Interesting times! David or Goliath

Interesting times! David or Goliath

High quality stocks or franchise have come down significantly $MTD $RCO.PA $THEP.PA DSV.CPH

Company with moats or franchise have come down significantly recently with the recent correction including large caps. This is an interesting time to double down or initiate a position in what was “too expensive of a stock”. Here are a few ideas small cap, large cap I dont care, if it is lower I am interested.

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

MTD 0.00%↑ Mettler Toledo

One compounder with EBIT operating margin of 30% is the world leader in industrial scale Mettler Toledo - $MTD. This is large cap territory. I have owned this one for many years, but I sold at some point went it reached 40x+ PE. Now it has come down to 24x.

What I would like to do is compared it with another small cap favorite Precia..also in the business of industrial scale. Precia has EBIT margin of 7-10%. Scale has some intrinsic advantage. Precia is priced at a lower multiple but still which investment is best? If we go into a downturn, a 5% drop in margin will impact much more Precia than MDT. A David against Goliath comparison.

DSV A/S

Another David against Goliath would be to compare DSV with Clasquin. DSV is the best asset lite freight forwarder if you look at the last 20 years. Conversion ratio (EBIT/Gross Profit) has reached 50% in 2022. Clasquin is nowwhre close to that. And now that the stock got hammered - should we go with DSV or keep our shares of Clasquin?

Spirits horribilis

The best franchise of Spirits companies got hammered in the recent month. These are amazing franchise unreplicable and considered sin stocks so very robust even in the upcoming recessions. “When you can’t travel because you lost your job or risk loosing your job, or have seen your mortagage going up by a thousand $, you certainly need a nice drink!”

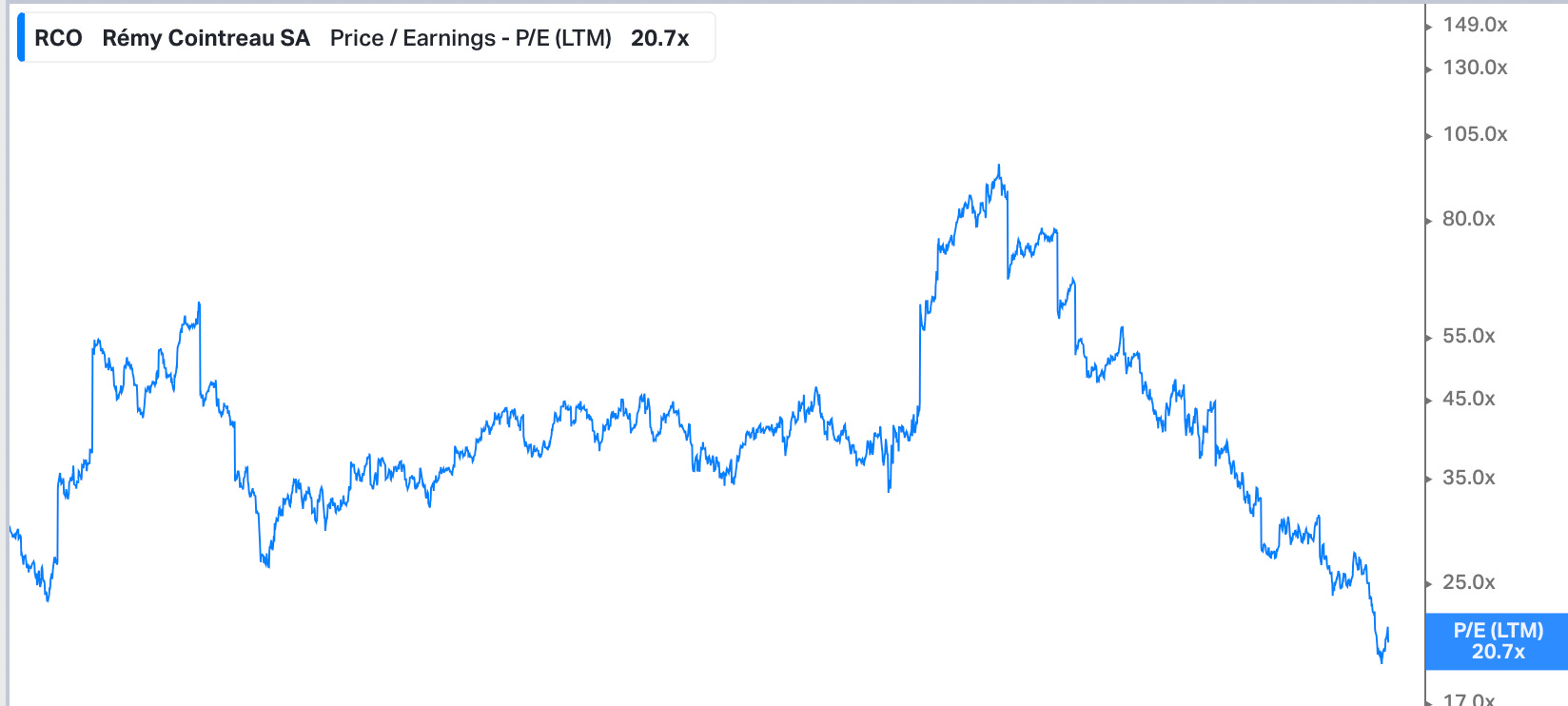

You just need to look at the best cognac brand of this world - Remy Martin.

This stock hasn’t traded below 20x PE for a very very long time.

The much larger Ricard or Diageo - The Goliath names - also have come down. Should we buy a bouquet of those. Or zero in smaller name like $RCO or another. I would feel much better holding a good amount of my portfolio into those sin stocks while waiting for the US economy to do the inevitable - no I dont think this time is different - hard landing in 2024, or 2025.

$THEP Groupe Thermador

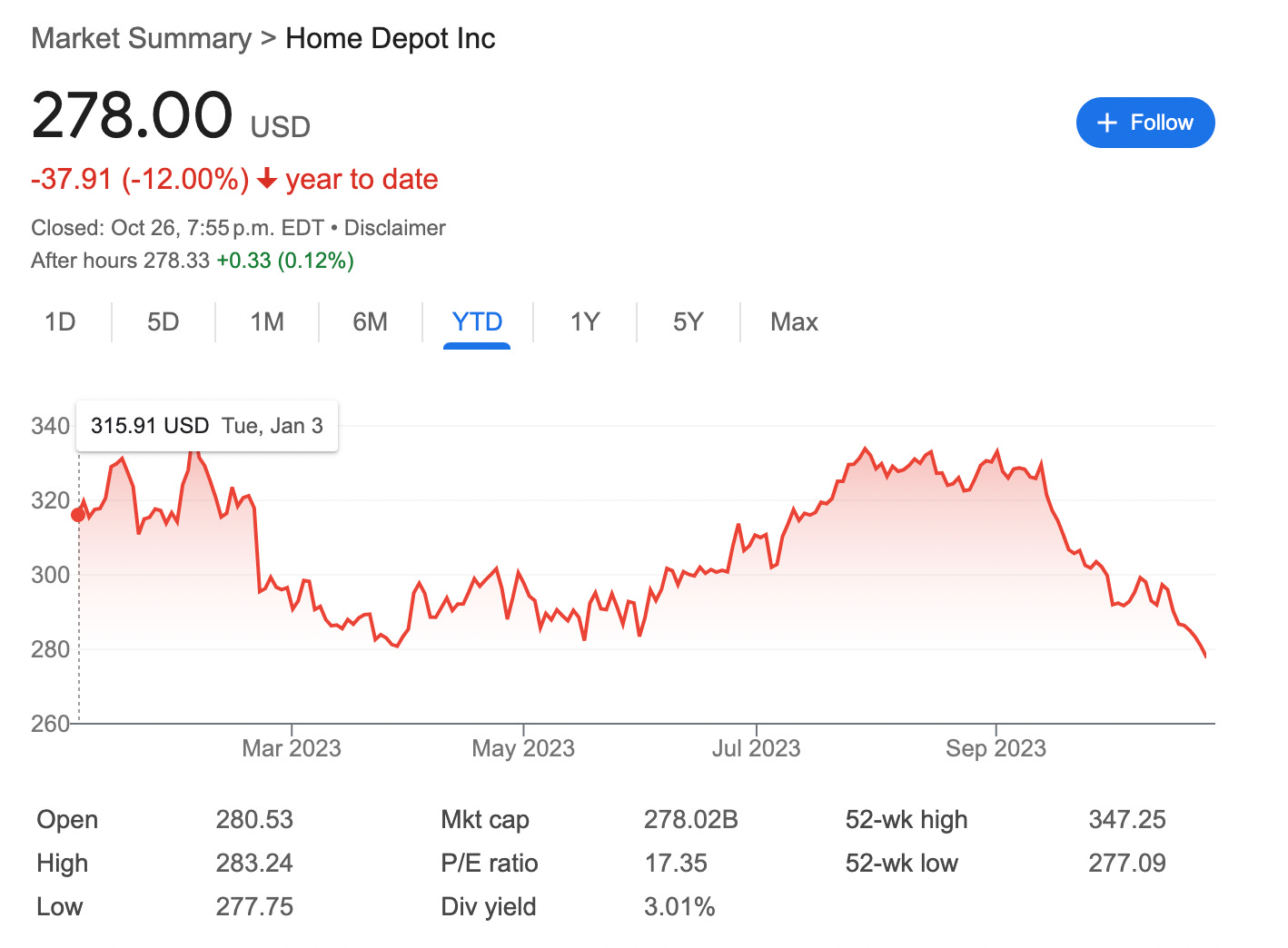

Small cap Compounder like $THEP have been down significantly due to fear of the recession impact. Is this a good investment? Should we double down and add more share - this is a #10 position for me. Or should we invest in large cap distributors or manufacturers like $HD, $MASCO, FERG 0.00%↑ in the same industry.

or the much smaller French peer samse

Conclusions

I may or may not expand on these topics over the next few weeks. But this is the analysis I am doing right now. The main message here is that small cap, large cap should not be a religion. In times of trouble, one can find value in both. And large cap have implicit scale and moats that protects it in difficult times.

Feel free to provide some comments. I really like the idea of doing some David against Goliath comparison, a peer comparison between a small cap and a large cap operating in the same industry. so expect some posts over the next few weeks on this.

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested

gd reminder on some names!