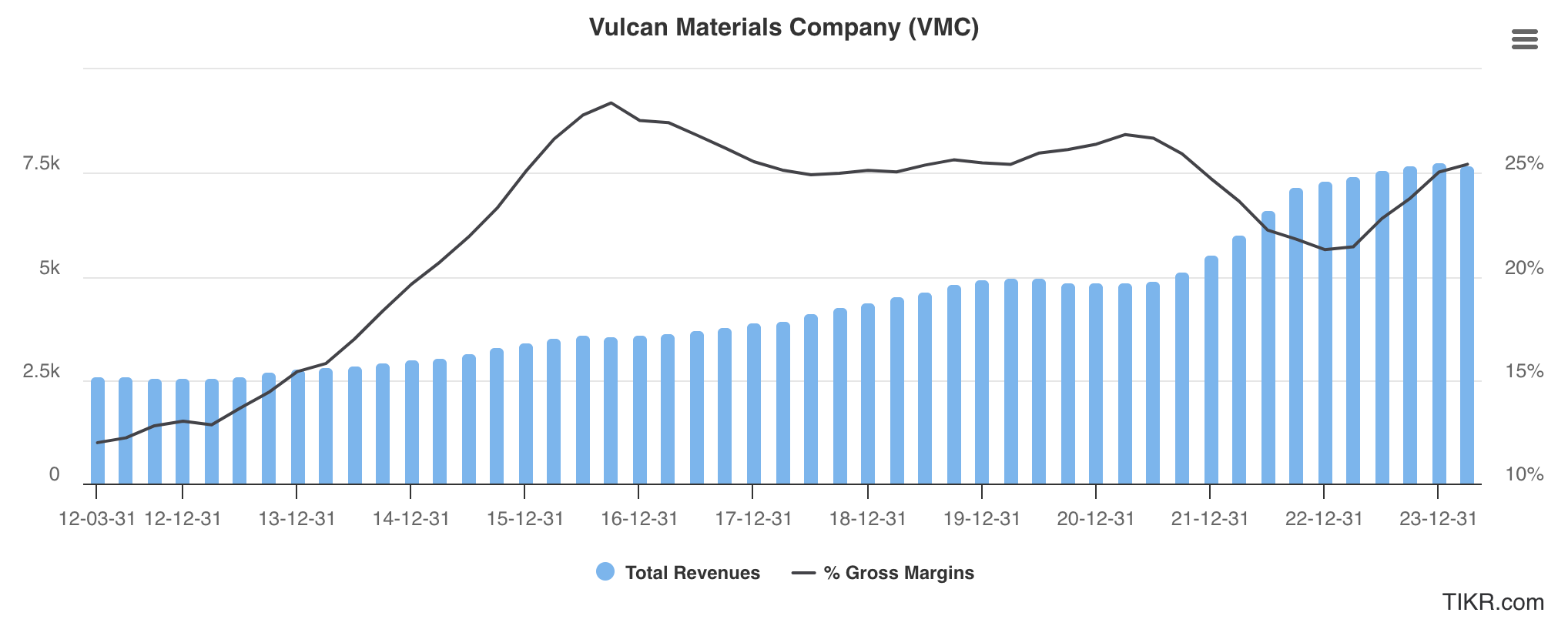

As shown below, Vulcan Materials sales has risen 3x since 2012 in a steady fashion. Sales has steadily risen since 2012 with the exception of a small decrease in sales in 2020 during COVID-19. Gross margin has risen steadily from 12% to 25% in the last quarter. Sales growth has been fueled by 2 acquisitions, Aggregates USA in 2017 and US concrete in 2021.

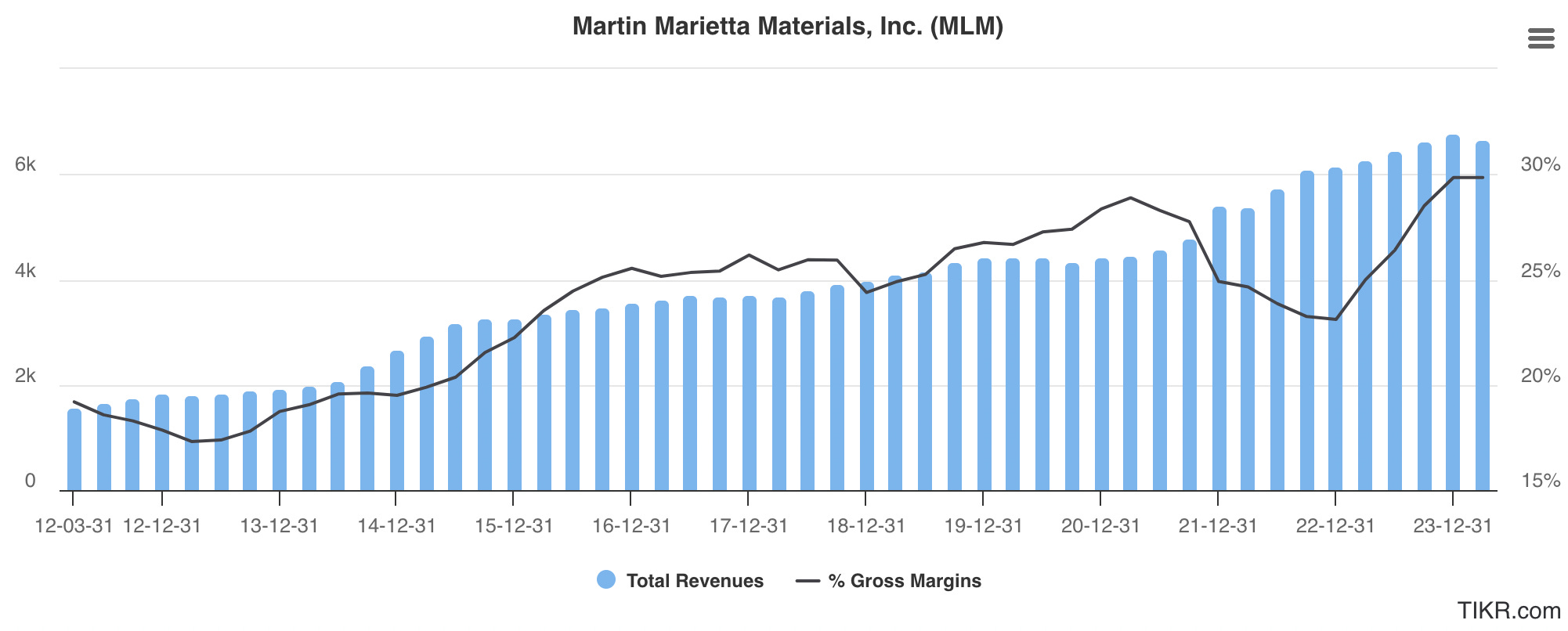

Martin Marietta sales have increases by more than 4x while increasing gross margin from 19% to 30%.

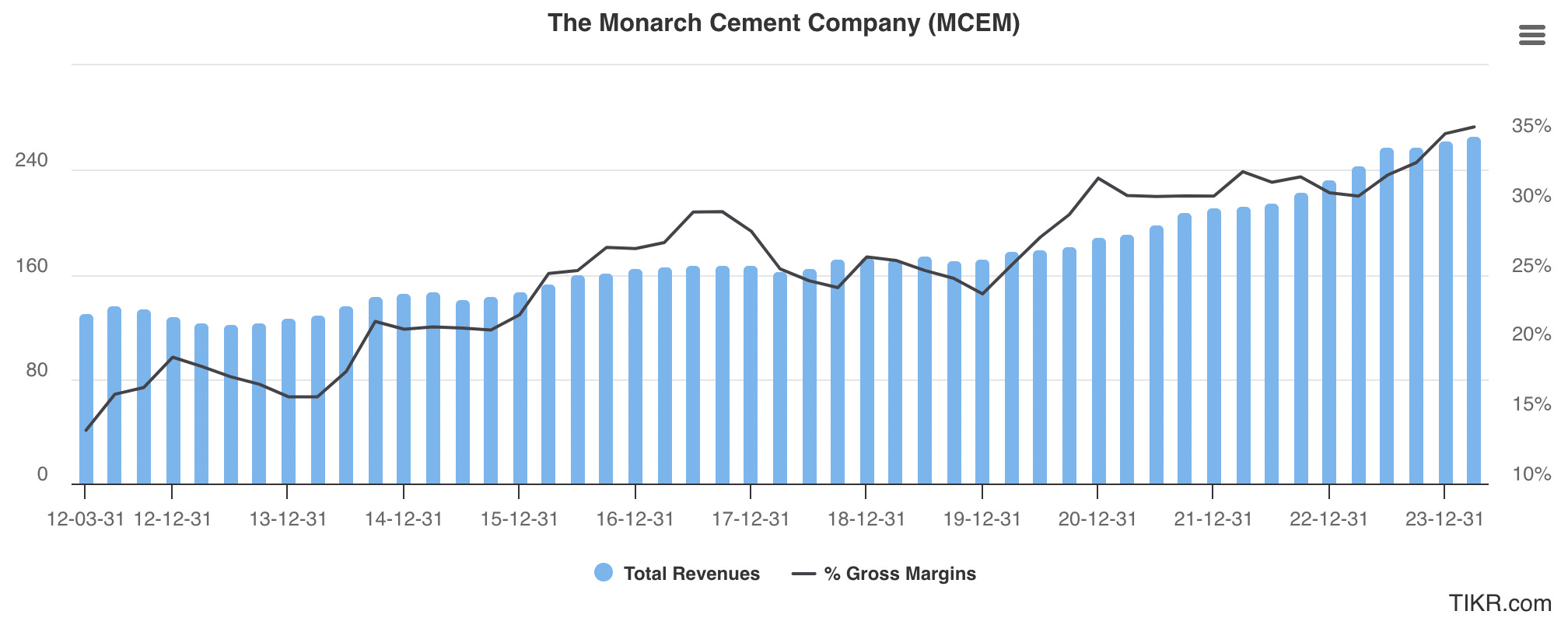

In the last article, we have excluded for Monarch cement the ready-mixed business from the analysis. If we include the ready-mixed business, sales in 2012 was $130M and in the last 12mo, sales were up about 2x at $266M. Gross margin went from 14% to 36% as higher margin Portland cement manufacturing end up being a larger contributor of sales in 2023.

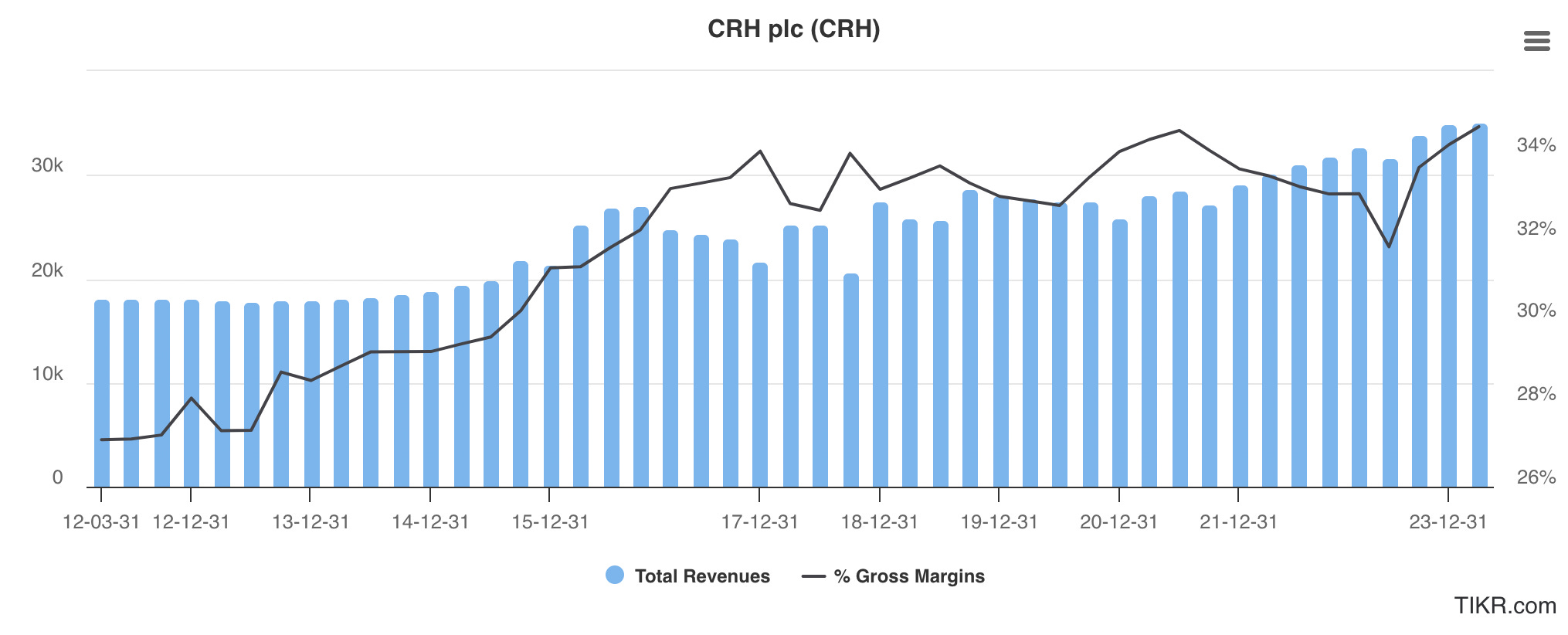

CRH’s Sales has more or less doubled in the last 12 years and gross margin has risen from 27% to 34%. A much smaller increase compare to the other peers.

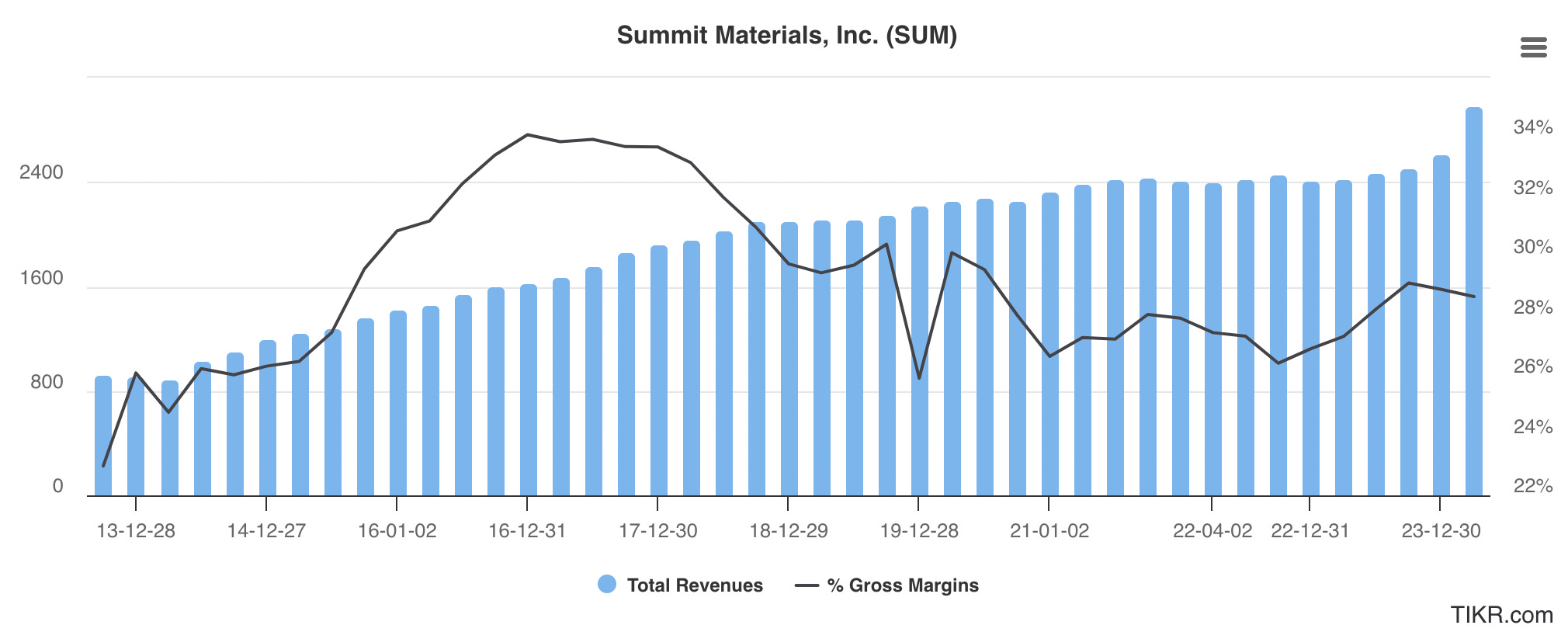

Summit’s sales has more or less tripled in the last 12 years and gross margin has risen from 24% to 28% with a peak of 34%.

Operating Income

Lets compare operating income and operating margin for the North American cement and aggregated producers:

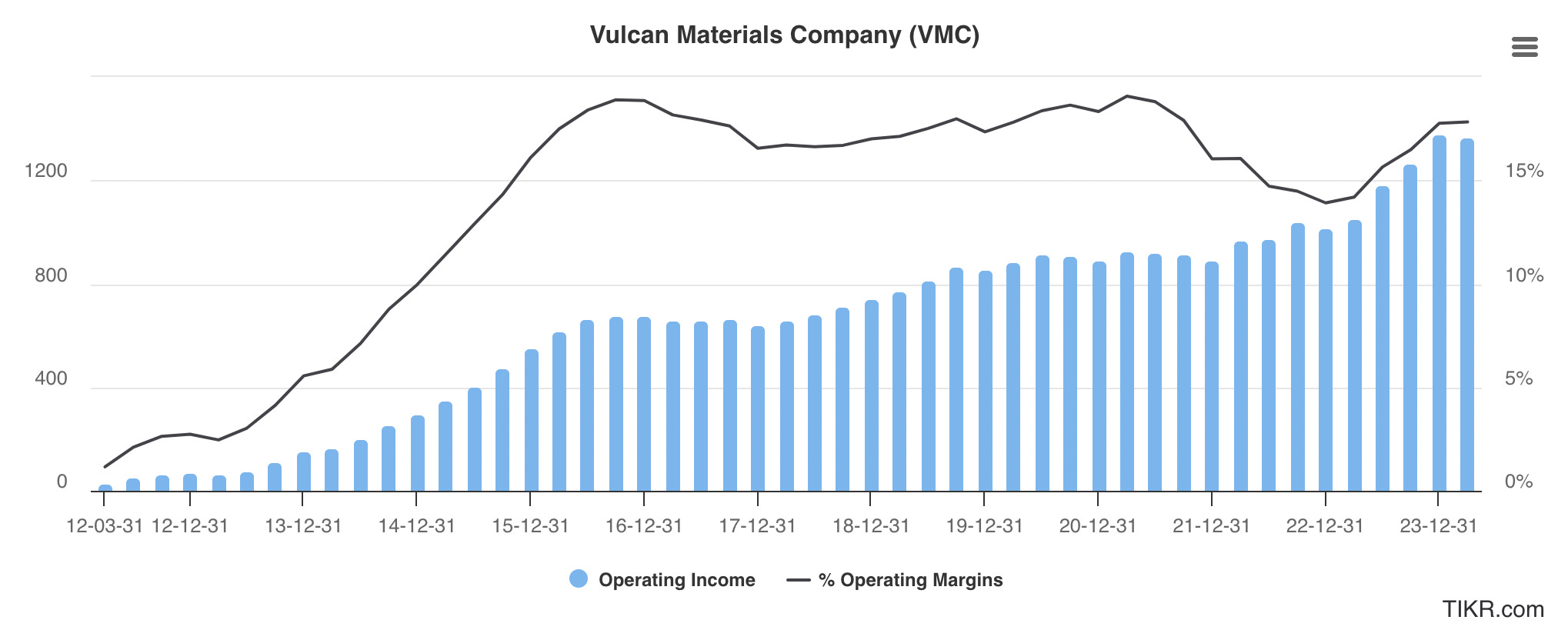

Vulcan Materials’ operating income has grown very quickly as operating margin has risen from a very low 1% in early 2012 to about 17%.

Martin Marietta operating margin started at a higher level in 2012 at around 10% than its peers, and is now at 22.7%. So higher than Vulcan Materials but lower than Monarch Cement.

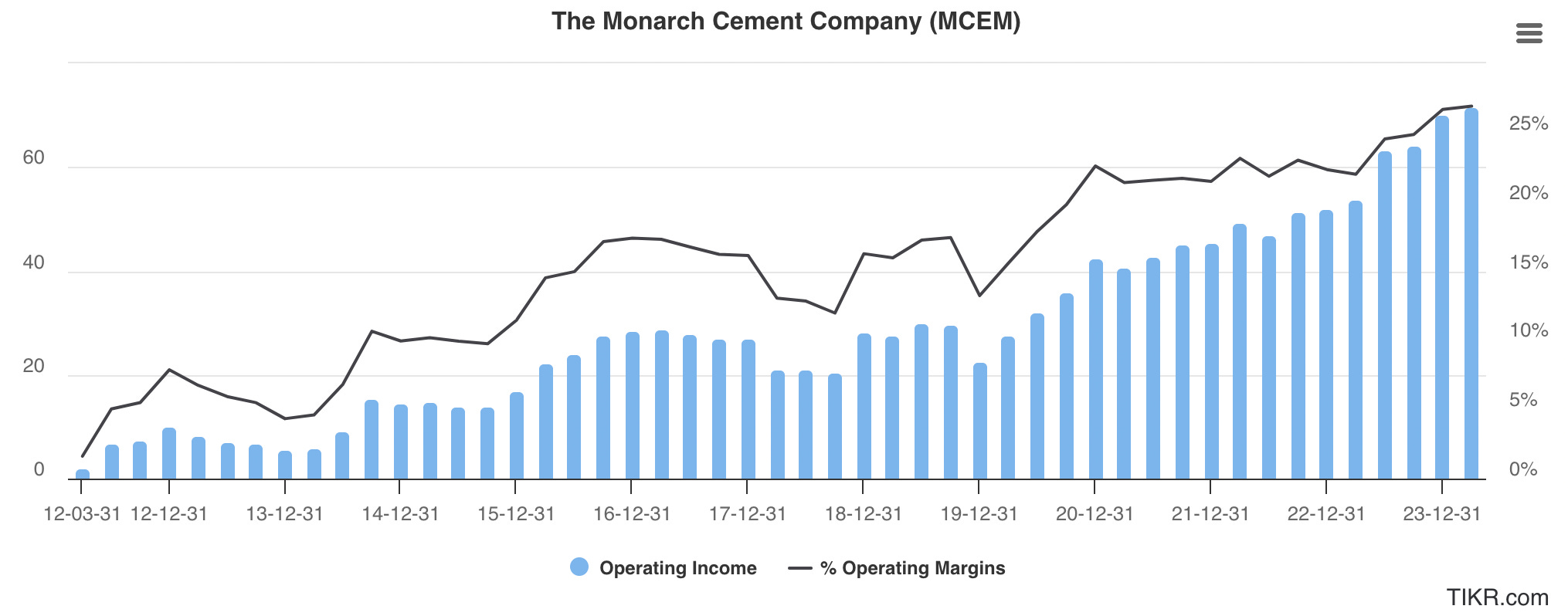

For Monarch Cement, we have a similar trend where operating margin went from 1.6% in 2012 to close to 27% in the last 12 mo. In 2012, Monarch Cement had a construction material subsidiary that was loosing a good amount of money. This subsidiary was close down in 2013.

CRH’s operating income has risen steadily and operating income went from 4% in 2012 to 12% in the last 12mo. Operating income is much lower than Monarch Cement and Martin Marietta.

Summit Materials’ operating income has risen significantly in the last 12 years. Operating margin is around 11% compare to low 1 or 2% in 2012.

Historical EPS

This historical EPS for the NA cement and aggregated producers:

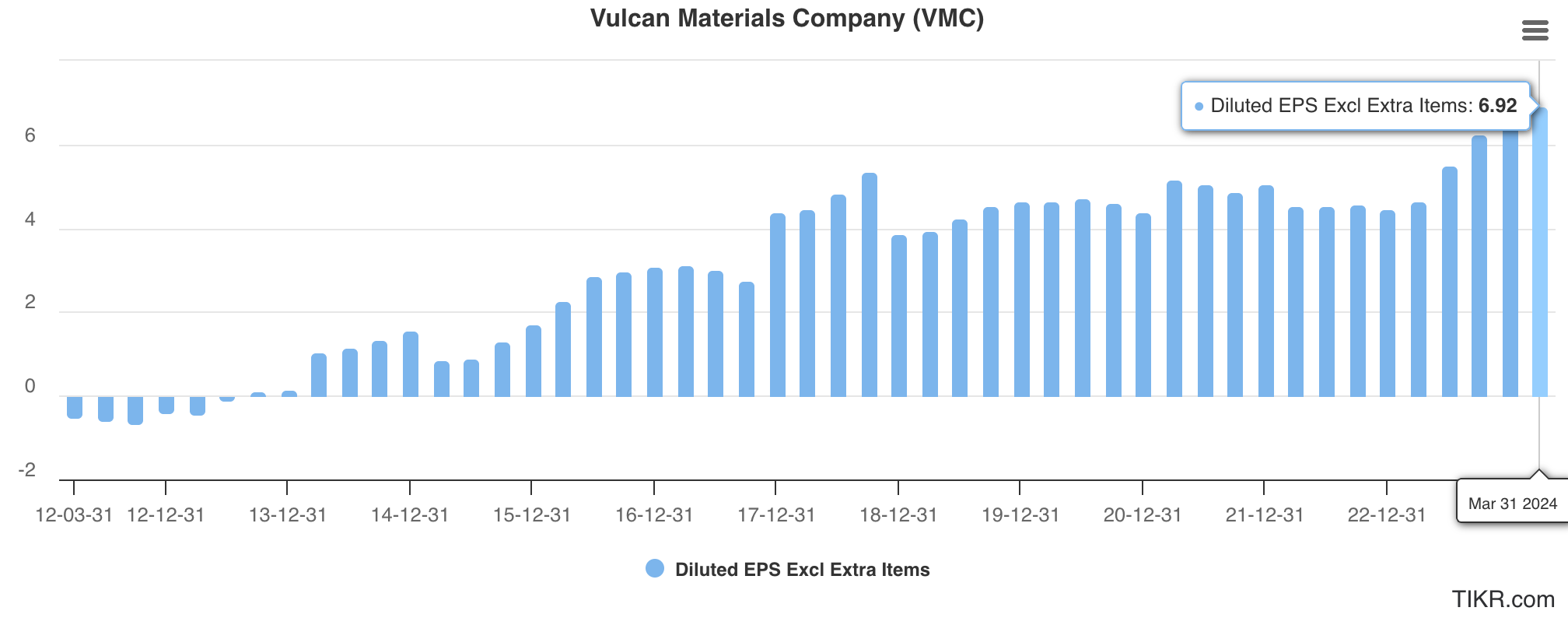

EPS growth for Vulcan Materials has improved greatly from a loss to 6.92$ EPS in the recent 12mo. The stock at 254$ is very pricey at current level, trading at 36x earnings.

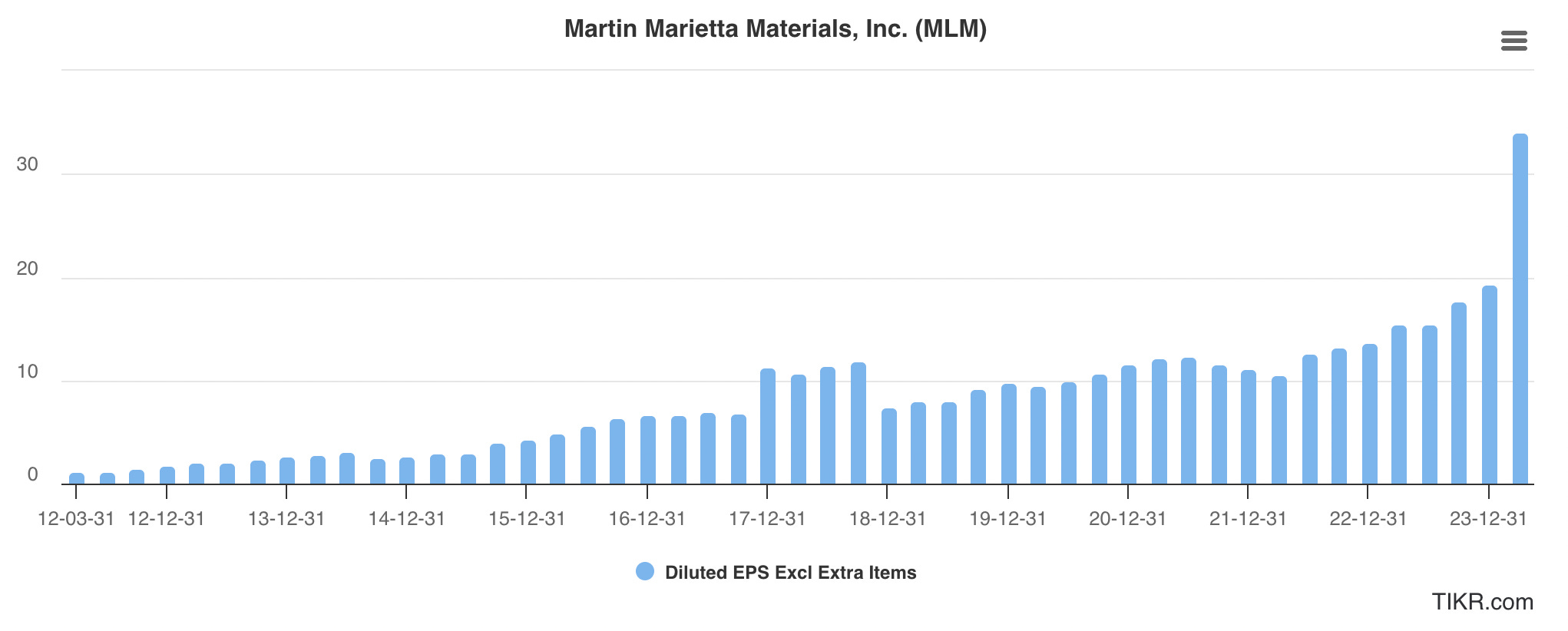

Martin Marietta EPS has jumped to 34$ in the last 12mo due to the asset sale of the South Texas Cement plant and ready-mixed for a gain of $1.3B. Without this extraordinary gain, normalized EPS is around 19$. So the stock is trading at about 29x earnings. A bit lower than Vulcan Materials.

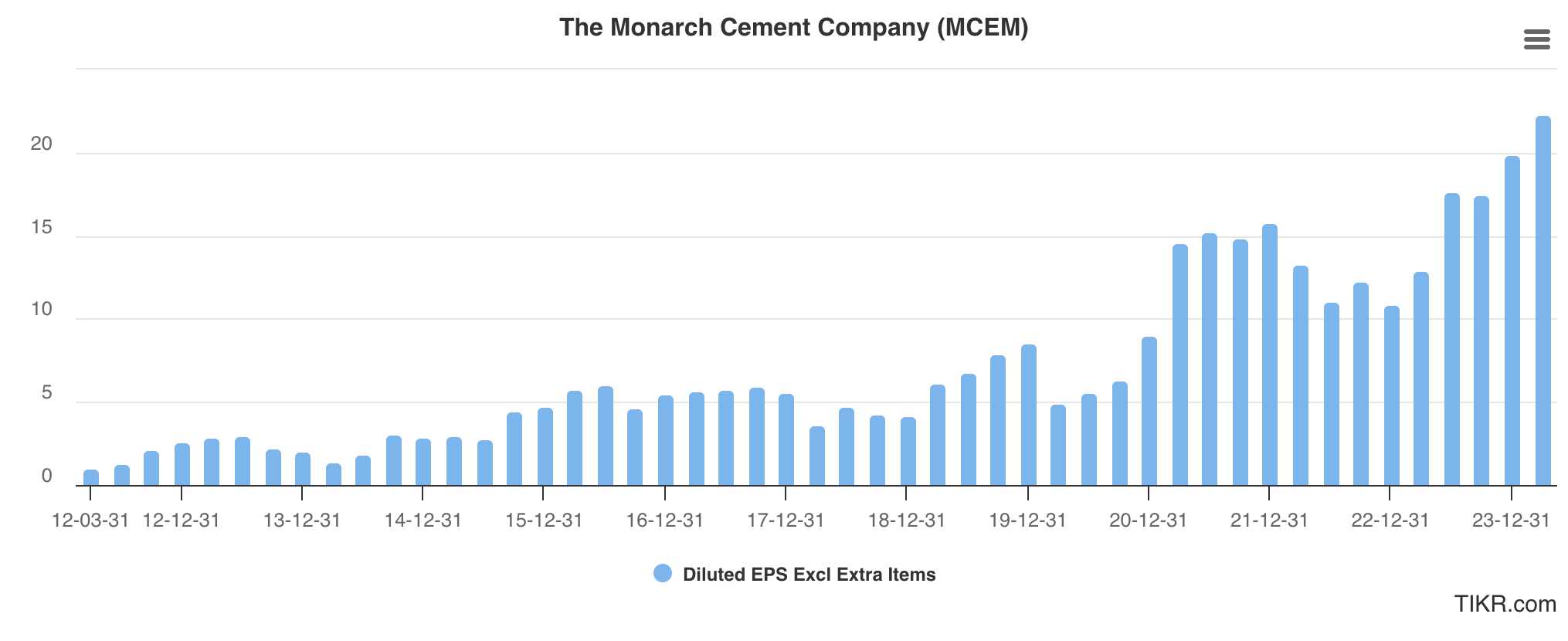

Monarch cement’s EPS has reached 22.32$ in the last 12mo, the stock at current price of 196$ is trading at very low PE of 8.8. The equity holding is performing very well right with large mark to market gains so now so it is contributing strongly to net income. As such, a more conservative valuation criteria would be to use EV/EBIT ratio which excludes mark to market gains from the equity holding. The equity holding value is subtracted from the market cap but the fluctuation does not impact the operating income (EBIT).

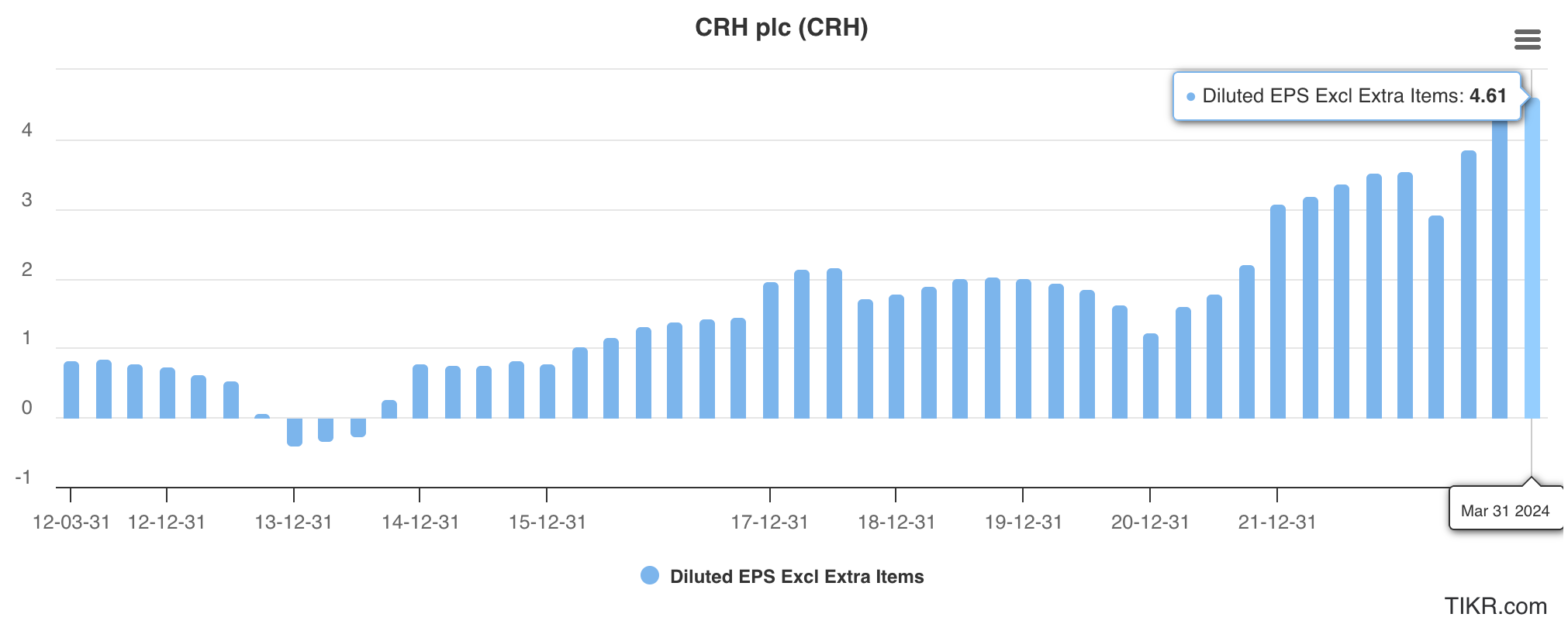

CRH’s EPS has reached 4.31$ in the last 12 months. The stock at the current price of 81.73 is trading at 19x earnings.

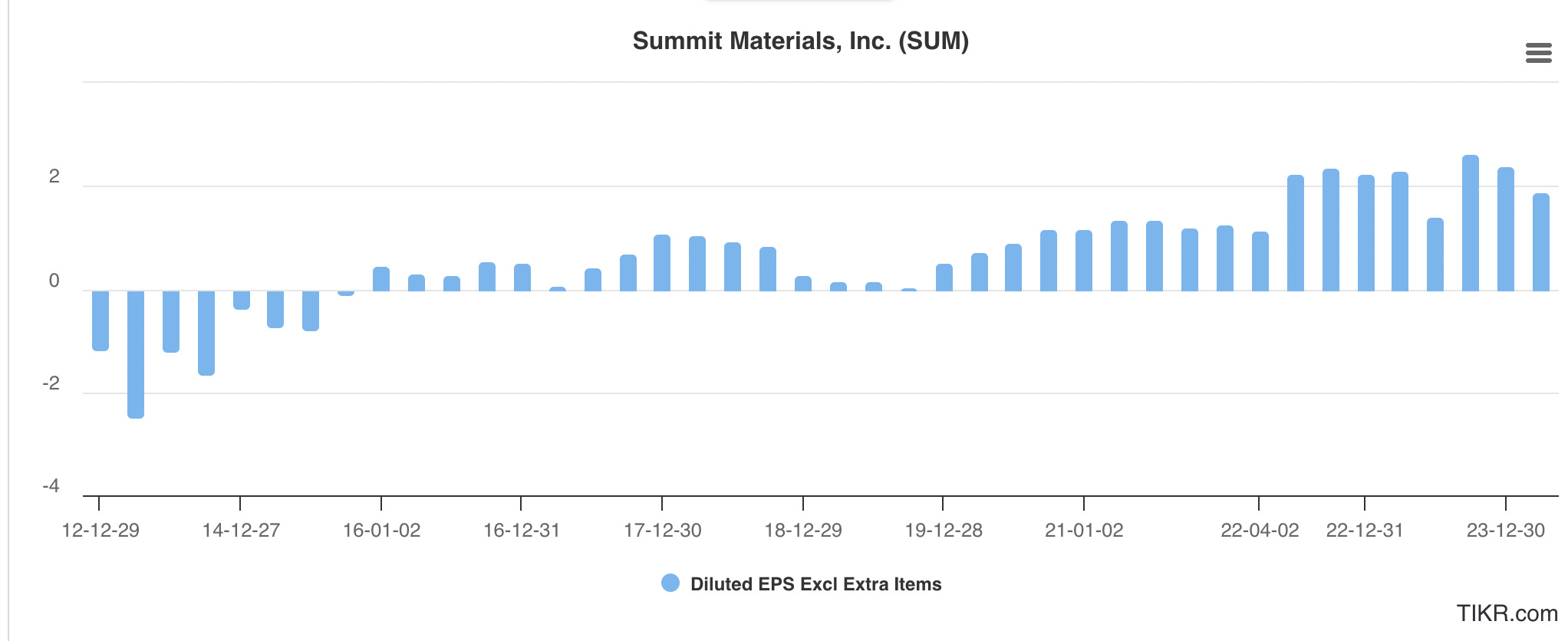

Summit Materials’ EPS has reached 2.39$ in the last 12mo and the stock is currently trading at 16x earnings.

EV/EBIT

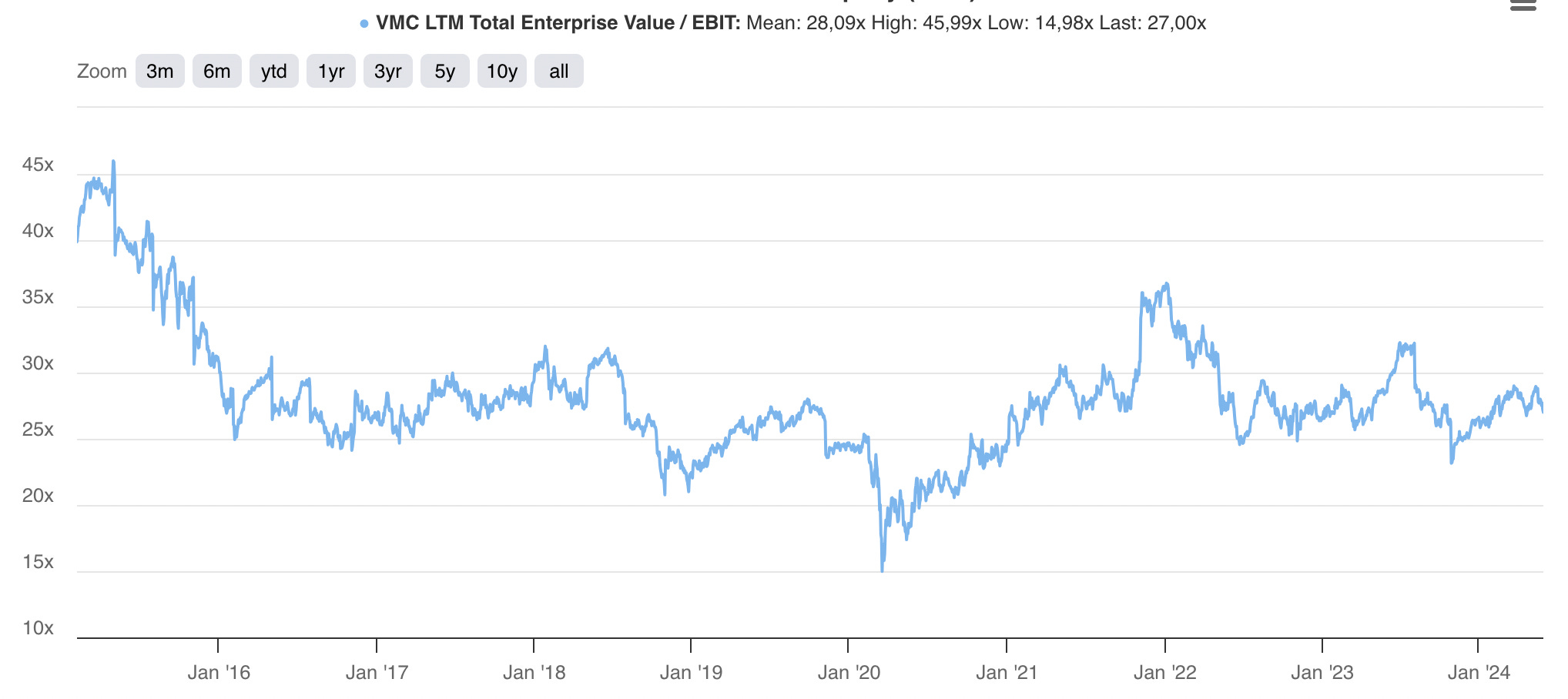

Using EV/EBIT ratio, Vulcan Materials has been trading historically at a mean trading range of 28 and now at 27 so it is trading somewhat lower than to the mean.

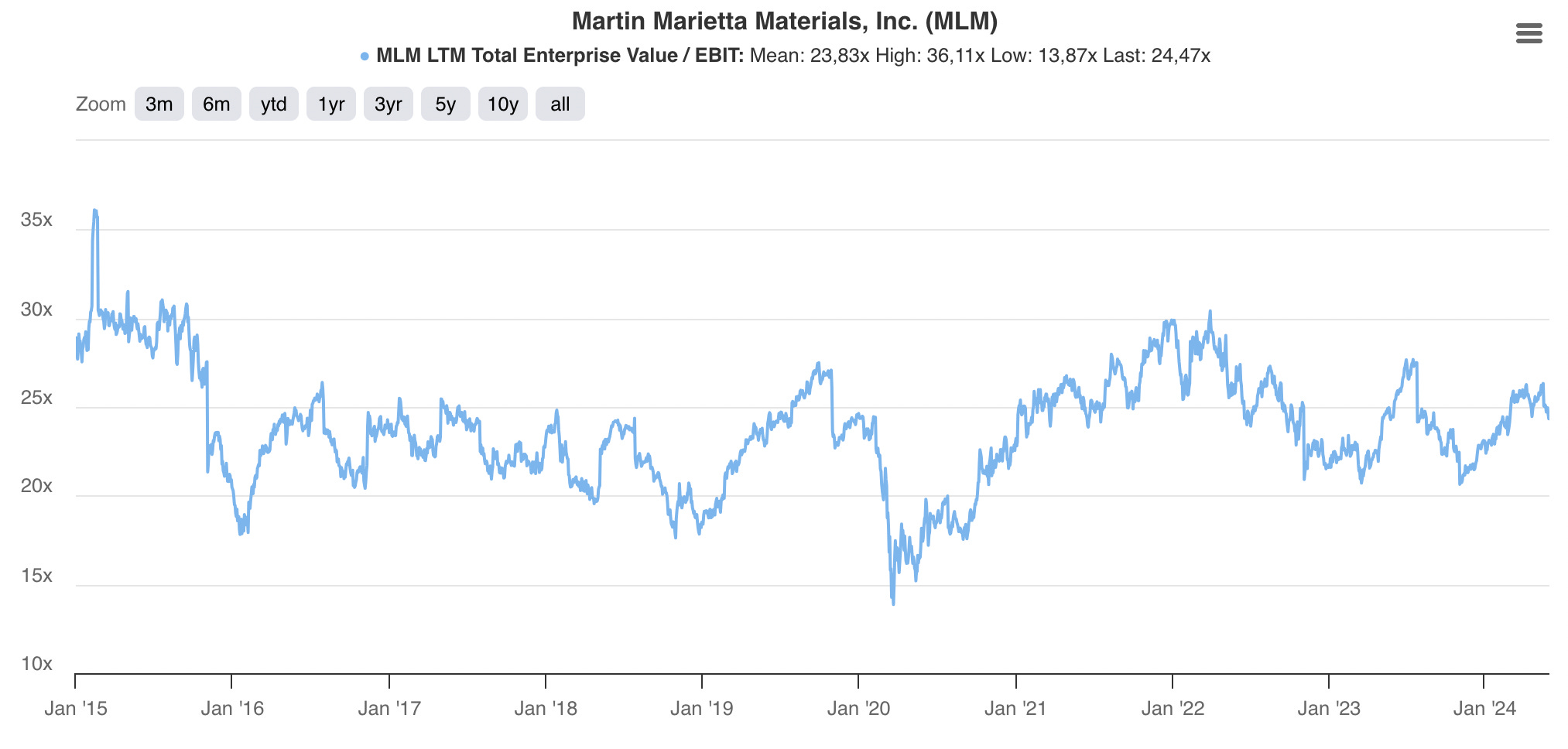

Martin Marietta’s has been trading at a mean trading range of 24x and it is currently trading at around that ratio.

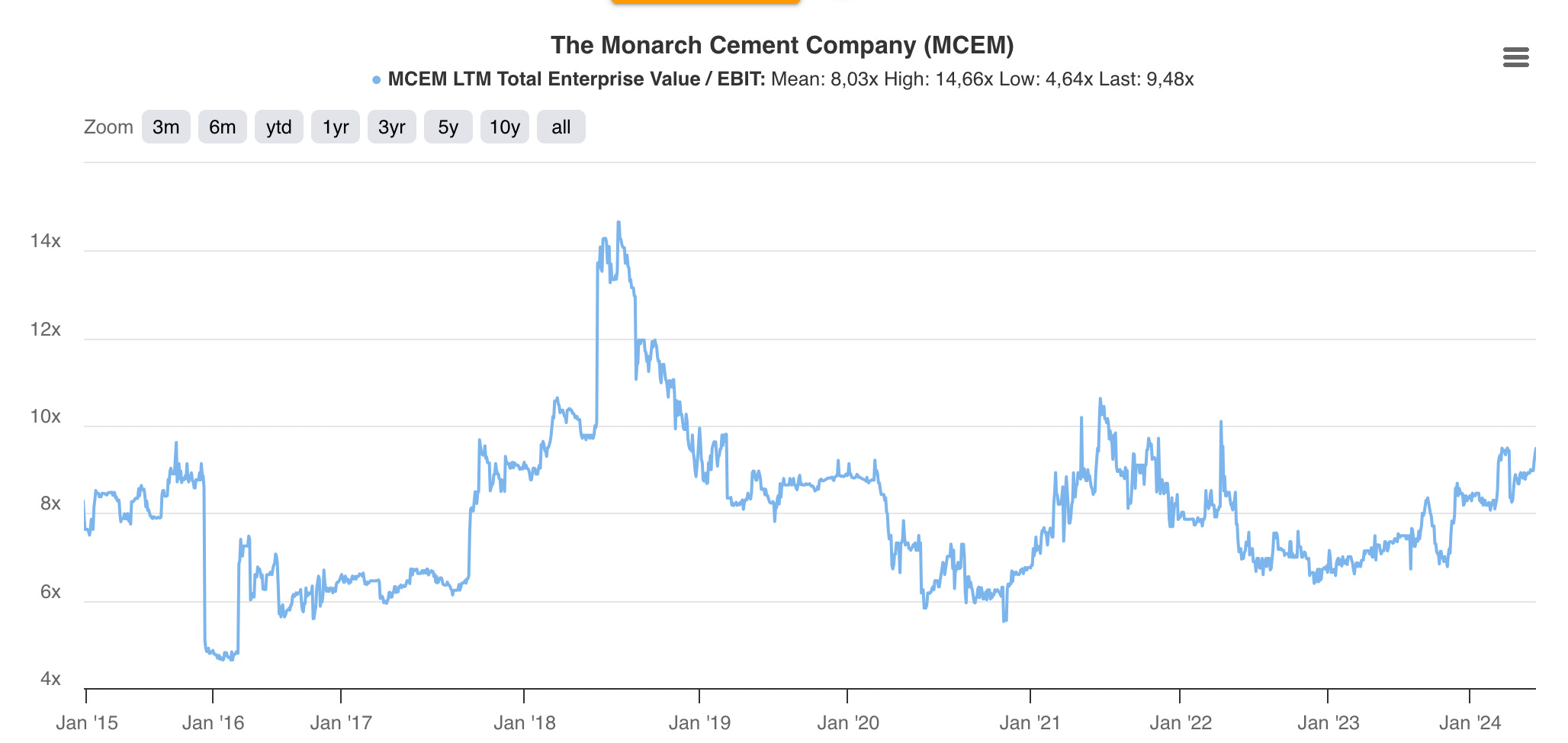

Using the same ratio, Monarch cement has been trading at a mean trading range of 8x EV/EBIT. It is currently trading at 9.5x using TIKR. However, the 80m equity holding should be removed from the market cap to calculate the EV. As such, EV/EBIT is 8.3x earnings.

Using the same ratio, CRH has been trading at a mean trading range of 16x EV/EBIT. It is currently trading at 14.6x, so somewhat lower than the mean.

Using the same ratio, Summit Materials has been trading at a mean trading range of 21x EV/EBIT. It is currently trading at 26x, so much higher than the mean.

Summary

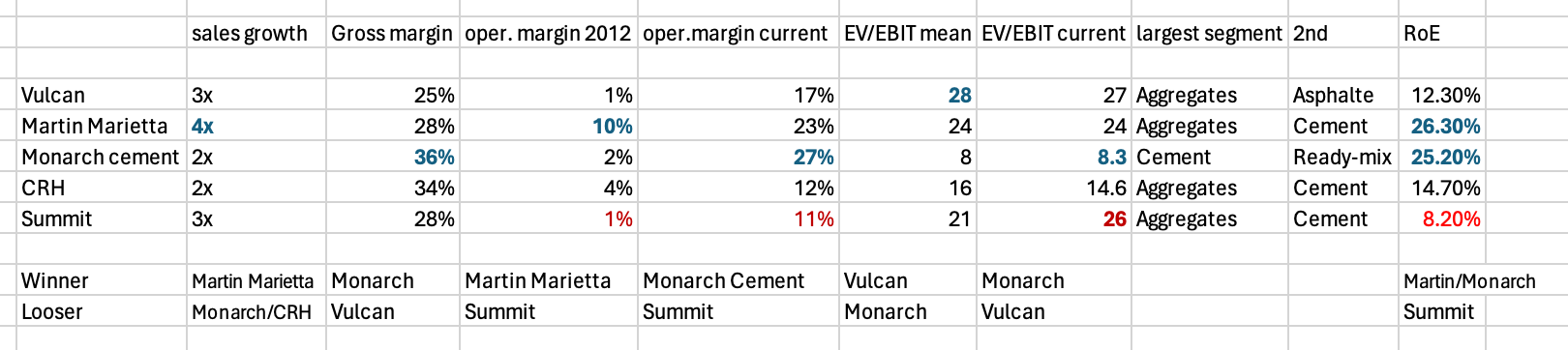

I summarize the operating performance and valuation criteria discussed previously in the following table. I also added the shareholder yields:

In terms of sales growth in the last 12 years : Martin Marietta ranks first while Monarch and CRH are last. Monarch is all organic while the other larger companies like Martin Marietta and Vulcan are growing through acquisitions.

The best gross margin is achieved by Monarch cement followed by CRH. This can be explained by higher gross margin typically achieved from portland cement manufacturing.

The best operating margin was again achieved by Monarch cement followed by Martin Marietta. The lowest operating margin is from Summit.

From a quality perspective, I would rank both Martin Marietta and Monarch cement on top in terms of quality. Martin Marietta is growing fast and seems to be making very good bolt-on acquisitions and divesting under-performing assets. Those acquisitions has fueled a higher growth than Monarch Cement. Monarch Cement has been laser focus in growing organically and optimizing its single cement plant, which have lead to generate the best gross margin and operating margin accross its peers. Both Monarch Cement and Martin Marietta have RoE of 26% and 25% respectively. This is almost the double of Vulcan and CRH.

In terms of valuation, the pure plays aggregate producers (Vulcan and Martin Marietta) are trading at the highest valuation historically - mean EV/EBIT of 28 and 24 respectively. The Street is willing to pay premium to the less cyclical aggregate producers. They are currently trading close the average.

Based on this, Monarch Cement is trading at large discount to peers based on the relative low EV/EBIT of 8.3 and based on the steady organic growth of its cement plant and its best of class operating margin. Considering the attractiveness of the infrastructure industry in US, this company deserves to be rerate to a higher multiple. The rerating has started already (trading higher than the average of 8x EV/EBIT) and I would not be surprised to see continued rerating over the next few years.

In second, I appreciate the high quality and impressive growth of Martin Marietta. Martin Marietta is trading at a lower multiple than Vulcan, and has a better margin and better growth than Vulcan Materials. It is fairly priced compare to historical valuation, so rerating is probably unlikely. Still operating income growth could be interesting over the next 3-5 years.

Summit materials is of relative low quality and is trading at a high EV/EBIT so less attractive.

Cheers!

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested

Great article! You probably know this already that Holcim plans to spin-off their North American division: https://fortune.com/2024/01/28/cement-giant-holcim-to-spin-off-north-america-unit-construction-boom/#:~:text=Holcim%20Ltd.%2C%20the%20world's%20largest,Gutovic%2C%20as%20chief%20executive%20officer.

One more peer to look into, although with a shorter history.

As a shareholder in Monarch for about 18 months I very much appreciate your write ups on the company and its industry. They are excellent. You have expanded my knowledge considerably.

Several points to add from my perspective.

Monarch is a multi generational founder led company. i suspect they will continue to stay that way. That means they have a long term perspective in all of their actions and relationships. They indicate a win, win , win attitude in their business. Which i like. This begs the question though have you or any other readers met their leadership team? And if so what are your impressions?

Also what are the senior leadership team employment packages including incentives?

They have a sizeable share investment portfolio How skilled are they over time at investing shareholders surplus capital in the equity markets? Or should they be giving it back to shareholders through dividends ?

Thanks

Geoff