$MCEM Monarch Cement: A superior cement business

This article dissects $MCEM's superior cement business where operating earnings has risen 11x in the last 10 years. Is it pricing, volume, margin? Acquisition driven?

Monarch cement is a $700M market cap pure play cement company which has delisted in 2014 from the public market to reduce overhead cost. It is currently trading on the pink sheet (OTC market) in USA. It is VERY thinly traded. Some day there is no trade (like today May 24th). Be patient if you decide to buy some shares. Monarch cement’ main asset is a single cement plant located at Humboldt, Kansas, approximately 110 miles southwest of Kansas City, Missouri. The Company owns approximately 5,000 acres of land on which the Humboldt plant, offices and all essential raw materials for the cement operations are located. This cement plant has the competitive advantage of having all the essential raw materials to make the cement.

The article constitutes my personal views and is for entertainment purposes only. The main goal of this article is to log my personal views. Nothing in this article or these posts in this blog should constitute an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

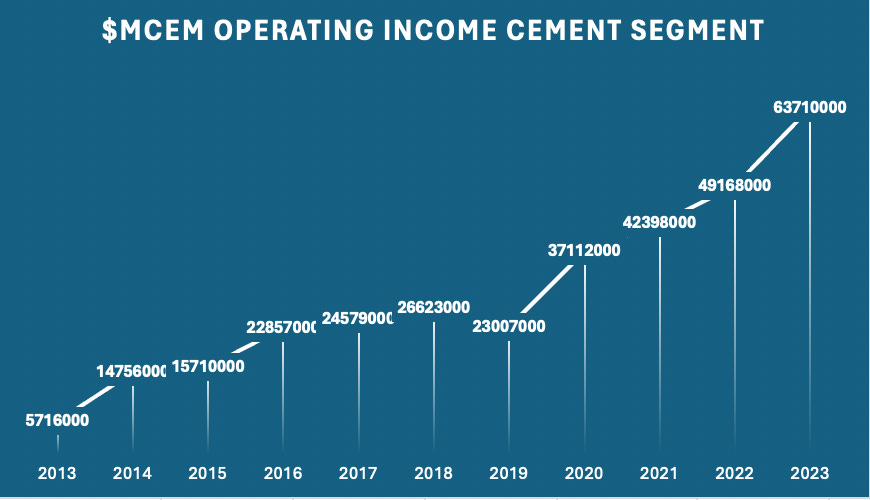

The cement plant has delivered more than 1.3 million tons of cements in 2023. It also owns many subsidiaries selling ready-mixed concrete, concrete products and sundry building materials around the area. The operating income of the Humboldt cement plant has risen 11x from $5.7M to $63.7M in the last 10 years. The rise has been steady has shown in the figure below, with a CAGR of 27%. How can we explain this rise in a boring business? Is this pricing? Volume based? Is it coming from an acquisition? It is a consequence of a rapid margin expansion. I have been dissecting the last 10 annual reports to better understand this outstanding performance.

The operating income numbers in the figure below are in US dollars

Cement business versus Ready-mixed segment

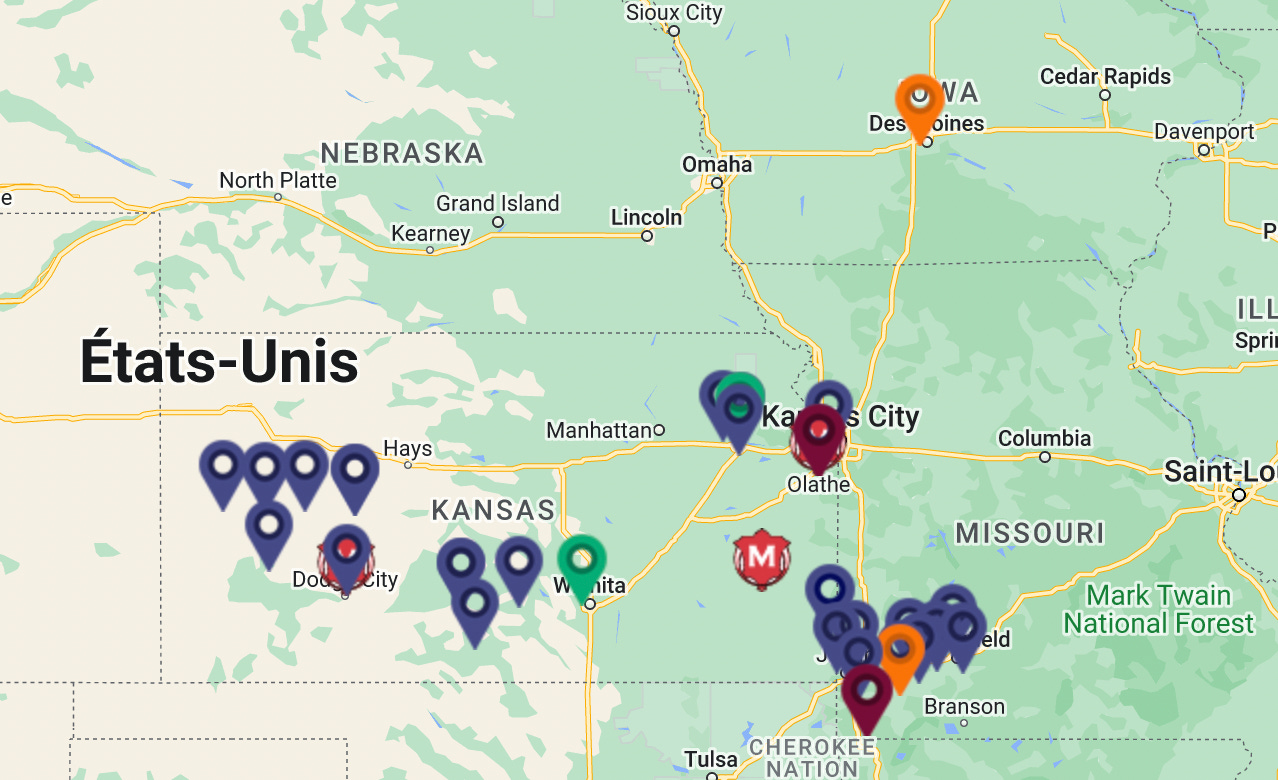

The following maps shows the primary market of the cement related products of Monarch cement. The company’s primary asset is the Humboldt cement plant, located SW of Kansas City, as indicated by the Monarch M logo on the map. This is where the portland cement is manufactured. The other locations corresponds to the ready-mixed locations where ready-mixed concrete is manufactured by combining aggregates with portland cement, water and chemical admixtures in batch plants. Cements are heavy to carry and as such cement plant only competes with local cement plant. A cement plant is typically operating as a local oligopoly with healthy and steady price.

As we can observe, there is a heavy concentration of ready-mixed locations in the Springfield, Missouri area and in Kansas city. Another good concentration of locations are spread to the west of Humboldt in the Kansas state. Please note that the majority of the cement sold is delivered to 3rd party in bulk or in paper bags with the Monarch logo.

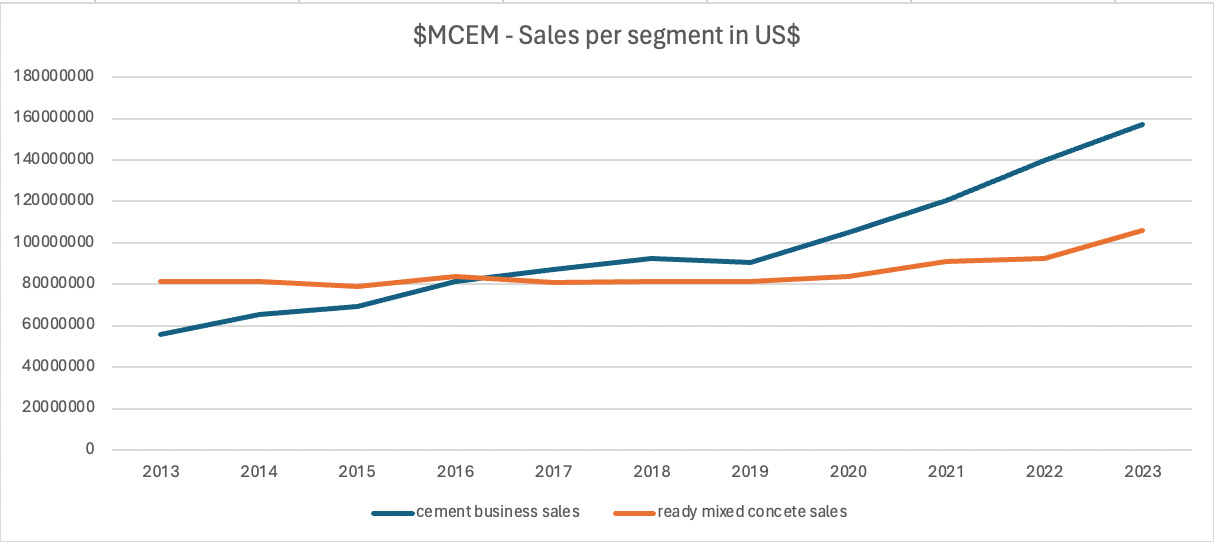

As shown below, the relative importance of the cement business has increased significantly over the years. In 2013, the cement business represent 40% of total sales, while in the most recent calendar year, the cement segment was over 60% of total sales.

In terms of operating income, the cement business represents more than 90% of the total operating income. The ready-mixed business is typically a highly competitive business with low margin as there is low barrier to entry. Anyone can decide to build or purchase a small plant to combine aggregates with portland cement, water and chemical admixtures. A cement plant is another story, which requires very large investment and high environmental barrier, as well as access to the essential raw materials in close proximity (lime (CaO), silica (SiO2), and alumina (Al2O3), in addition to small amounts of magnesia (MgO), ferric oxide (Fe2O3), sulfur trioxide (SO3), and other oxides). Monarch cement's plant is located in a strategic location (Humboldt) which has access to all these raw materials in their 5000 acres property.

Since the cement business represents more than 90% of the operating income of the company, the article will concentrate on analyzing the historical results of this segment.

The Humboldt Earnings Powerhouse

As mentioned before, the Humboldt cement plant is the core asset of the company and have seen operating income growing 11x in the last 10 years in a steady fashion which represents a high growth rate of 27% CAGR.

So where is this high growth coming from? Is it due to steady pricing increase? Steady volume increase? It would be surprising that volumes of such a boring business be raising that fast. Have they done acquisitions or expansion to gain market share? I have been dissecting the growth.

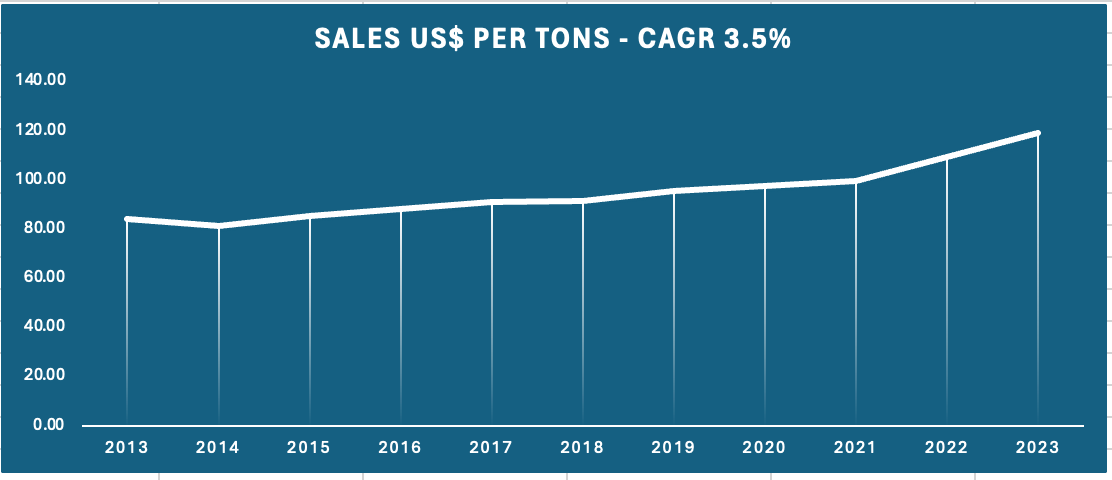

Pricing component - 3.5% CAGR

I have calculated the portland cement sales per tons delivered in the last 10 years. As you see, the price of portland has been rising steadily at 3.5% CAGR with only one down year (in 2014). The price has risen by 41% from 2013: 84$ per tonne in 2013 to 119$ in 2023.

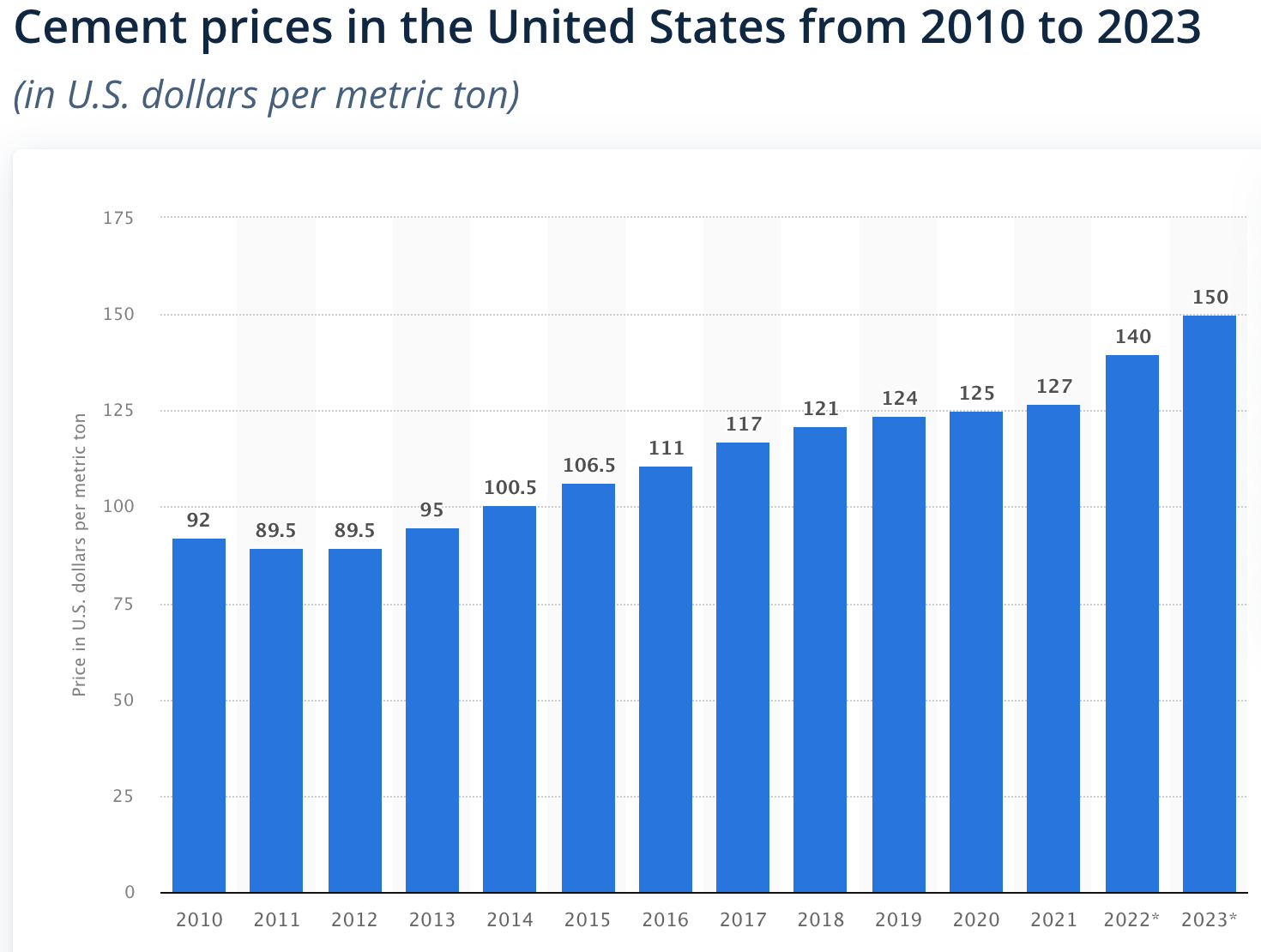

If we look at the national average of the cement portland price per tons, the price went from 95$ in 2013 to 150$ in 2023 per tons or about 58%.

Seems like Monarch cement has not risen its price as fast as for the national average (41% versus 58% for the national average). Cement prices in large cities are likely more expansive due to several factors (environmental constraints, higher transport costs, difficulty to access essential raw materials, higher demand). Monarch cement might sell below the competition’s price to gain market share.

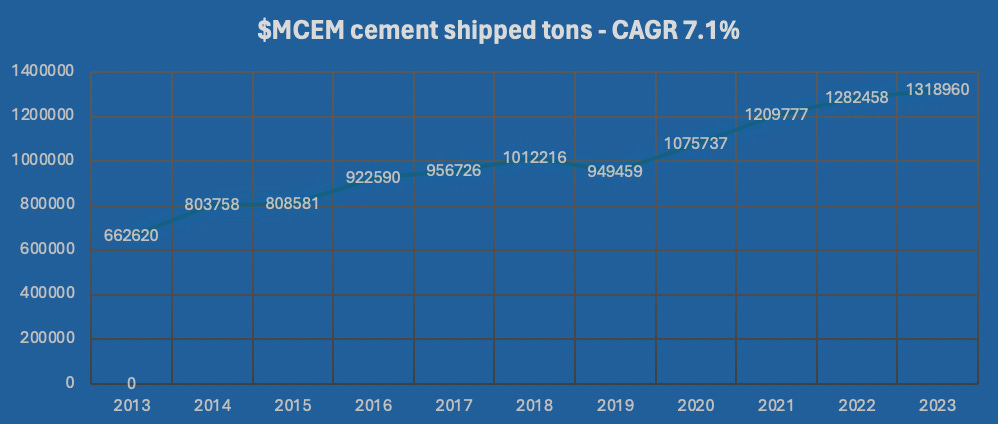

Volume component - CAGR 7.1%

Monarch cement has basically double production in the last 10 years. This is quite an achievement for a stable and boring company. In 2013, they shipped 663 thousand tons and in 2023, they shipped 1.3 million tons.

The rise in volume has been steady growing at an impressive rate of 7.1%. There was only one down year in terms of production: in 2019. 2019 was a very difficult year operationally with heavy rains which have interrupted Monarch cement production during a portion of the year.

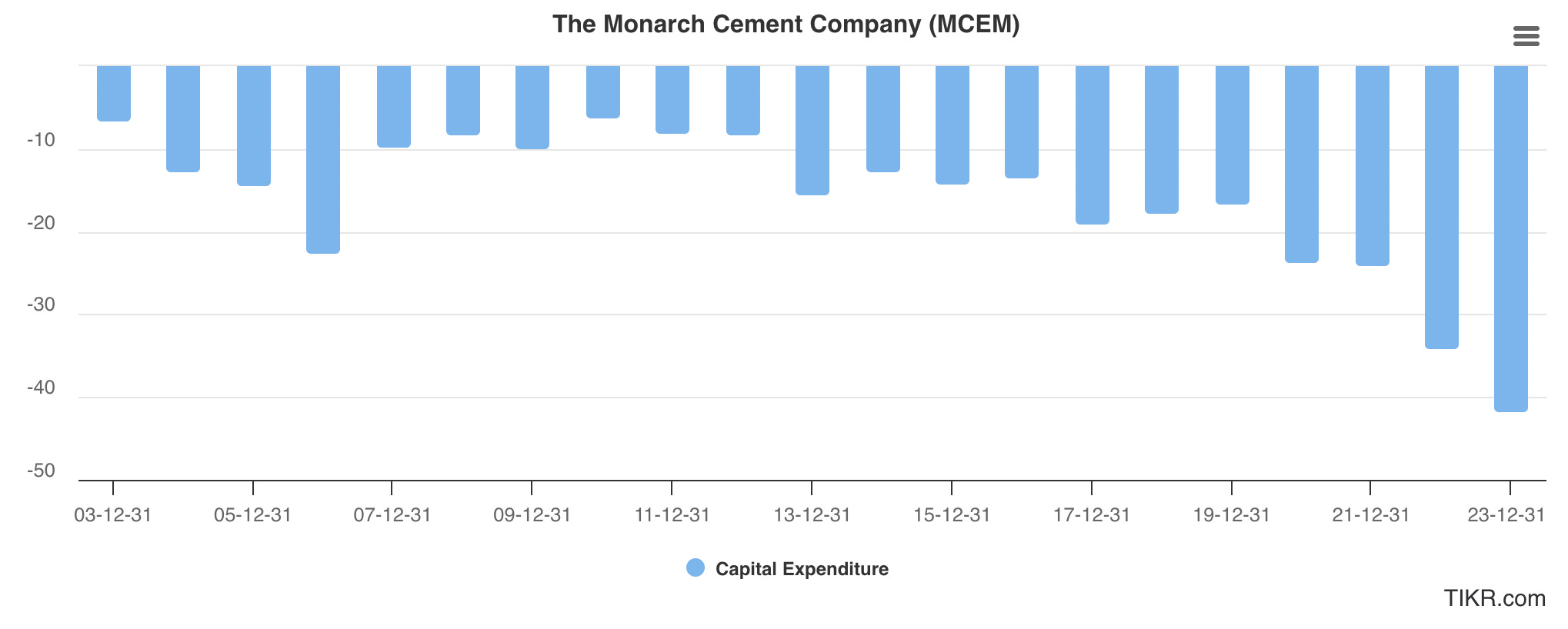

In 2006, Monarch cement has upgraded the cement plant to deliver one million tons of portland cement. So, we could assume that Monarch cement had not reached full capacity until 2018 and 2020. Since 2020, I suspect Monarch cement has been busy upgrading the cement plant to increase capacity.

This is reflected in the CAPEX line as shown below:

You can see that CAPEX investments between 2007 and 2020, after the 1 million tons upgrade in 2006, have been relatively low. Since 2020, the CAPEX program has risen steadily as I suspect the cement plant is operating close to capacity and the management is busy increasing the plant capacity. This is a great problem.

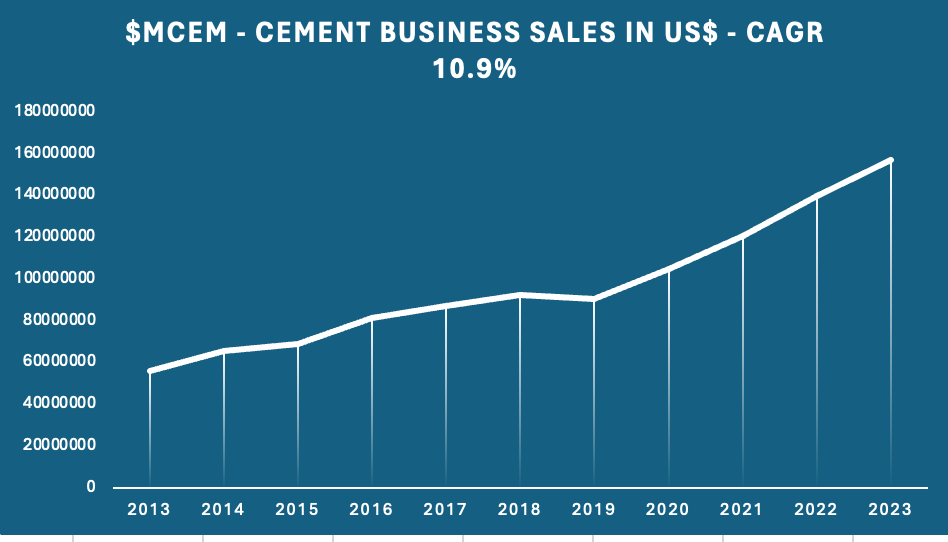

Cement business sales increase

The figure below shows the sales of the cement business which have risen from $55.8M in 2013 to $157.0M in 2023, or about 3x higher. As described previously, this growth is explained 70% from volume and 30% from pricing.

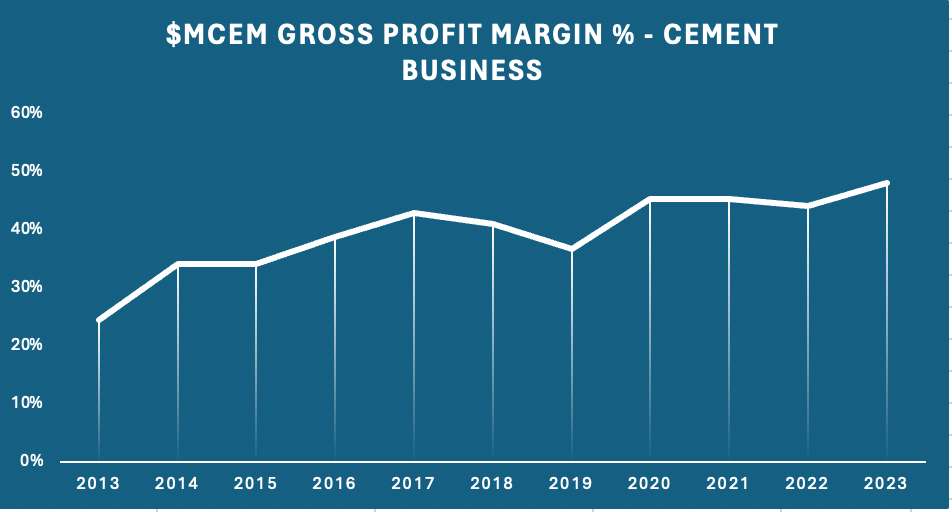

What about margins?

Another large factor is the fact that gross profit margin has doubled in the last 10 years. In 2013, the gross margin was 24% and in 2023, the gross margin has increased to 48%. The rise has been steady until 2017, as the cement plant was getting closer to the 1 million tons capacity. Since 2018, the rise in gross margin have been slower, however, 2023 has seen another big jump. Current gross margin of 48% is very healthy.

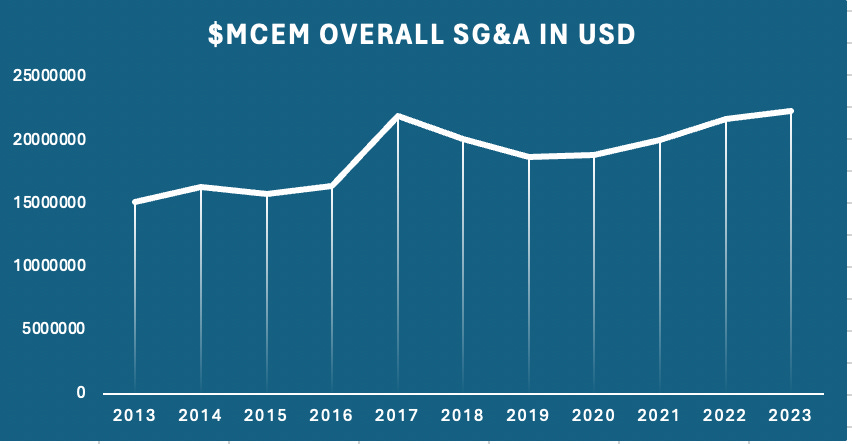

Very good cost containment on SG&A

In contrast, Monarch cement has been very good at containing expenses related to SG&A.

SG&A has risen very slowly over the last 10 years, rising as shown below from $15M in 2013 to $22M in 2017, then going down to $19M in 2020 and going up slowly to $22M in 2023. In 2023, the overall SG&A represented only 8.5% of the total sales. These numbers are not specific to the cement business, but I suspect that the SG&A cost margin specific to the cement business is even lower.

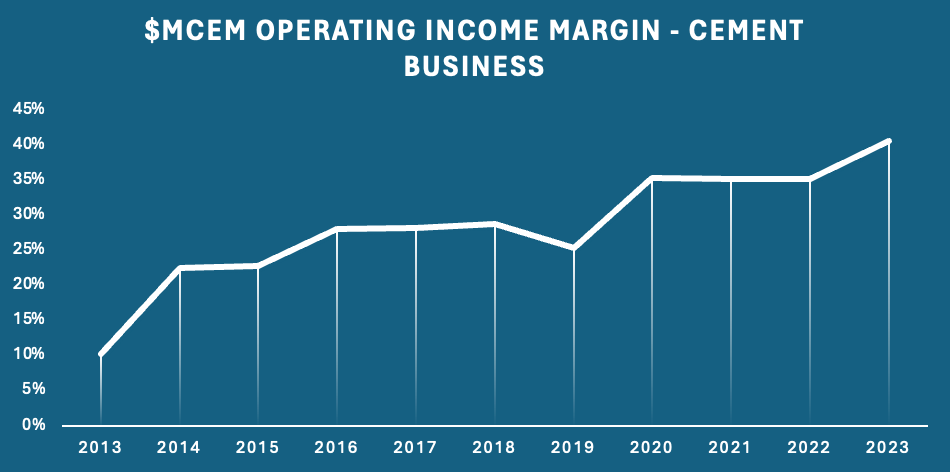

An impressive fourfold increase in operating margin for the cement business

The doubling of the gross margin with strong cost containement of SG&A have lead the operating margin to grow 4 times since 2013. In 2013, the operating margin was around 10% and in 2023, the operating margin is 40%.

Summary and forecast

The 11 times increase in operating income can be explain by 3 factors

4x increase due to operating margin

2x increase due to volume increase

1.5 increase due to pricing increase

This resulted in a staggering 27% CAGR increase of the operating income in the last 10 years.

What to expect for the next 5 to 10 years?

I would think that the average rate of pricing increase should continue, and it might actually increase even faster. We are in a time of strong inflation. So 5% CAGR might be a better projection for the next 5 years.

Volume increase might be lower - so around 5% based on recent trends and the fact that we are in full capacity.

So in terms of sales, I think we could see sales raising at the same rate at before or around 10% CAGR, but the rate of growth would be due to stronger pricing and lower volume rise. This is only based on current trend. Take this with a grain of salt.

In terms of cost, I think operating margin could rise a few % further, but at current 40%, it cannot double again. So I suspect operating margin might increase from 40% to 50% over the next 5 years to reach a plateau.

5 year Forecast summary:

Pricing: 5% CAGR

Volume: 5% CAGR

Operating income margin: 2% CAGR

As such, operating margin might rise around 12% per year in this scenario.

The company is returning around 3% in dividends and buyback. So from a growth perspective, MCEM should compound close to 15% to the shareholder (12% operating income growth and 3% dividends). This assumes no re-rating on valuation. On top of that, operating income should increase even further the balance sheet. The current balance sheet is worth $124M in cash and long term investment.

Follow-up Post

A follow-up to this post, I will go over current valuation, the balance sheet and comparison with peers (North American peers like Martin Marietta, Vulcan Materials and Eagle materials). Quarries in general have intrinsic local competitive advantage and so we will go over that investment concept as well. I will also go over the recent CAPEX increase and provide some visibility on what constitutes those investment.

As a teaser, Monarch cement currently trades at 8.3 EV/EBIT - price as of May 24th 2024 is $193 per share. $MCEM has no debt and a healthy cash balance and long term investment of $123m.

Risks factor:

Cement manufacturer can be cyclical. If local, state or federal government decide to lower expenses related to infrastructure like roads, bridges and so on, the demand for cement will go down. Pricing could go down and operating margin will suffer. A hard landing in USA economy could have a similar effect.

Disclosure: I have cumulated shares of Monarch cement since January when my #1 position Logistec was taken over. I have mentioned several times that name in previous posts or twitter but was not able to make the time to write an actual post on this stock. I was able to slowly cumulate shares at a lower price than the current price. This is not a recommendation to buy or sell the stocks. Do your own research. I am providing this article to illustrate why I think that Monarch Cement could be a good investment and I might get good feedback or learn aspects or considerations that I was not aware along the way.

My investment philosophy is centered around investing most of my $ in targeted industries with strong tailwinds, in industry providing good returns on capital and exhibiting business moats. The top industries I am currently focused on are: E-commerce, Consumer Tech, Fintech, Beverage and Infrastructure. Monarch is a major holding and constitute my largest infrastructure play.

Let me know if they are specific aspects that I have not covered or not planning to cover in part 2 and that might interest you so I could address those in the follow-up post.

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested.

Many thanks for sharing your analysis, great to see how the growth can be explained by a combination of price, volume, and margin improvement! I became quite interested in the company, but two concerns hold me back from investing.

1) How do you judge the risk contained in the equity investments, only in Q1 2024 the posted USD 10.9mio profit? But that profit can also turn into a loss and increase the cylcal risk in a downturn.

2) Any idea where the large local demand over the last 10yrs did come from? Was it mainly coming from public projects and is there any chance to estimate the pipeline for the next years? Were there some large projects in the area that might be finished in the next years and could cause lower demand in the future?

Would highly apricated your thoughts on these two points!

Great-write up. I have been a shareholder for 5 years (I suspect we both learned about this company through OTC adventure blogpost) so I have been the lucky beneficiary of their great operating performance. I made the mistake of cutting my position in half at the beginning of the pandemic... live and learn.