Japanese Stocks Series Part I - Yamada Corp $6392 a pump manufacturer cash-rich low PE growing mid single digits

Japanese Stocks Series Part I - Yamada Corp $6392 a pump manufacturer cash-rich low PE growing mid single digits

This is PART 1 of the Japanese Stock Series focused on Yamada Corp, a leading manufacturer of Air Operated Double Diaphragm pump

Background - Japanese Stock Series

Strategy: The Japanese stock market have been a fertile ground to find attractively priced stocks of good business with cash rich balance sheet.

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

I have a starting position on 10+ Japanese stocks that exhibits the majority of the following criteria:

1) Bullet proof balance sheet with net cash>25% of market cap and little debt

2) Robust and good business

3) Attractive operating income yield compare to peers

4) Lt Rev and EPS growth

5) >10B yen cap

The main objective of the Japanese series is selfish. I want to spend the next few months studying those promising Japanese stocks and decide whether I want to increase my position, keep those as starting position and monitor or sell.

I am not new to the Japanese stock market. I have owned franchise like Fanuq, Shimano and Nintendo but also net net. One think I learned is that I have difficulty owning a slow melting ice cube even if cash is 2x the market cap. As such, the second and third criteria are very important for me. The business need to be easy to understand and in an industry that I like, that I know and that should have good prospects in the near future.

The attractiveness of the operating income yield is key as I want to earn superior returns in this foreign country. If I can find a similar business in Europe and US at a similar price, I need to pass. This is Japan.

I can be very patient if I see the business progressing years after years slowly but steadily. So exhibiting some growth is an essential criteria.

The 10B yen cap is more opportunistic. This is an arbitrary number to hope for some liquidity and for some activist to come in. 10B yen of tradable securities is also also the limit to be eligible to trade in the Prime market. Yamada corp trades in the standard market (not Prime) so this is a major factor.

The Yen Factor

I have no clue whether the Yen will continue to trade lower or reverse course and trade higher over the next few years, but this is not a factor. The reason being that I am yen neutral in my account, i.e. all my purchase in yen is done on margin which my broker currently charges me a blended 1% to 1.5%. I can invest in low risk arbitrage opportunity that will give me much better than this rate (like Logistec) or let the equivalent in cash sit in USD which gives me 4-5%. This is a great deal. Say I invest 20B yen, my Yen balance shows 20B of debt but I own around 20B of equity in Yen.

Yamada Corp $6392 Overview

Yamada makes industrial pumps (62% of sales worldwide), automotive equipment for repair shops (25% and only sold in Japan) and aftermarket parts (12%). Yamada’s main product is the air operated double diaphragm pump (AODD) and is a leader in that field.

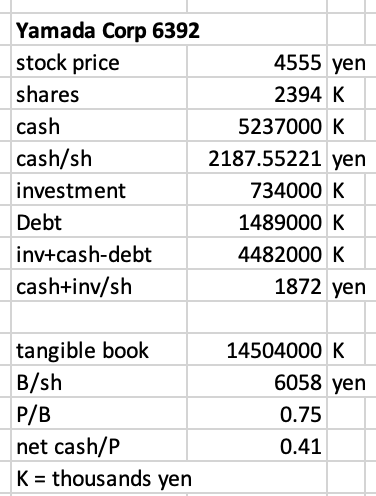

Criteria 1: A Bullet Proof Balance Sheet

As a shareholder of Yamada corp, you get an outstanding margin of safety. Each share holds 2187 yen of cash and short term investment. If you sum up the cash and long term investment and subtract the long term debt, you get 1872 yen per share or 41% of the current market price. The owner is also protected by other tangible assets. Tangible assets includes its flagship Sagamihara plant near Tokyo completed in 2022. The company did take some debt to construct the new plant but have been paying the debt at a rapid pace. Tangible book per share is 6058 yen. This results in a price to book of 0.75.

The following image shows the new Sagamihara Fab. where the industrial pumps are manufactured.

You can watch the video in the following link for a site visit:

Criteria2: The Business

Yamada splits its sales into 3 segments:

Industrial Pumps: They sell more than 150 different pumps, the majority of which are AODD pumps.

Automotive: Basically car maintenance equipments mostly used by automotive repair shops in Japan.

Aftermarket: Service parts and Repair services of the industrial pumps adn automotive segments.

Industrial Pumps Segment

62% of the sales related to industrial pumps which are sold worldwide. In that segment the main product are air operated double diaphragm pump or AODD.

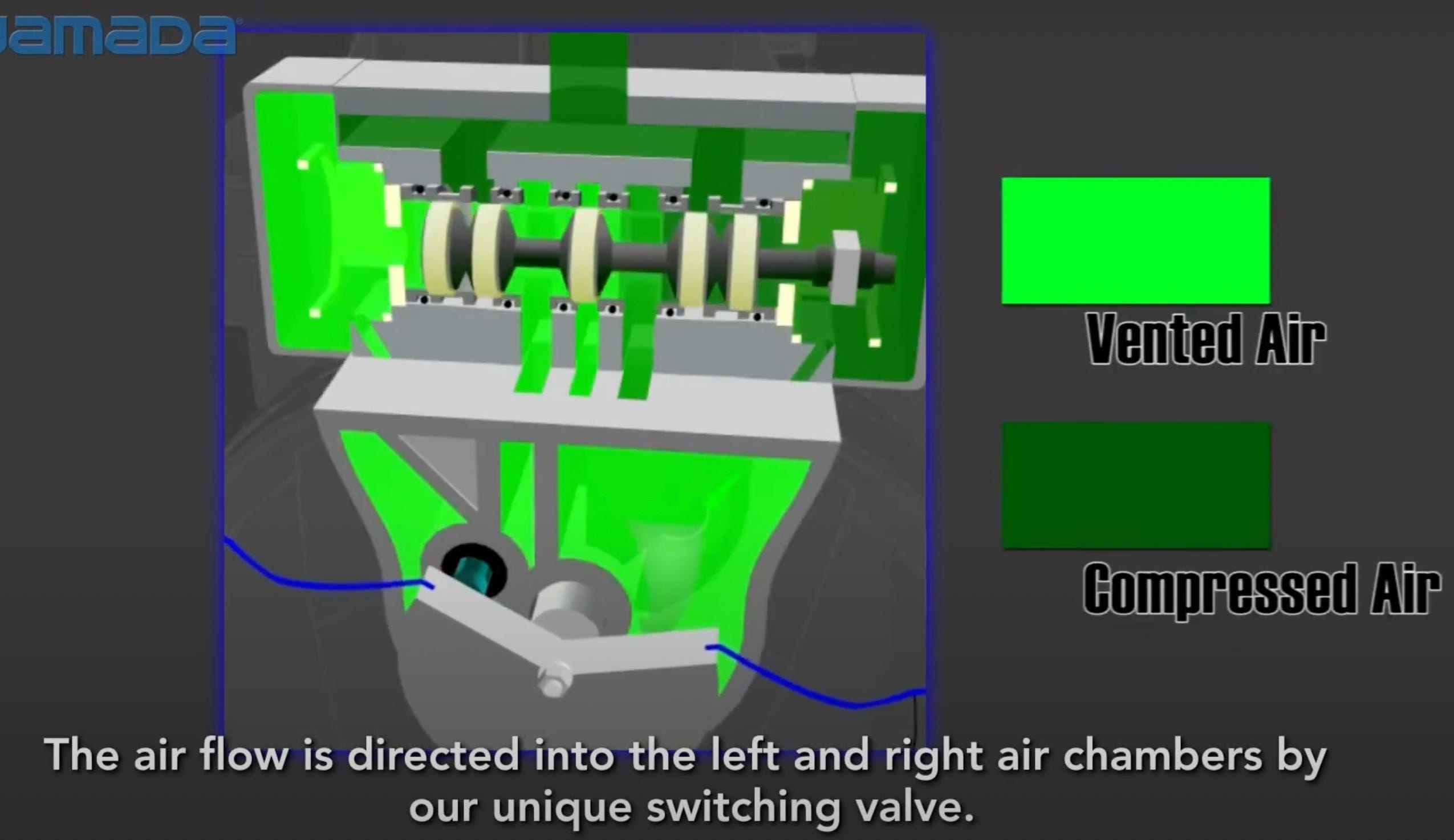

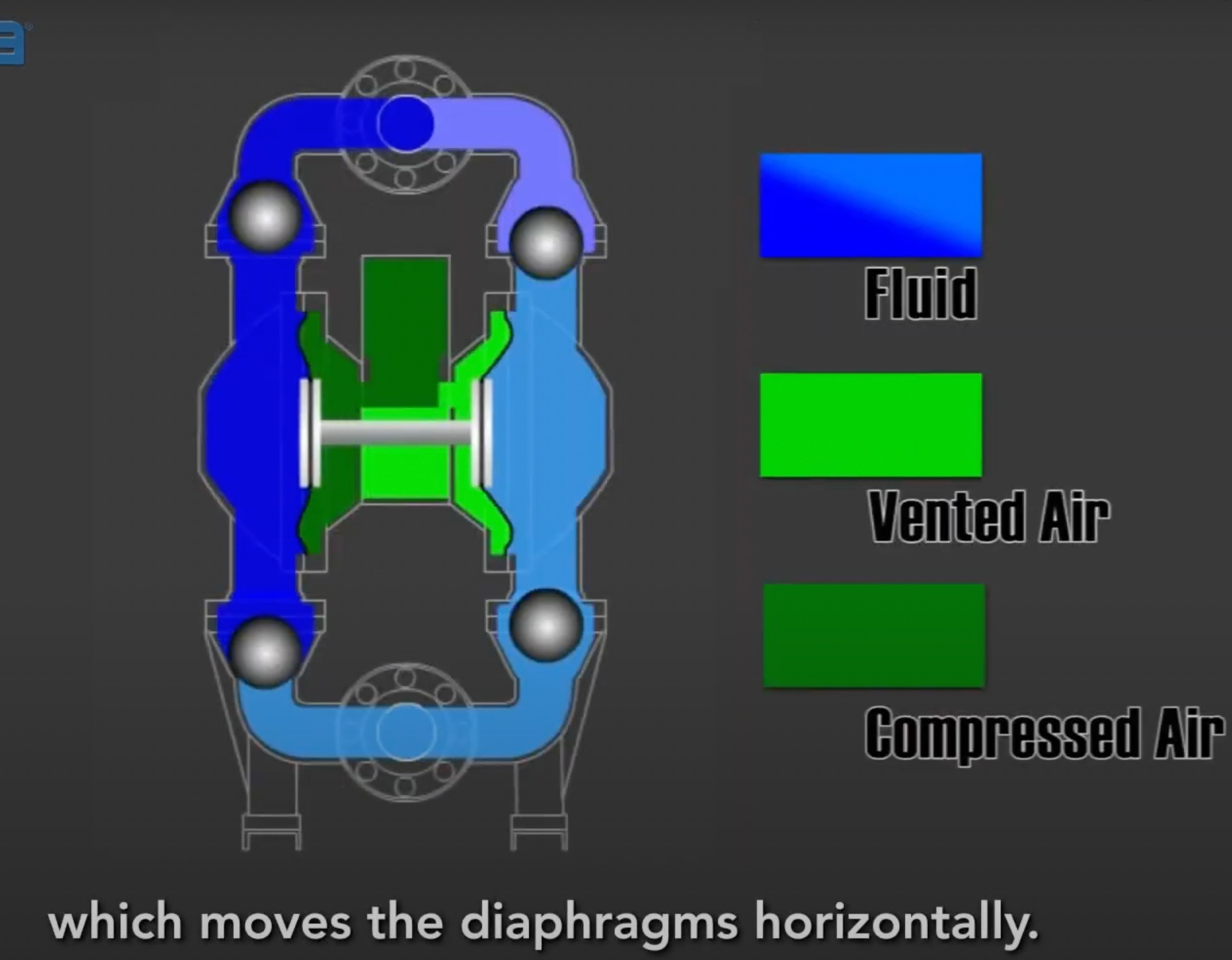

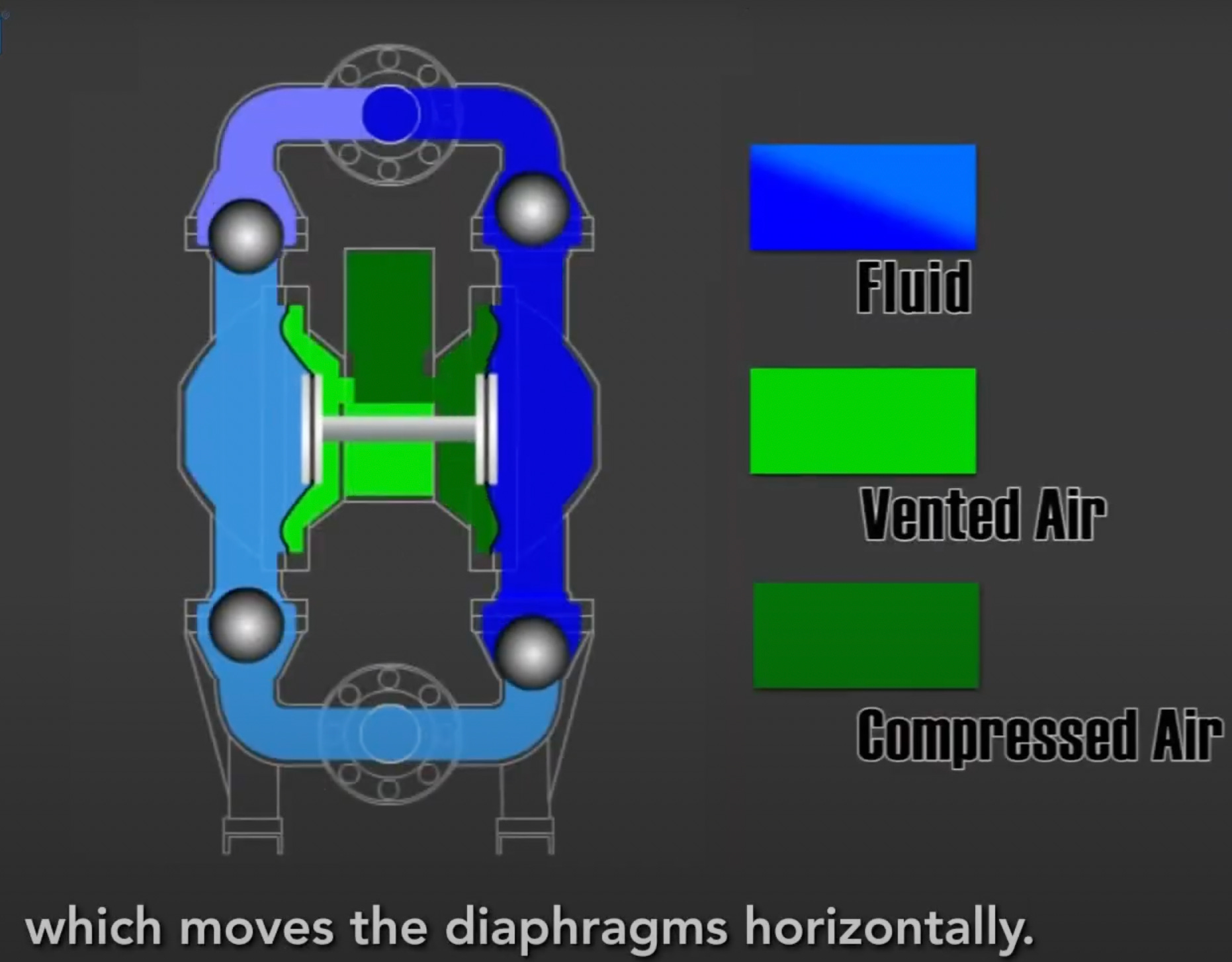

AODD pump is a pneumatic pump that directs compressed air between two sides of the pump, back and forth.

This air valve switching pushes compressed air behind a diaphragm and that directly applies the force to the liquid in the chamber forcing it up and out of the pump.

That same force pushing one diaphragm out is drawing the other diaphragm in, as they are attached to a common center shaft, and that creates a vacuum in the opposite liquid chamber.

While one side is evacuating liquid, the other side is filling up and this process goes back and forth to create the actual liquid transfer.

AODD pumps are used in a wide array of industries. AODD are explosive proof, no fluid leakage, self priming, adjustable discharge volume, simple structure, compact and can transfer fluid containing slurry or high viscosity.

The are also simple of design and can be easy to disassemble for maintenance.

These pumps are used in a vast array of industry as described in the following link:

https://www.yamadapump.com/applications/

Strong Export Component

Based on the last 2 quarters, the distribution of sales of industrial pumps and its associated aftermarket sales is shown below:

The USA represents 52% of sales, followed by Japan 23%, Netherland 13% and Thailand 3%. As such, more than 72% of sales is towards the export market for this segment. This trend of continued increase of shares of export sales has accelerated since 2022. Please note that Yamada’s results ends on end of March of each year. So the numbers for 2023 refers to Sales from April 2022 to March 2023. The largest contributor in sales growth is coming from USA, followed by China and Thailand. Europe is flat. Rising export sales is something beneficial for a Japanese enterprise due to the long term trend of yen depreciation and gives protection from the weak GDP growth and demographic challenge of the Japanese market.

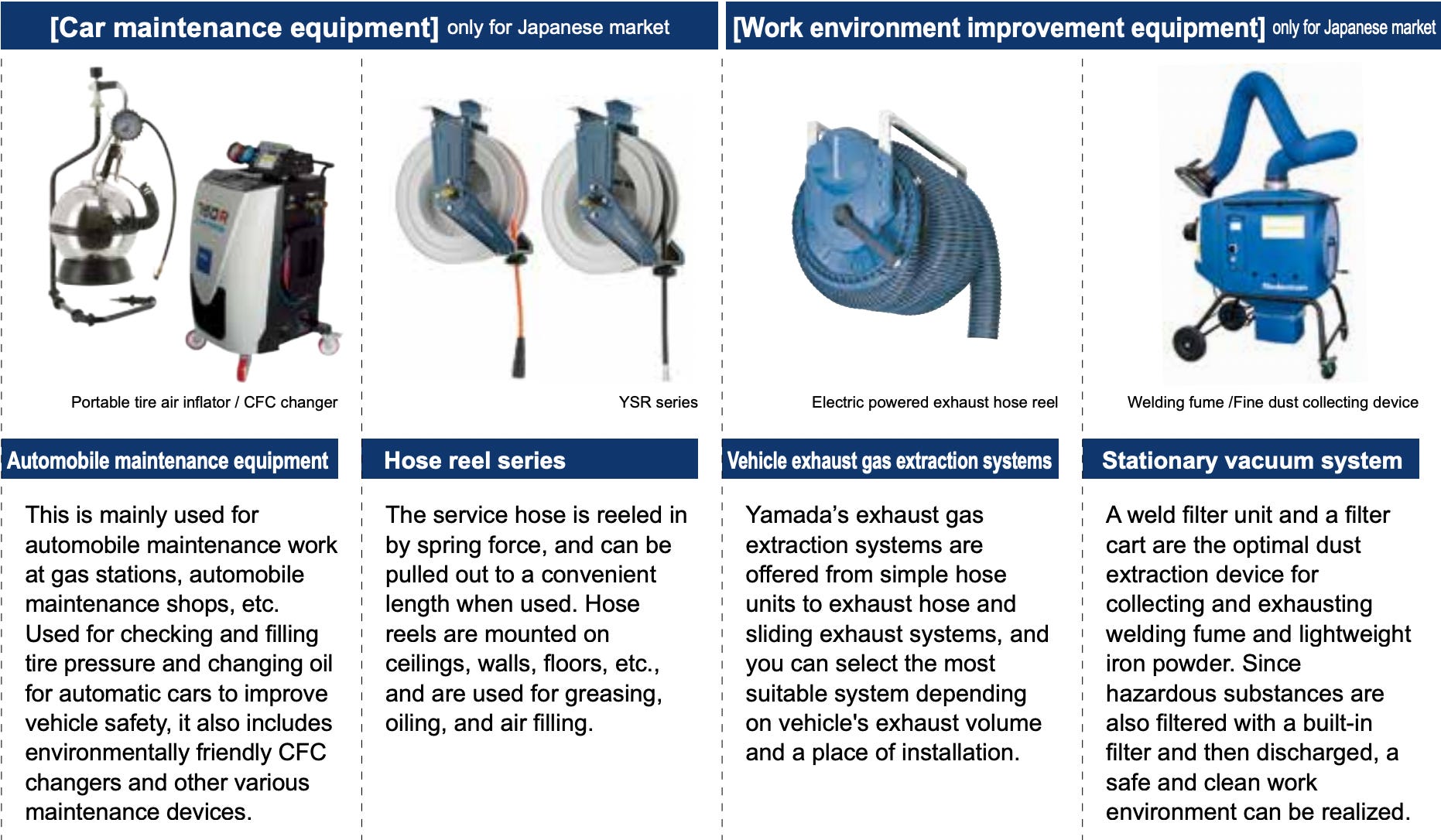

The Automotive segment

The other segment which represents 26% of sales for the last 6 months is related to the automotive market. Most of the products are related to pump related specialized equipment used in automobile repair shops: portable air inflator, electric powered exhaust gas extraction and toxic dust vacuum.

Healthy Margins

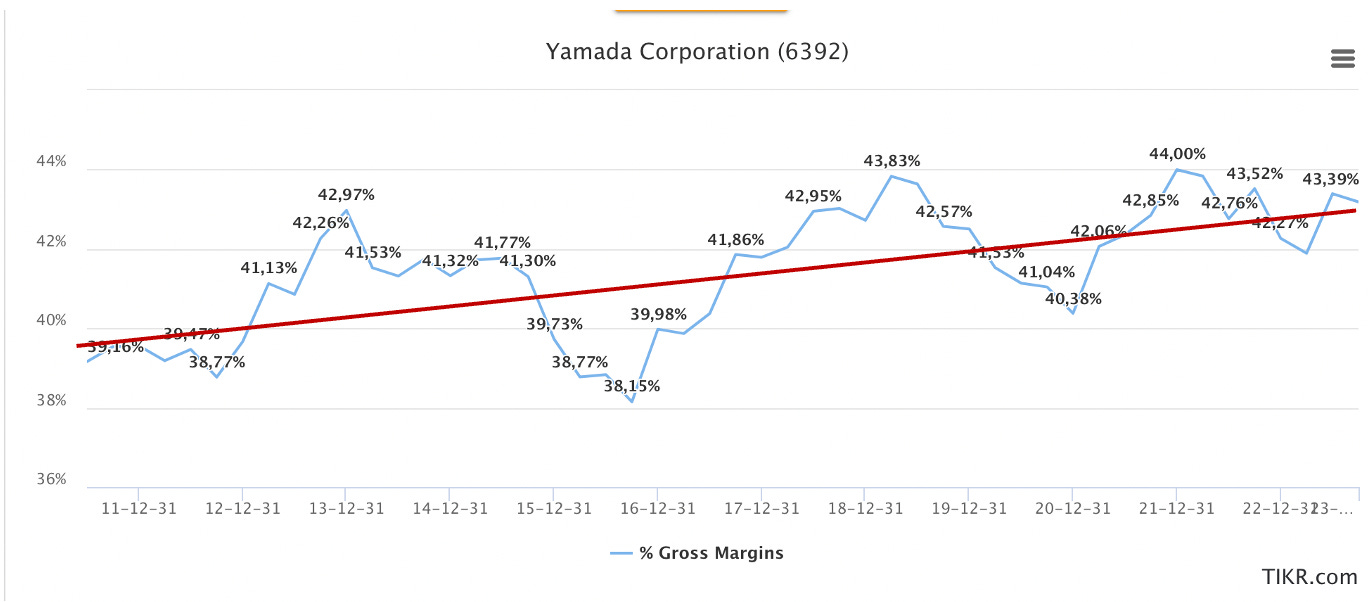

Yamada has exhibit healthy gross margin over the last 11 years hovering between 38% and 44%. Furthermore, I think we can detect an upward trend of the average gross margin from 39% in 2011 to 43% in recent years.

I really like those quarterly 12 months LTM charts from TIKR. You can subcribe to TIKR using this link. https://app.tikr.com/register?ref=8mn9us

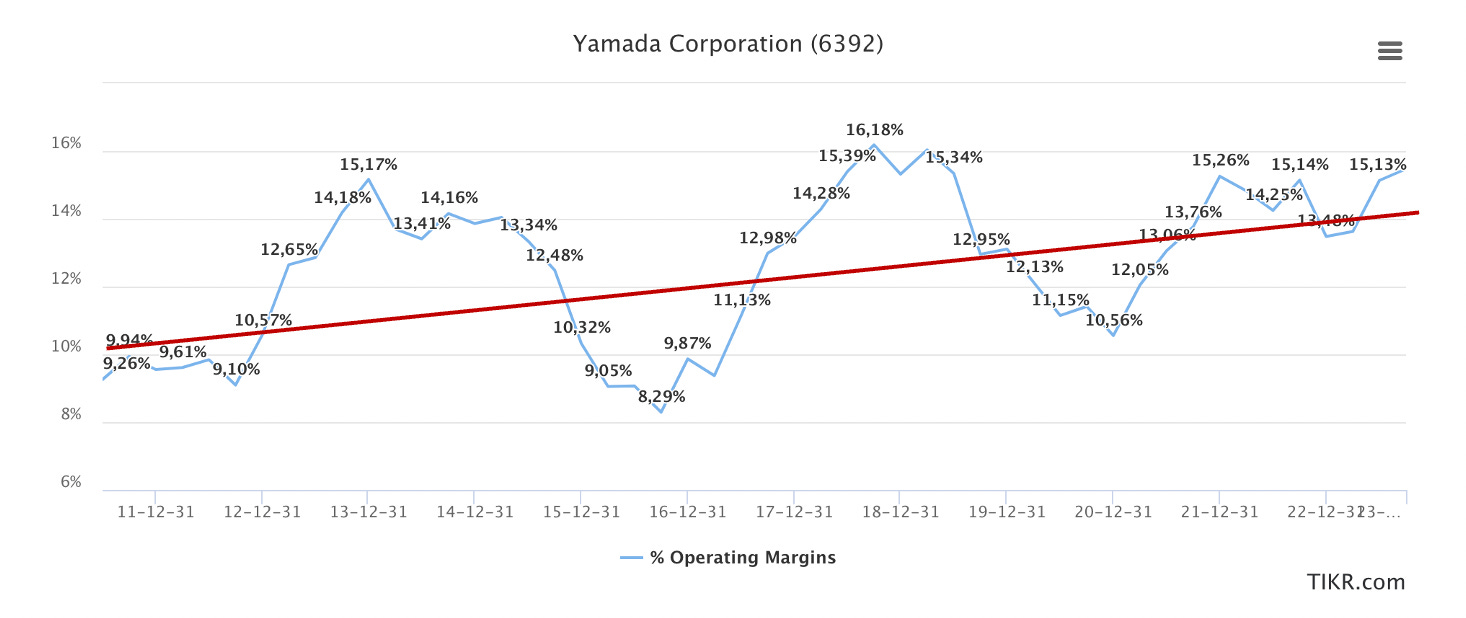

This is reflected in the operating margin whis stable but following an upward trend from 10% in 2011 to around 14%+.

This indicates that the products have good pricing power even in difficult time and Yamada has built a narrow moat.

AODD Market and competitors

The market of AODD pumps is fragmented however my understanding is that Yamada is among the top 5-7 in the markets they are marketing their product (USA, Japan, Europe). Here are a list of top AODD vendors: Graco, Dover, Yamada, Crane, Ingersoll Rand, Flowserve.

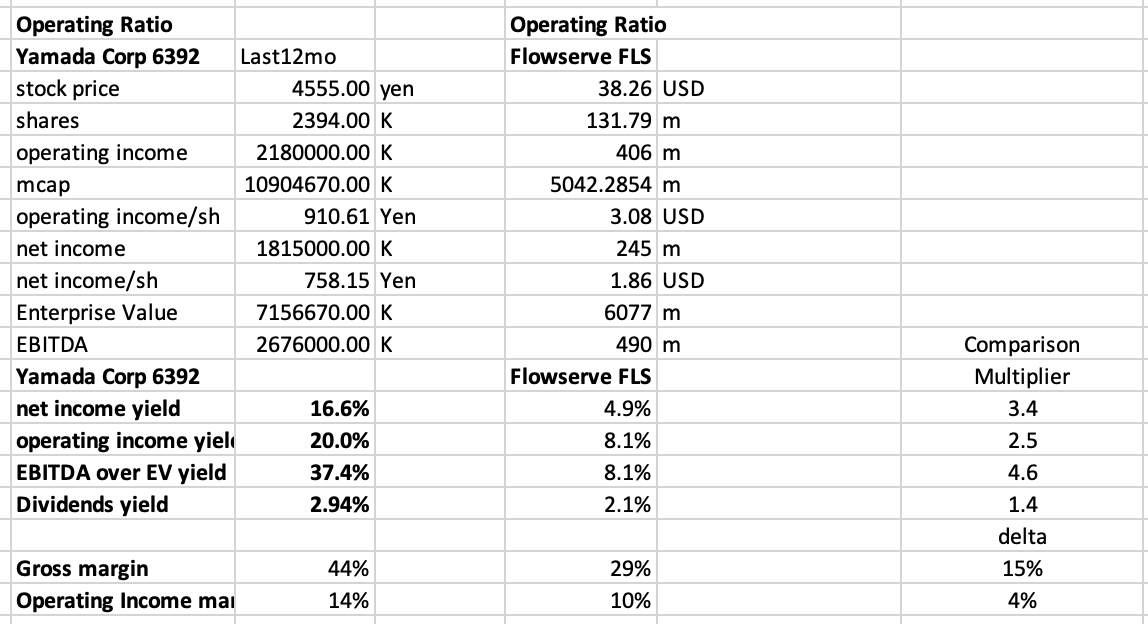

Criteria 3: Attractive operating income yield compared to peers

Yamada exhibits attractive income yields as shown below:

These are amazing operating yield by itself, but lets compare this with a pump manufacturer - a very large pump manufacturer. A Classic David against Goliath comparison.

Flowserve - a giant peer

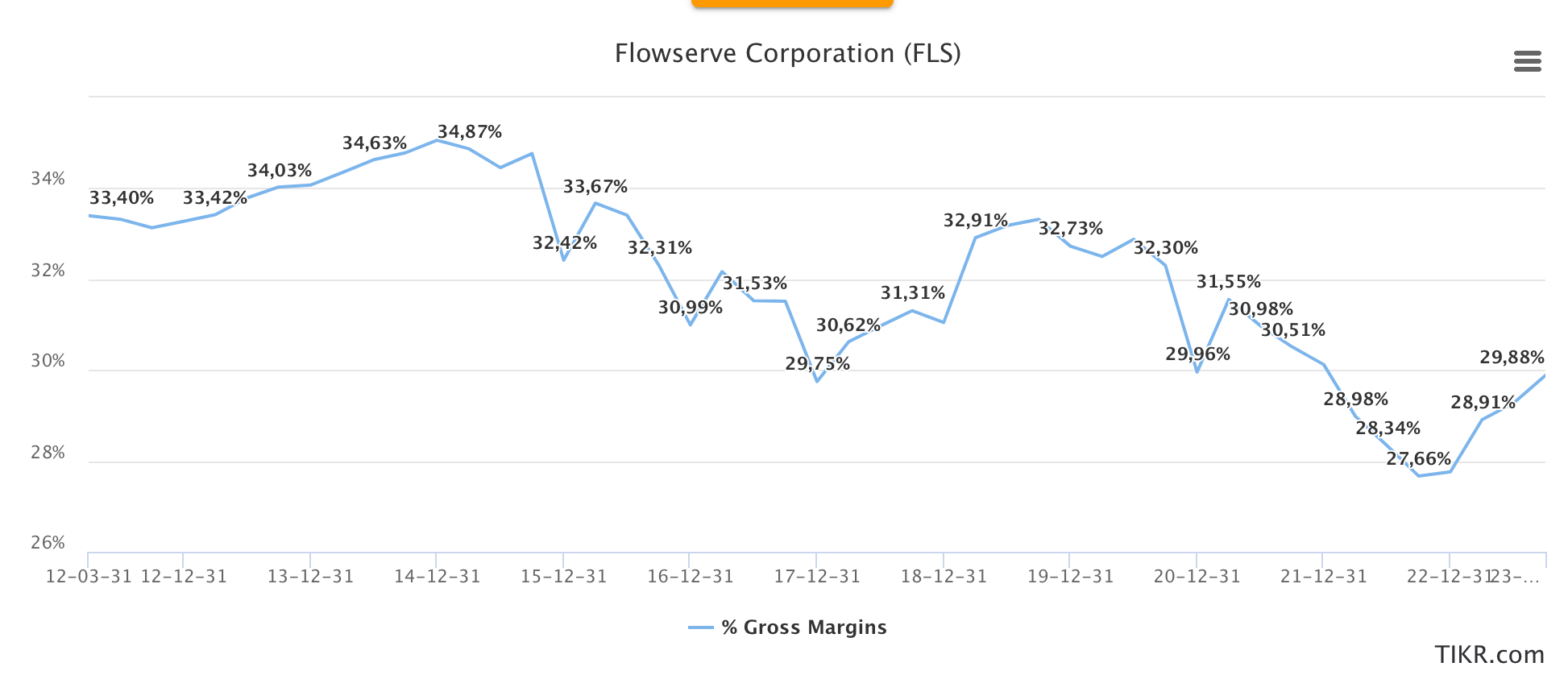

Flowserve makes custom and pre-configured pumps and pump systems, mechanical seals, as well as engineered and industrial valve and automation solutions, including isolation and control valves, actuation and controls. Flowserve’s trailing 12mo sales is over 4.1B USD versus Yamada’s trailing 12mo sales is 129m USD so 31x larger. Flowserve has a much larger product portfolio. Lets look at the historical gross margin and operating income margin of Flowserve to understand if Flowserve have operating scale leverage.

As you see Flowserve gross margin is hovering between 27.6% to 34% and is following a down trend where recent gross margin is around 30%. Yamada’s gross margin is much healthier at 43%.

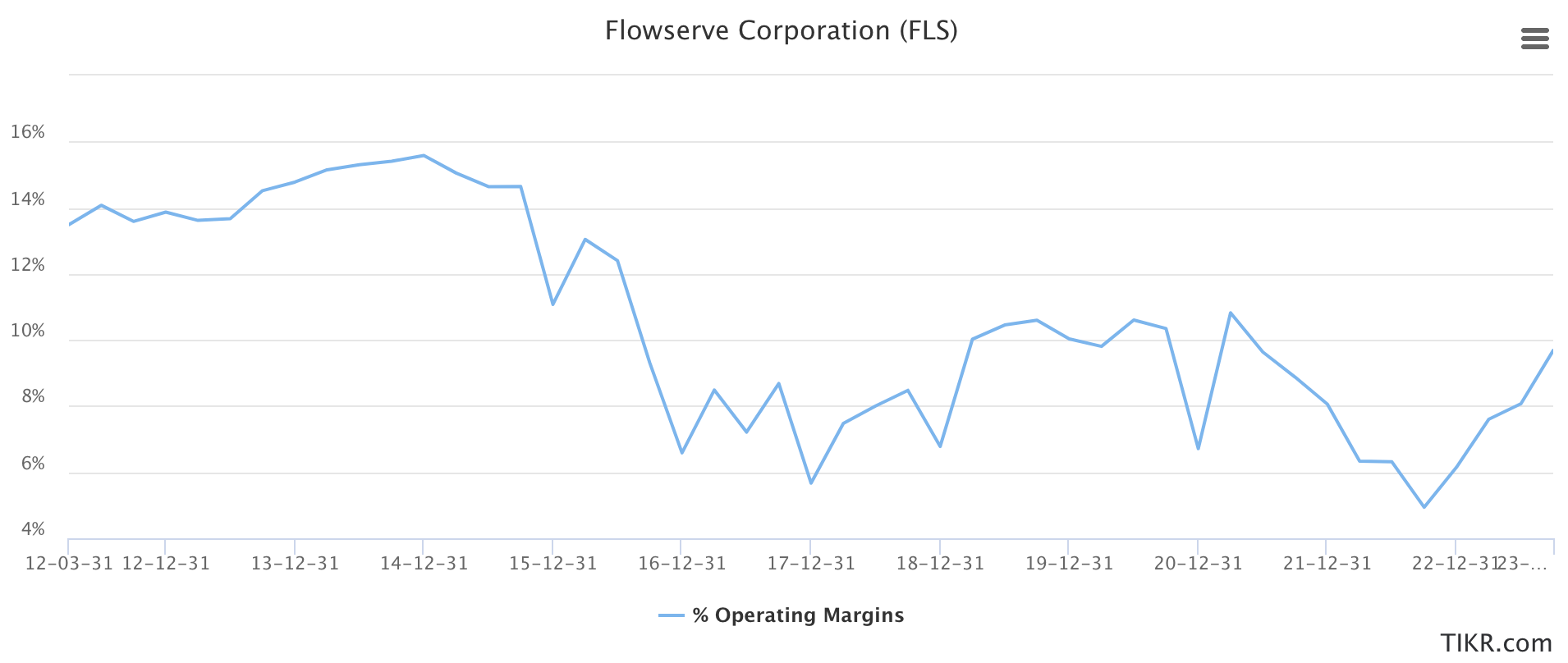

In terms of operating margin, Flowserve is also following a down trend and is now around 10%. Yamada’s operating margin is currently at 15%.

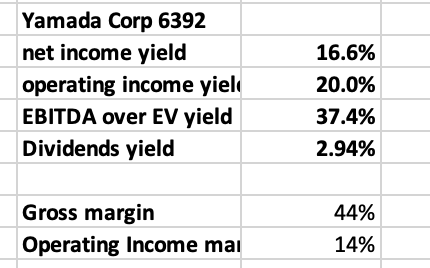

On a net income yield and operating income yield, Yamada is 3.4x and 2.5x more attractive than Flowserve. Because Yamada is very cash rich compared to Flowserve which has about 1B of net debt, the EBITDA yield over EV is 4.6x more attractive.

More surprising, even if Yamada is 31x smaller in terms of sales has a positive delta of 15% and 4% on gross margin and operating margin respectively. Clearly, from these criteria, Yamada is a widely more attractive than Flowserve.

Criteria 4: Long term Revenue and EPS growth

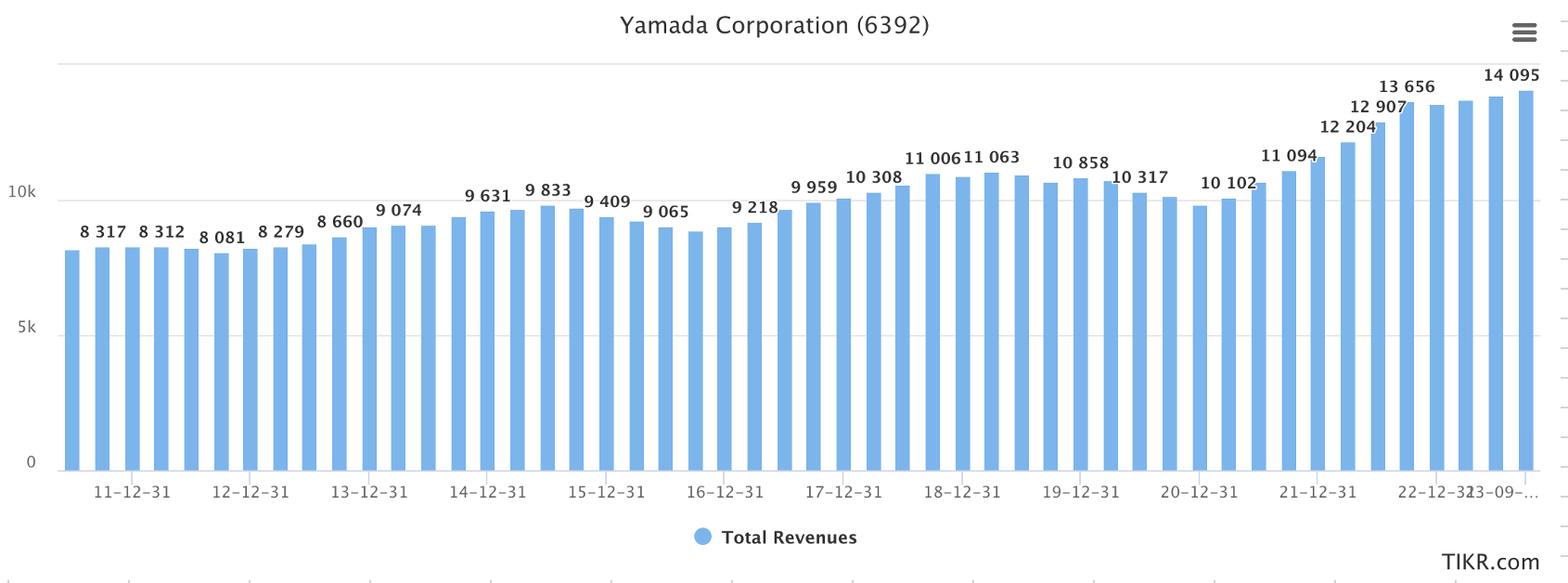

Yamada have seen sales growing very steadily at a CAGR of 4.5% over the last 12 years as shown below with only 2 small down turn for a few quarters (in end of 2015 and 2020). I like the fact that growth is very predictable although slow.

Furthermore, if you focus on USA sales, CAGR is 9% since 2016.

If we look at the historical EPS, the EPS is more cyclical, however since we have seen that both gross margin and operating margin have grown over the last 12 years, EPS has been growing more rapidly than sales at a CAGR of 11%. Now it is possible that over the next few years, Yamada’s margin may drop by a few points, but it seems that it is capable of growing margin over the long term. In 5 years, I would not be surprised to see margins even higher.

This is truly outstanding that a company which exhibits some very good growth in net income over the last 12 years is trading at such a high net income yield (16.2%).

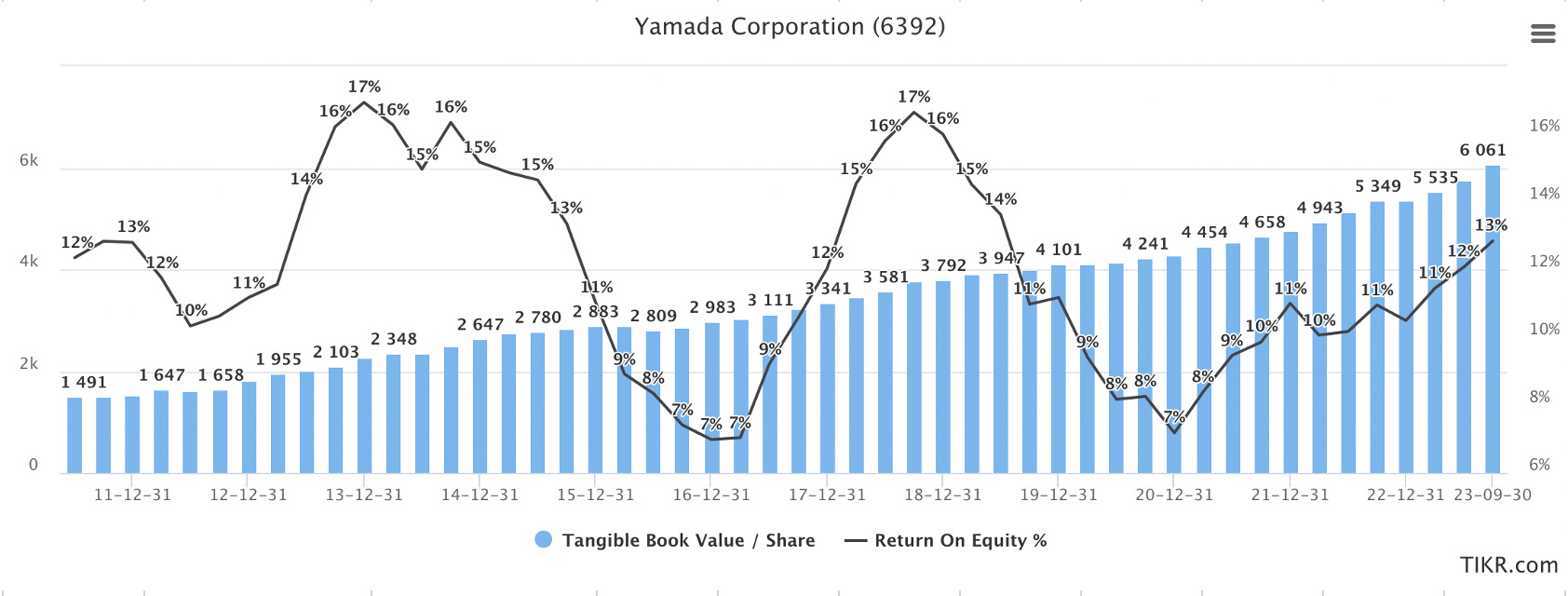

Tangible Book

Tangible book has grown steadily at a CAGR 12.3% over the last 12 years. RoE is also quite acceptable, however, if you remove the cash component of the equity, RoE is much higher.

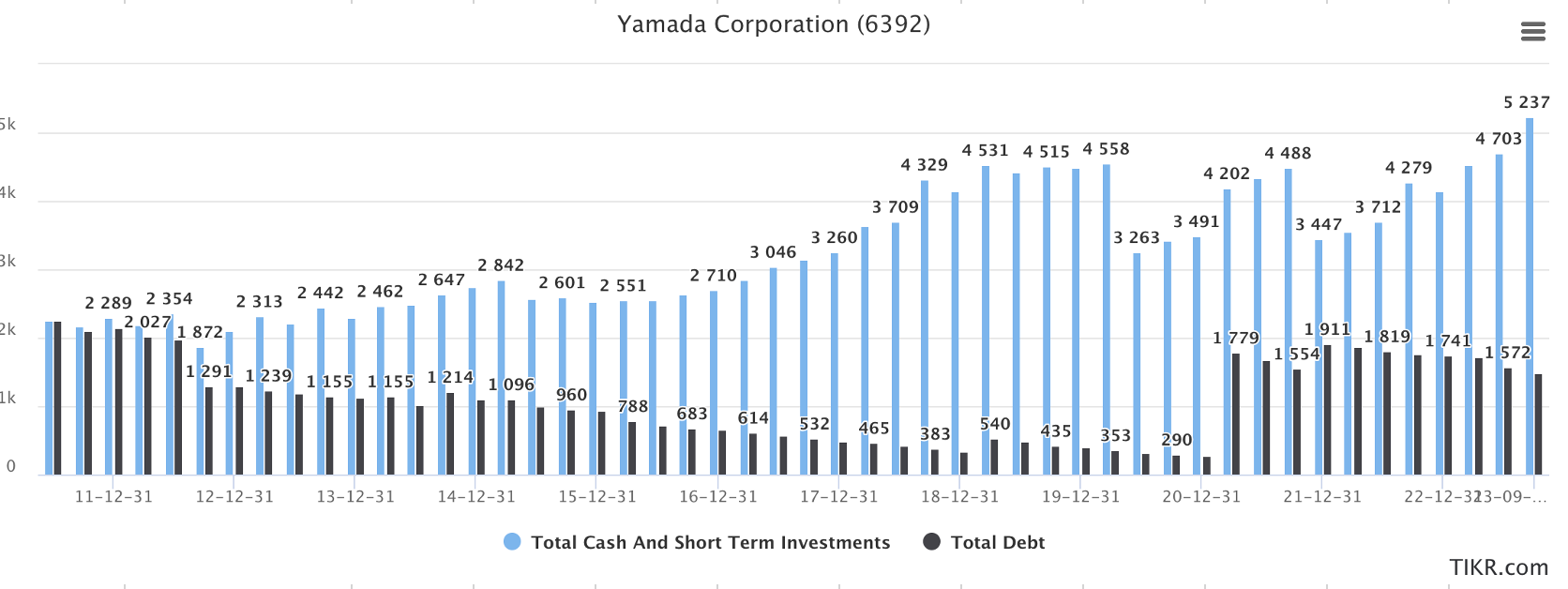

Yamada has repaid its debt steadily from 2011 to 2020 to almost zero while increasing its cash position. Then, in 2021, it took 2B of debt to build the Sagamihara fab. The old fab was build 60 years ago, so we should not expect a new plant soon. My understanding is the new fab is much larger than the old one and allows Yamada to consolidate its manufacturing work in a single location and there is space now to build more products.

Skin in the game

The Yamada family has a whole owns 23% of the company. Two members of the family have key roles in the management. The current CEO Shotaro Yamada owns 8% of the company and Kotaro Yamado the head of technology owns 4.7%. This is very much a family run business.

Conclusion

Yamada Corp I found I can buy a family run and owned solid business with superior gross margin (43%), operating margin (15%), a fortress of balance sheet at 40% cash of market cap which have been growing sales, EPS and tangible by 4.4%, 11% and 12.4% respectively in the last 12 years at a net income yield of 16%.

On the cons, thinly traded… be careful this is japan where undervalued stocks can remain undervalued for years be patient. There are no buyback in the recent history and it is paying 3% of dividends which is very small payout ratio. There is no cross shareholding in this company neither.

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested

Great write-up! But dose the company have English version reports? I only found Japanese version.

Thanks for sharing🙏 Great write-up👍 As I started researching the Japanese market for some hidden gems, it's definitely a very interesting one.

I will add a link to the analysis in RhinoInsight's upcoming Friday Roundup today.