Part 3 - Richelieu Hardware, valuation and outlook

Part 3 - Richelieu Hardware, valuation and outlook

Going over historical valuation and outlook for 2023 and beyond

2023 will be a challenging year in terms of year over year comparison.

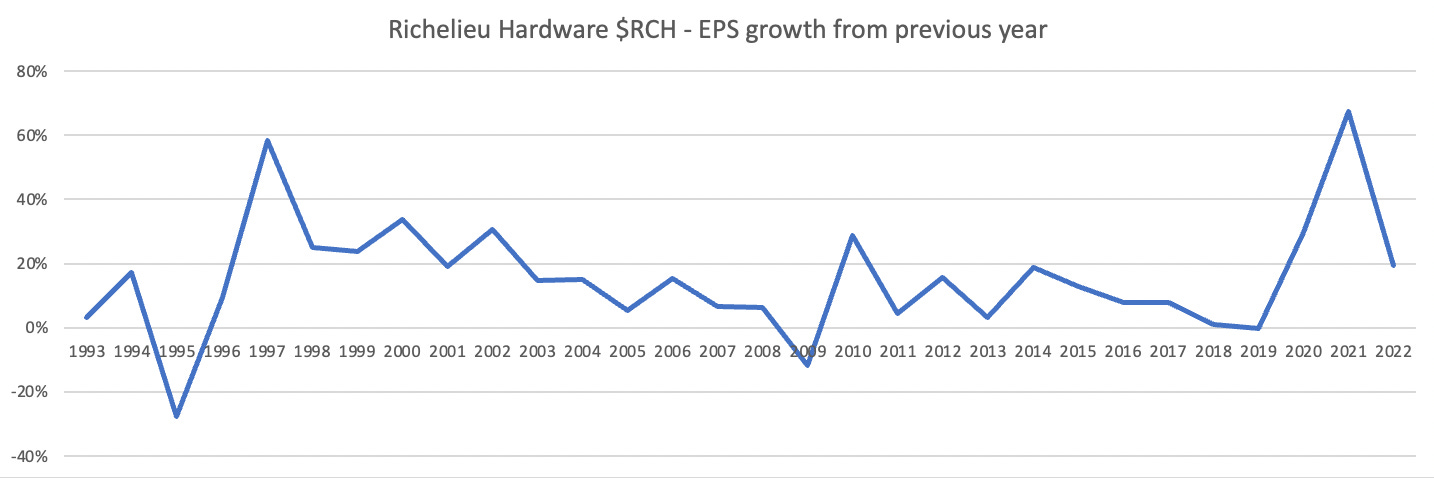

Both 2021 and 2022 were exceptional years in terms of revenue and earnings growth with EPS raising almost 3x in less than 4 years as seen below:

All figures in this article are in Canadian dollars

The article constitutes my personal views and is for entertainment purposes only. This is not investment advice. Please refer to the disclaimer at the end of this article for more details.

WinterGems Stocks -paid users have access to archived posts is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

It is very unlikely that Richelieu will be able to earn more in 2023 than in 2022.

Historical Comparison

As seen in Part 1, Richelieu Hardware produces very steady growth and YoY EPS deceleration has happen only twice in the last 30 years - in 1995 and in 2009.

Both 1995 and 2009 were exceptional year in Canada, with the new construction starts incredibly low and great economic uncertainty. The federal government was facing a very high deficit and it was cutting expenses left and right. The chart below shows the new housing starts in Canada, reaching in 1995 an almost historical low which had not occurred since 1960.

New housing Starts in Canada

2023 Outlook

Will 2023 be such as year? What should we expect in 2023?

Is Richelieu Hardware current stock price correctly reflecting the challenging short term outlook?

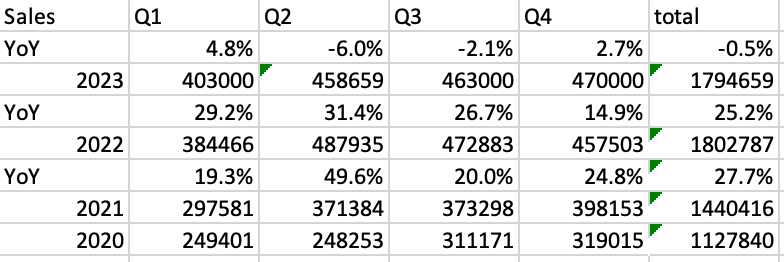

The first quarter was released last week with the following highlights:

Sales of $403.0M, up 4.8%

EBITDA of $49.1M - EBITDA margin of 12.2% from 14%

Eps 40cents - down 25% yoy

Here are some interesting facts gathered during the conference call:

Management is guiding EBITDA margins as a going forward to be in the low 14%.

March saw sales decline in the high single digits. However, March 2022 was the peak of sales in 2022, the best month ever. So we can assume that this is the toughest comparison. Q2 was the strongest quarter and saw the highest growth vs 2021, so it will have the largest decline YoY. We could estimate a 5-6% decline in Q2. Comparison for the the rest of the year will be easier.

Based on management loose guidance, Here are my sales estimates per quarter in 2023:

As such, I would estimate sales to be slightly down (0.5%) to $ 1.794 billion.

For EBITDA, I would use the management guidance of low 14%. Assuming 14,2%, EBITDA for 2023 should be around $ 255 million, down 11% from $ 287 million.

Inventory Issue

In the last 2 quarters, the management has stated that inventory is higher than it should be and inventory will be reduced over the next one or 2 quarters. This can be shown in the following chart:

As you can observe, inventory has increased significantly, in 2021 and especially in 2022, where inventory over sales ratio went from 25% to 36% in 2 years. Management has stated that this was intentional to handle the supplier disruption the industry faced during the COVID period. They claim to have gained market share by doing this. Now that the logistic supply are under control, the management intends to reduce inventory by $ 80 million over the next quarter or so as indicated at the last conference call:

On inventory: It's the same answer as the one in January, Zach. So increase in December and January stabilized in February, and it started to decrease in March, and the plan is to decrease from $60 million to $80 million.

High level of inventory also created some extraodinary expenses which affected EBITDA margin in the last quarter as outside warehousing costs due to temporary inventory increase.

Historical valuation

So considering all this factors including the expected decline in EBITDA in 2023, what should be the fair ratio that we should pay for Richelieu Hardware. As we can see below, Richelieu Hardware typically trades at a ratio of EV/EBITDA of 11.5 (average over the last 10 years).

Today, it trades at a very low ratio of 7.5 of year end 2022 EV/EBITDA. The last time this happen was in 2008 (year end), as the market was forecasting a drop in EBITDA in 2009 and the stock dropped to 5.83$ (split adjusted) and to a 6.5 EV/EBITDA. But this was the GFC and priced were very depressed in 2008 YE.

EBITDA actually dropped by 4% in the following year (2009) and the stock rebound to 7.83$ in 2009 and 10$ in 2010 (almost doubling in 2 years. The EBITDA returned to a more historical average at the time of EV/EBITDA of 10 after 2 years.

So, the price decline is not surprising and it follows the 2008-2010 scenario.

In my opinion, by year end of 2023, Richelieu Hardware should return to more favorable EV/EBITDA valuation - probably not as high as the historical average of 11.5, but something like the one Mr Market assigned in 2010, or around 10.

The table shows below my estimates for Enterprise Value, EBITDA and projected price assigned by Mr. Market by year end. I used the expected low 14% margin indicated by management during the call. Specifically I used a EBITDA margin of 14.2%.

One thing to note is that by reducing inventory by $80 million and slowing down capex investment by Q3, I would think short term debts which stands at $137 million in Q1 should reduce by $80 million (inventory) and with some free cash flow of at least $20 million from operation less potential acquisitions, we should reduce ST debt to $30 million. Q1 is a slow quarter and the company is still investing at an elevated level in capex (warehouse expansion in USA) and made 5 acquisitions.

As such, a fairer price for Richelieu Hardware should be 45$ assuming that EV/EBITDA would return to a conservative 10.

Over the next 3-5 years, organic and acquisition growth should continue and I expect Richelieu will continue growing EBITDA at a historical level of 10%+ and Mr.Market will reassigned a EV/EBITDA of 11.5.

Do your own calculation… but in 3-5 years $RCH should have increased significantly from current level of 37$.

I hope you enjoyed those 3 PARTS as much as I did. I would be more than happy to get any feedback or counter arguments!!

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested

Good job with your part. 3! I readed comments also and I think we focusing too much on the house bubble. The most important factor for RCH is Interest Rate and % of house aged 35 years and more.

- First the age of house is very important to know if people will remodel/renovate their house or not, about this, perspective at US is very good for RCH.

- Interest Rate :: this is the most important factor and we cannot compare with 2001/02 and 2008/09, why? Because they drop the rate during recession, so people can refinance take money from their house and renovate their house.

In addition, renovating a kitchen or a bathroom is very expensive, so many people would have to go into debt to do this renovation and the most common way is to refinance the house at 2-3-4-5%

I know many other factors need to be watched, but for me and in the short term, these factors are very important to understand price/margin/growth. That's why I don't think management will maintain their EBITDA margin at 14% and we should be back to ~11% margins.

I have a lot to say but I will stop here.

Hello! Thanks for your great analysis. I personaly think that there are headwinds in the short term. For example, the consumer sentiment related to the macrotrends economic cycle could have some impact in the bussiness. The housing tendencies also should have some impact. I think the rise in the interest rate will affect housing.

However, the financial position is sound. The low part of the cycle is normally good to serial acquirers when they have an excelent financial position. In fact, they are expading themselves faster than ever taking into consideration the number of distribution center, especially in EEUU.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Cánada 30 31 30 35 34 34 35 36 36 36 36 36 39 41 47 50

EEUU 15 16 18 23 24 24 25 28 28 31 31 34 36 41 57 59

Even with a significat decline in Ebitda in 2023, it would be an atractive investment in the long run if we think the growth will accelerate later. I am considering to start a position. I think the time is with the shareholder in this case. Even if we are wrong about about the price and the decline is worse than expected I think the company will be still here and growing in the following years.