Logistec 2022 earnings update

Logistec released today on March 22nd the 2022 year end results, here are the updated numbers and charts. Updated on March 24th 2023 at 2AM ! after reviewing the 2022 annual report and the conf.call

All figures in this article are in canadian dollars

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. Please refer to the disclaimer at the end of this article for more details.

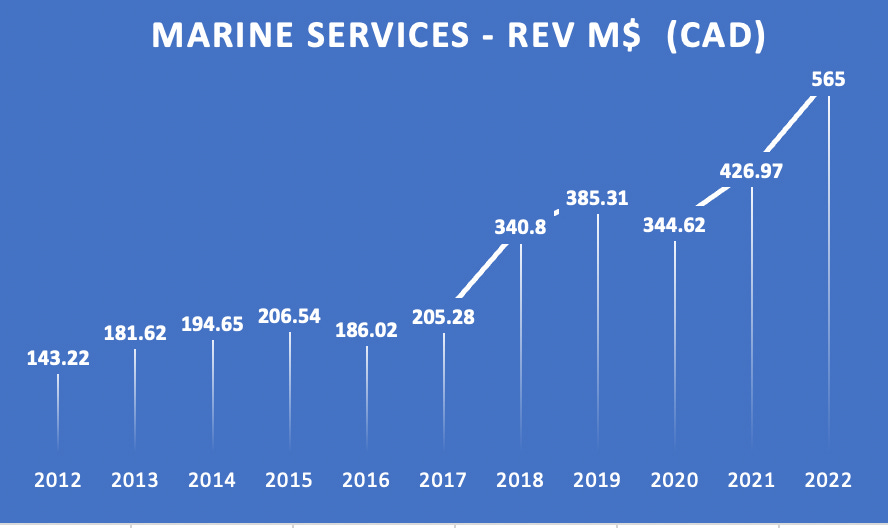

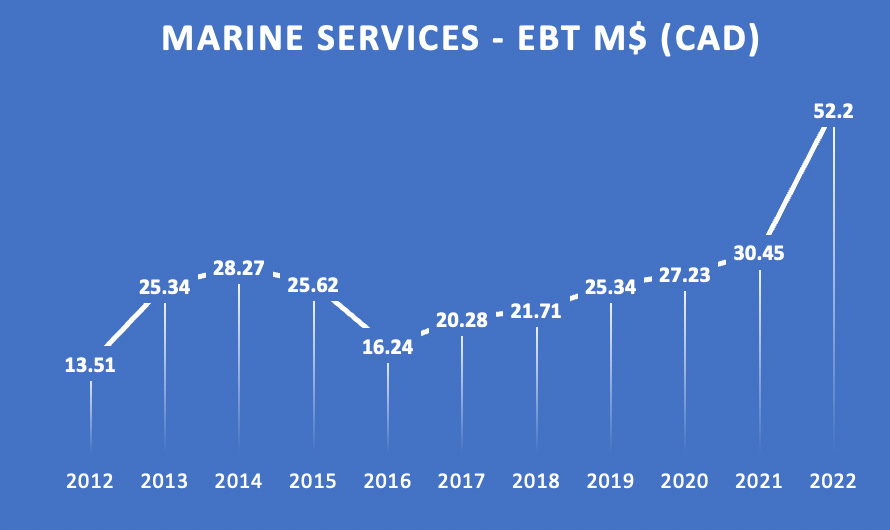

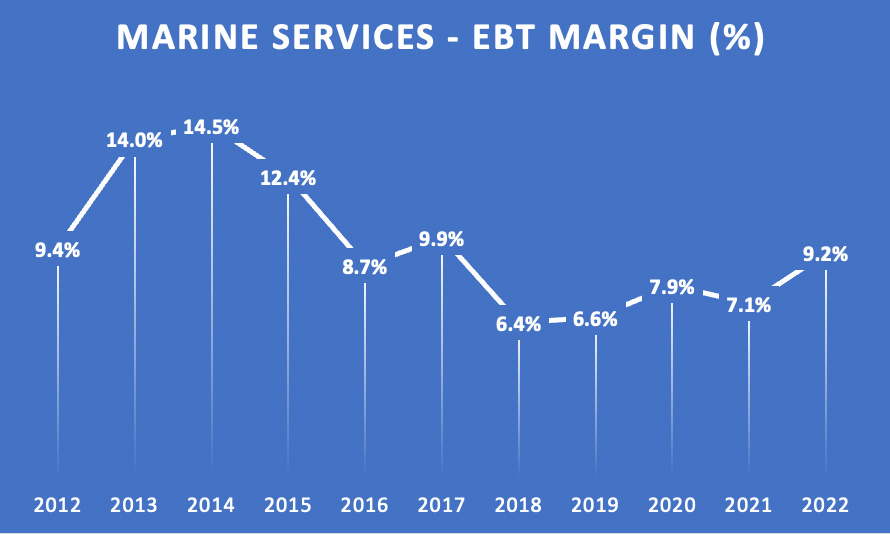

Marine Business

The marine business is firing on all cylinders! with sales reaching $ 565 million, up 32%. EBT has reached $ 52 million - up a staggering 73%!

This reinforces my belief that management must focus new investments into this segment. The management seems to agree for now, with Logistec’s largest acquisition to be made in it history, the acquisition of the Fednav Maritime Terminals to expand its maritime network by 11 terminals. This acquisition worth US$105 million will bring its network to 90 terminals in 60 ports across North America. This should close by end of this month.

https://www.logistec.com/logistec-announces-strategic-acquisition-of-fednavs-terminal-division-expanding-its-network-in-north-america/

So again we should assume a very large increase of sales and EBITDA in 2023 for this segment.

The EBT margin has improved significantly by 210 BP from last year to 9.2%.

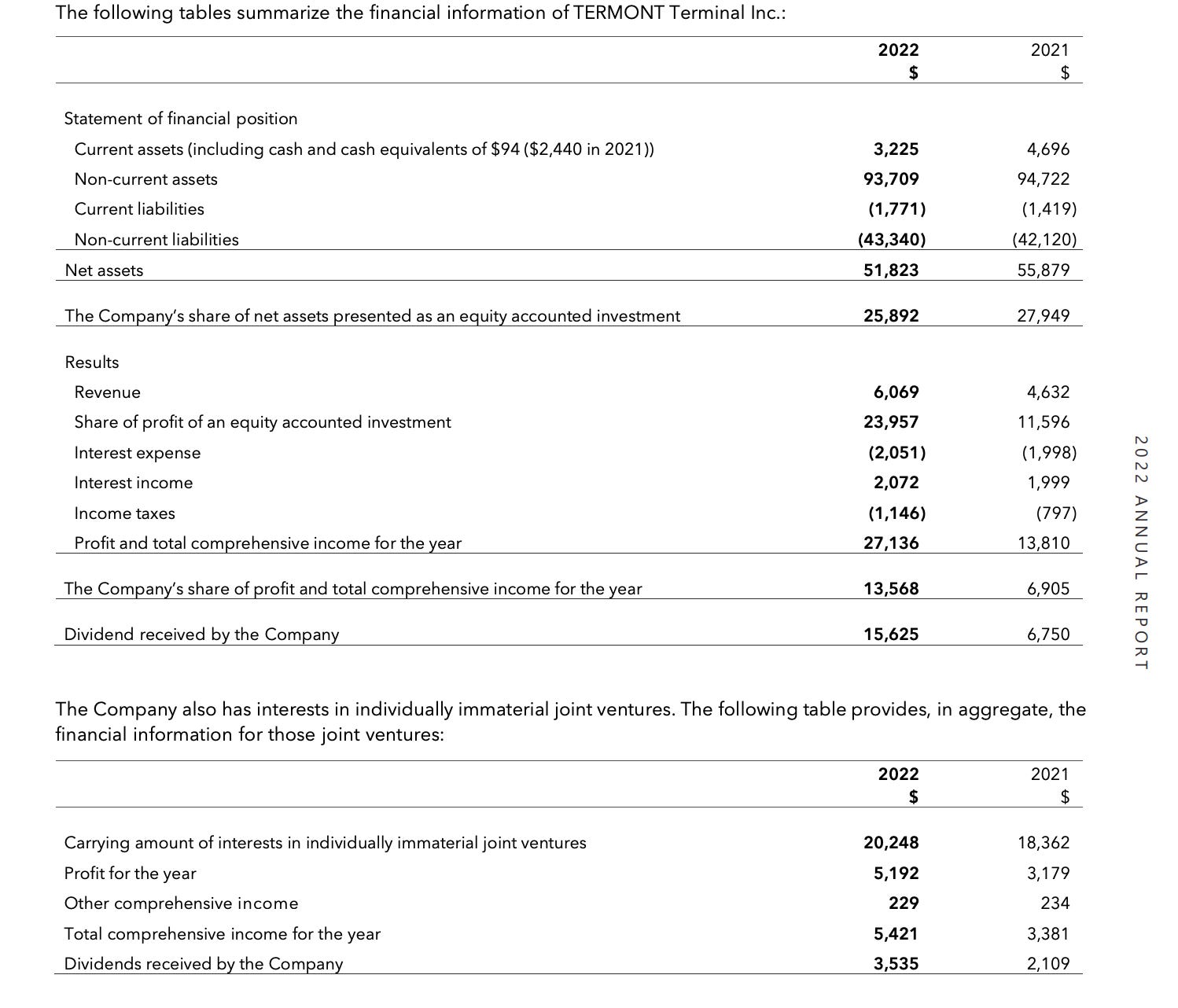

The Hidden Gem port in Montreal

Montreal is a strategic location to ship containers from or to the East (Europe, UK). Logistec manages two of the largest container terminals in Montreal, namely the Maisonneuve terminal and the more recent Viau terminal (both are operating under Termont Montreal). Termont Montreal is owned 50/50 by MSC and Termont Terminal. Logistec owns 50% of Termont Terminal.

Below is an extract of the Termont Terminal results. As you can see, 2022 was a very good year for Termont Terminal, which brought $15 million in dividends and $13.5 million in equity earnings to Logistec, up significantly from $6.7 million and $6.9 million respectively in 2021.

Company share of profit from Termont Terminal is increasing steadily (in thousands dollars)

2019 4102

2020 7351

2021 6905

2022 13568

Also, noteworthy at the conference call, Madeleine Paquin mentioned that revenue generated by Termont Montreal and Nanuk transportation (equity share of 25% and 50% respectively) would have represented sales of $350 million in 2022.

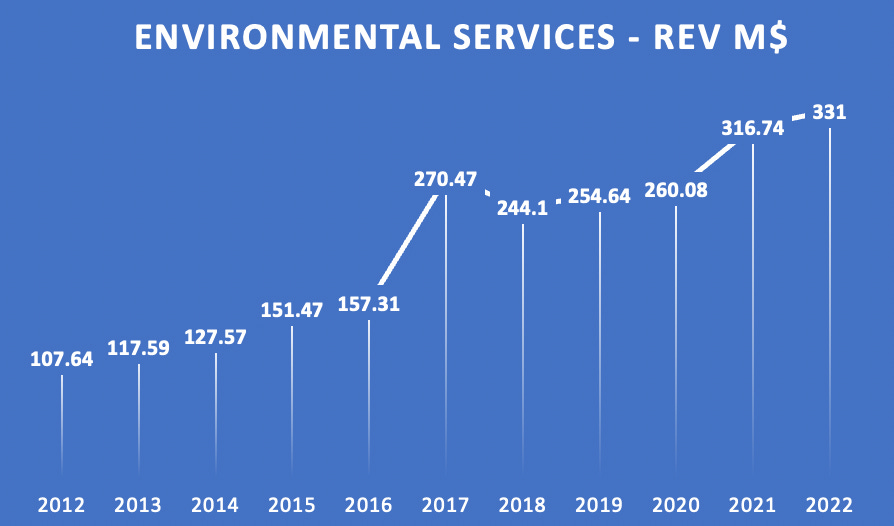

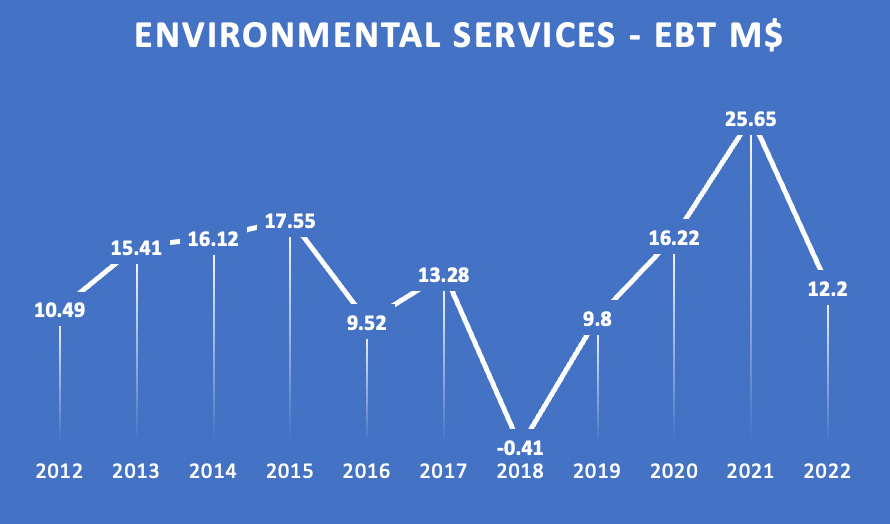

Environmental segment

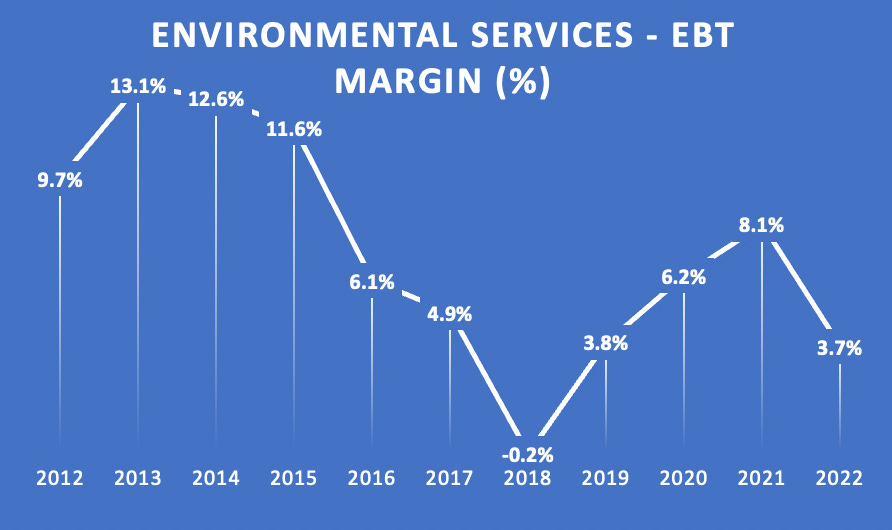

2022 brought disappointing results from the environmental segment. Revenue increased by 4.7% to $331 million and EBT was down to $12.2 million. The increase of sales is mostly due to last year acquisition of American Process Group. The subsegment of the renewal of underground water mains was actually down $ 7 million to $177 million. Management reported that significant contracts related to the ALTRA solutions were postponed to 2023. The performance of this segment has been weak since the acquisition of FER-PAL in 2017, with the exception of 2021 which was a good year.

2022 was the second worst year in terms of EBT margin for this segment, with a EBT margin of only 3.7%.

Logistec has been struggling with the FER-PAL acquisition and the Altra solution business for 5 years now. I believe it is time for management to really reflect whether it should continue to be in the business of Renewal of underground water mains. Ambition to expand in the US has been costly. Perhaps scaling down operations to the canadian market only would be wiser. The site remediation and the dredging and dewatering business seems in much better shape and provides more stable income.

The 2022 annual report still mention that strategic acquisition in the environmental business is a possibility. With the largest acquisition in Logistec history being consumed this month (Fednav Maritime Terminal), it would be ill advised to consider another acquisition especially in the environmental segment.

On the positive side, the marine segment represented 80% of the overall EBT of the company and with the acquisition of Fednav Maritime Terminal, the marine business will be even more significant. The environmental business is becoming less and less a factor when evaluating Logistec as a whole.

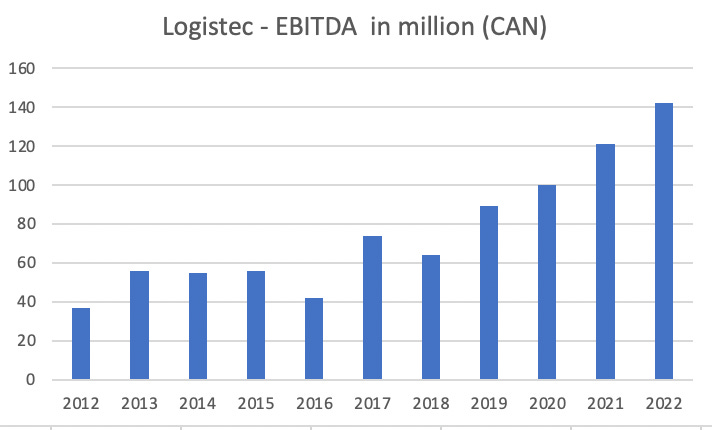

EBITDA

The EBITDA released by the company is $142.1 million which is excellent and meets my expectation.

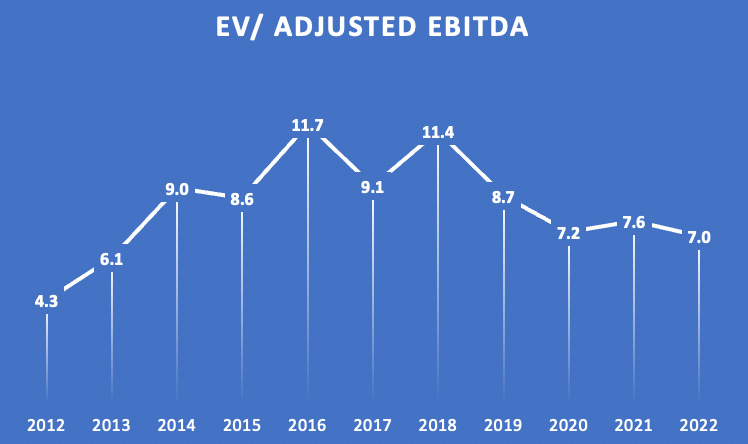

The company EV/EBITDA ratio trade at a low 7.

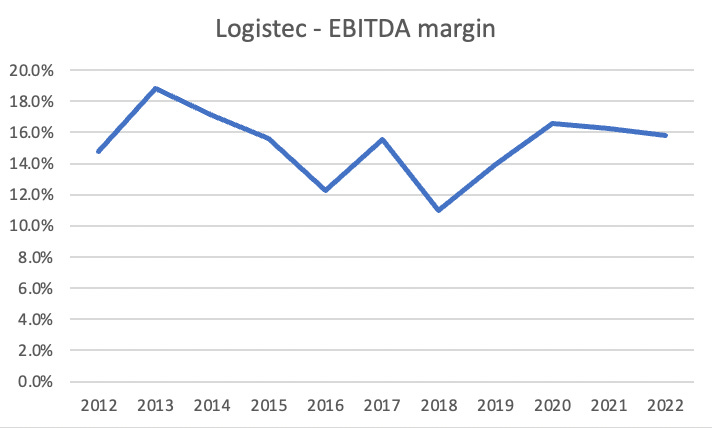

The EBITDA (EBITDA/sales) margin has reached 15.8% which is somewhat below EBITDA margin achieved in 2021 and 2020. Again the slight decrease is due to the weak performance from the environmental segment.

Fednav Maritime Terminals Acquisition

The Fednav acquisition will bring $116.8 million in revenue with a purchase price of US$105 million. The Fednav terminals should be very synergic with Logistec’s network. Fednav headquarter is about 2 blocks (1000 de la Gauchetière) from Logistec’s HW (600 de la Gauchetière) so integration should be smooth.

Here is the list of Fednav maritime terminals. The main market and the predominant cargos handled for each terminal are also provided:

Albany, NY - New York (steel, forest, containers)

Burns harbor, MI - Chicago (steel, bulk, forest, containers)

Eastport, ME - export Eur (forest, bulk, containers)

Hamilton, ON, Toronto (steel, bulk, containers)

Lake Charles, LA, Houston New Orleans, (aluminum,rice,forest)

Milwaukee, WI - Chicago (steel, forest, container)

Port Manatee, FL Tampa Bay (forest, steel, bulk)

Tampa, FL, Tampa Bay (forest, steel, bulk)

Thorold, ON Buffalo, (Bulk, steel, Project cargo)

Port Erie (bulk, steel)

Summary

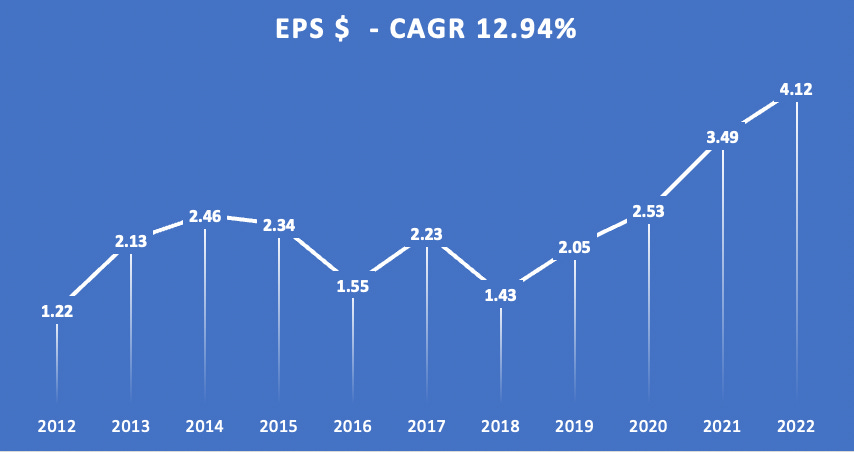

Q4 EPS was below my initial estimates. I thought since Q4 2021 had a lot of non recurring expenses that Logistec would beat last year Q4 results by a mile. It seems that due to very weak margin in the environmental segment in Q4, the excellent Q4 results from the maritime business was not sufficient to raise EPS further. Still 2022 EPS is UP 18% from last year. The maritime business is in great shape, the Termont Terminal subsidiary has brought $15 million in dividends, and with the Fednav acquisition, the maritime business could not be better.

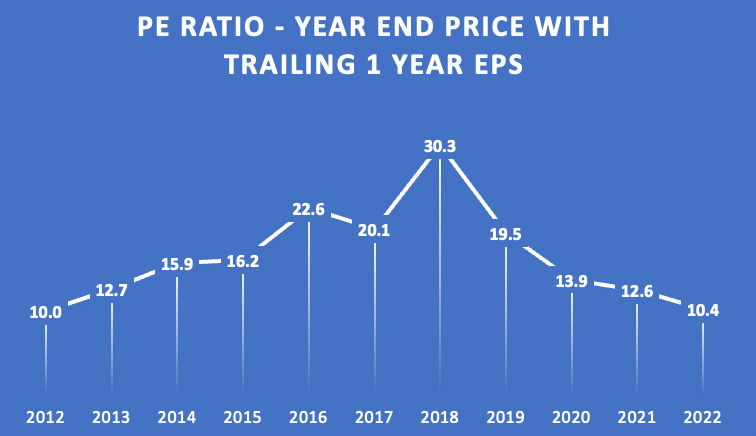

The stock trades at a historically low PE of 10.4.

Feel free to leave some comments

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested

Great write ups, thanks!

Re. FY21 non recurring costs vs FY22 - if I understand correctly from FY22 through FY27 they're required to pay down $10m of principal annually on their 2027 notes, which may have negated a bunch of the non-recurrence of last years costs although I'm sure you probably picked that out? I haven't yet looked closely enough to confirm - I'd presume the the $10m was spread evenly across quarters rather than a lump-sum at year end.

Thanks again for the write ups - very intriguing.