PART2: Richelieu Hardware, Risk Factors

PART2: Richelieu Hardware, Risk Factors

We go over what could go wrong with this serial acquirer

“Success Breed Complacency. Complacency Breeds Failure. Only The Paranoid Survive.” Andy Grove

In memory of the recent passing of Gordon Moore, I thought the famous quote from another Intel’s giant, Andy Grove, was totally adequate. Only the paranoid will survive should be how an investor should assess its holdings - what could go wrong?

Holding a stock like Richelieu Hardware which has raised revenue from $28 million to $1.8 billion in 32 years could lead to complacency from its shareholders.

So what could go wrong?

All figures in this article are in Canadian dollars

The article constitutes my personal views and is for entertainment purposes only. This is not investment advice. Please refer to the disclaimer at the end of this article for more details.

Risk Factors

So what could go wrong with this investment?

Here are a list of potential risks that Richelieu Hardware may encounter in the next few years.

Operating margins may compress over the next few years as new construction homes decline with the raising interests or inventory build-up (post COVID)

New construction home decline could trigger revenue decline

The competitive landscape in US may prohibit Richelieu to take market share

Suppliers may become direct competitors and sell product directly to manufacturers or large box retailer

Valuation risks will be addressed in PART3.

1. Margin, margins, margins

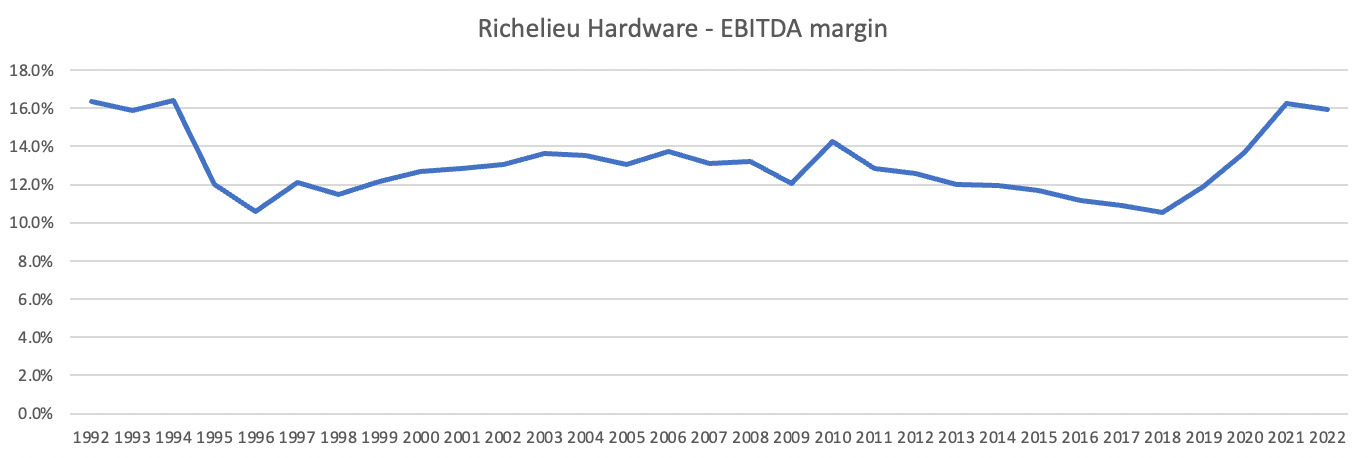

The following figures shows the EBITDA margin achieved by Richelieu Hardware for the last 30 years.

EBITDA margin hovers between 10% to 16% over the 30 years span. The lowest margin was 10.6% in 2018 and 1996. 2018 was a low point in terms of margins, here is what Richard Lord stated in terms of explanation for the margin compression in that year versus 2017:

For the year, EBITDA was $106 million, up by 2.9%. The gross margin was slightly down from 2017, influenced by lower gross margin of some recent acquisition due to the different product mix. Considering the continued investment in market development, the reorganization of some distribution centers, the cost of implementing new technology and the cost of introducing new products, the EBITDA margin stood at 10.6% compared with 10.9% for 2017.

Thankfully, the margin went up dramatically in recent years (2019: 11.9%, 2020: 13.7%, 2021: 16.3%, 2022: 15.9%). Better cost control, namely related to freight cost are mentioned as the main reasons for the increase in EBITDA margin. In 2019, asked whether 12% was achievable long term, Richard Lord mentioned that we are aiming for but it is not a given. Well that was a conservative stance, as one year later, the EBITDA margin went over the 12% level to 13.7%. Now the new long term target EBITDA margin is between 14% and 15%.

Interestingly, margins do not compress significantly in periods of financial crisis, like 2009 (Great Financial Crisis), or 2001 (technology bubble burst). Also, during a very long period, between 1999 to 2013, the margin was quite stable, hovering between 12% and 14%.

Now what should we expect in the short term for 2023?

Here is what Richard Lord had to say about margins for 2023:

There will be a price deflation for certain products for a while. There is no doubt because of the excess inventory, the higher costs that we have, namely for some products for the retailers. That should temporarily affect our gross margin, but especially for example, for the fastener and fitting business because we have excess inventory instead of -- we have direct import for certain of our customers from Asia or directly to our customers. This year, we're going to use our inventory instead of selling product at reduced margin coming directly from Asia. So we have to carry the cost of having this product inventory, but we're going to use the product, which is already into inventory to shift our customers at a lower margin.

That will affect probably our margin. But we don't want to expect any disaster, but we're going to have a certain decrease for certain product line we don't see the effect as being dramatic in Richelieu result if you look at the next couple of quarters.

Zachary Evershed ANALYST

Got you. And previously, you've given a range of maybe 14% to 15% EBITDA margins in a post-pandemic world. Do you think that's still the case with what you're seeing in terms of inventory discounts and that kind of thing for 2023?

Richard Lord EXECUTIVE

Yes, it is.

Since Q4 EBITDA was still quite high with 16.8% EBITDA margin on a seasonally strong quarter, there is still a lot of momentum in terms of margin on the positive side. As such, I would expect based on the comment provided by Richard Lord, that margin may compress by 100BP or 150BP in 2023, to about 14.5% to 15% to reduce inventory buildup of products purchased at higher price.

Long term, management is guiding to a 14% to 15% range. Noteworthy, margins in the US is 2/3 of margins achieved in Canada. This could be explained by higher competition in the US and a less dominant position from Richelieu.

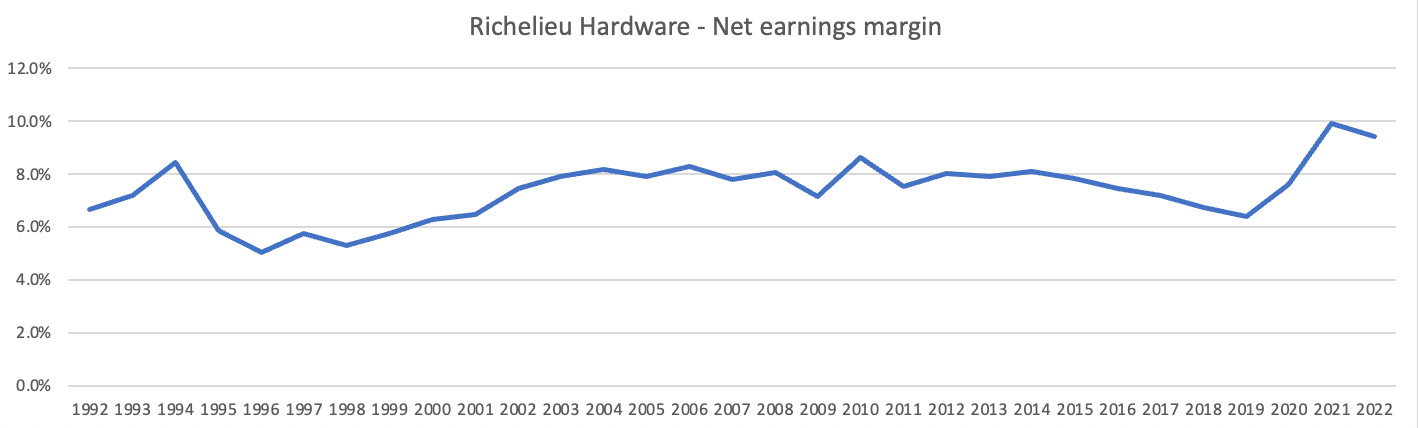

The following chart shows the net earnings margin achieved by Richelieu Hardware.

As expected, the net earnings margin is greatly correlated to the EBITDA margin. So we could probably see a 100BP reduction in net earnings margin in 2023.

2. Impact of new construction start housing units decline

It is expected with the high interest for new mortgage that new construction start will decline over the next few years. So what is the impact of this foreseen decline on Richelieu Hardware’s sales.

The following charts shows new construction start housing units in the US and in Canada for the last 20+ years.

New construction start housing units in Canada

We can observe that the US saw a large year over year decline from 2005 to 2010 and a slow increase from 2011 to 2021. In Canada, the number of new construction starts was quite high until 2008 followed by a sharp decrease in 2009 followed by a rebound in 2010. Although, housing starts never got to the 2005 level until 2021.

If we look at the sales growth year over year for Richelieu, the only year where sales declined was in 2009 and by only 5%. This can be somewhat correlated to the very large decline in new construction started in 2009 for Canada. In that year the decline was more than 50%. It can also be explained that during that year, everyone was afraid of loosing their job, and that it was not probably the best time to start renovating your house. We can safely say that new construction starts are only a small factor that drives sales. Another counterexample is 2022, where new start construction declined in 2022 both in Canada and in the US, but sales actually increased by very high 25%.

Sales growth declined in 2013 and 2019 but the new construction start was stable in those years. As such, I would conclude that new construction starts are not strongly correlated with sales growth for Richelieu Hardware. I believe Richelieu Hardware’s sales are more related to the renovation business of existing homes.

High interest might actually be a good thing, as people will stay longer in their house to retain their mortgage which was financed with a relatively low interest rate. This might actually trigger the need to make some additional renovations to their home.

We stay here but let's renovate our kitchen!

3. The Competitive Landscape

Richelieu Hardware’s sales to manufacturers and woodmakers represents 86% of sales. As such, I will concentrate in identifying Richelieu direct competitors in this segment. Direct competitors in this segment are distributors which sell directly to manufacturers. Here is a list of distributors serving the same market in order of importance:

Wurst Group (private): namely the subsidiaries operating under the name of Wurst Louis & company (West coast), Wurst Wood (east coast) and McFadden (Canada). I have estimated that these 3 subsidiaries operate 44 warehouses. These subsidiaries are operating somewhat autonomously with separate websites. The Wurst Group is a worldwide wholesaler of fasteners, screws and screw accessories, dowels, chemicals, electronic and electromechanical components, furniture and construction fittings, tools, machines, installation material, automotive hardware, inventory management, storage and retrieval systems. The group of over 400 companies across 80+ countries has been servicing the Automotive, Woodworking, Metalworking, Industrial and Construction industries with a strong presence across Europe. The Wurst group has been consolidating the specialty hardware industry in a worldwide basis. I believe other markets like the automotive market or industrial market are more important for Wurst than the specialty hardware market. In terms of the specific specialty hardware (home) market, with 44 centers, Wurst is a smaller player than Richelieu Hardware, but has a stronger presence in the West coast. Wurst’s website is archaic. Ordering online is archaic, where the customer is guided to a PDF catalogue. Wurst has more financial means than Richelieu Hardware and probably has very good pricing power, but it lacks focus on the speciality hardware.

Rugby, division of Adentra: Rugby has 31 centers and have disclosed sales of $ 500 million. It was purchased by Adentra in 2016 for $ 100 million (USD). Rugby Architectural Building Products is a wholesale distributor of specialty building products with primary business is the wholesale distribution of non-structural and decorative architectural grade building products. Their customers produce end products for diverse interior environments including commercial, industrial, retail, residential and institutional markets. Headquartered in Concord, NH, with over $500 million in annual revenues, Rugby’s 700 employees serve over 30,000 customers across the United States. Our geographic footprint covers 41 states, serviced by 31 facilities, a fleet of over 100 trucks, and a sales force of 170 knowledgeable professionals. With $ 500 million in sales, Rugby is about the same size as Richelieu Hardware is in the US. Adentra has been buying distributors in the construction market left and right with debt. Adentra’s operating earnings in Q4 were down significantly from last year and it is much more exposed than Richelieu Hardware to the new construction home segment.

As you can see in the sales split, the majority of sales are related to wood or surface product. Richelieu hardware is not in the stair parts, mouldings, hardwood lumber, hardwood plywood, boards and doors (except the knob and other metallic related product). Adentra is a competitor to watch, but this competitor may not survive the next housing decline downturn due to a high debt level. Adentra is currently priced at a PE of 5.

The following are much smaller player distributors present in NA:

McKillican (private): 17 locations and 40k SKUs. Mostly present in the West coast (Canada and US).

Atlantic Plywood (private): 12 centers in NorthEast of US

Dakota Hardware (private): 11 centers mostly in the South of US

In summary, there are 2 large competitors with overlapping products and similar size but lacking the focus to the core speciality hardware (metallic components). There are 3 or and potential more regional players with 10-20 centers.

3.b Views on Market share and fragmented industry in US

Richelieu has a dominant position in Canada. Its market share is potentially around 65%. So what is Richelieu's market share in the US? And is the US as fragmented as was Canada in the 1990s?

I had an interesting exchange about this topic with Clear View Equity Research last week.

Canada is about 1/10 of the US economy in general. However if I look at the new construction start, the rate of new construction is 250k in Canada versus 1.6 million in the US or about 15%. Lets use 15%.

Richelieu sales were $1070m in Canada in 2022, and 730m in the US. Assuming a market share of around 65% (2/3) in Canada for Richelieu - this would mean that the TAM of Canada in the speciality hardware is 1.65 Billion. Lets assume that the US is typically 6.66 times (1/.15) larger than Canada, thus the TAM in the USA should be around 11 billion. So 0.73/11 is around 7% market share.

As such, Richelieu hardware market share is around 7%. Adentra has recently stated that Rubgy sales have reached $500m USD or 6% market share. Wurst group has 44 centers and is well established so we could assume that it is of similar size to Richelieu hardware. McKillian is about 1/3 of Richelieu so about 2% market share. The other 2 are even smaller but leave them at 2% as well.

Here is the table of Richelieu Hardware’ peers (wholesale distributors of speciality hardware) and my rough estimate of their market share in US:

This is based on the assumptions I described in the previous paragraph. Based on this estimate, the US is still very fragmented. The fragmented segment may also include sales of suppliers that are made directly to manufacturers without going through the regional distributors.

4. Suppliers may become indirect competitors

Richelieu distributes products made by well established suppliers. Here is a short description of key suppliers in its market:

Blum (private) : Blum is a leading supplier of products related to kitchen cabinets such as hinge, lift, inner divider or the runner system. It is distributed over 120 countries and had sales of 2.5 billion euro last year. It has one warehouse in Canada and 1 warehouse in the US.

Knape & Vogt (private): K&V is a supplier of drawer slides; wall-attached shelving for commercial, home and garage applications; kitchen, closet and bath storage; office ergonomics products and specialty hardware. expanded product offering of Hinge Systems, Lifting Systems, Drawer Box Systems and Fittings.

Amerok (private): Amerock is a supplier of cabinet hardware, bath accessories, decorative hooks and wall plates. It has sales estimated at $70 million USD.

Liberty hardware (subsidiary of Masco): Liberty hardware is a supplier of bath accessories, cabinet hardware (knob, pulls), hooks, racks, plate. It has sales of around $100 million.

Berenson (private): Berenson is a supplier of decorative hardware, drawer slide, hinges, fasteners and screws.

Richelieu hardware: Private brands and exclusive products targeted to manufacturers and retailers comprise some 60% of Richelieu offering. As such, Richelieu is on its own a major supplier of specialty hardware.

As such, Richelieu hardware is also competing with its suppliers. These suppliers may also sale directly to manufacturers to remove a middle man. Blum offers services to guide customers in the purchase of their products for example.

In the retail business, all the suppliers compete head-to-head with Richelieu Hardware.

Conclusion:

The main direct competitors of Richelieu Hardware are the Wurst Group and Rugby. Blum is a well established supplier of Richelieu Hardware and is likely a direct competitor, selling directly to Richelieu hardware’s customers. Blum and the Wurst Group have worldwide reach to over 120 countries and as such have larger scale than Richelieu Hardware. In my opinion, Richelieu is more innovative and has a much broader and attractive catalogue of products.

In a major economic downturn, like the GFC in 2009, Richelieu may see a small reduction in sales, but sales are geared to the improvement/restoration/repair market and are much less cyclical.

The margin are stable and it does not fluctuate much over the economic cycle. The company has guided to a small reduction of EBITDA margin by 100 to 150BP in 2023 versus 2022. 2021 and 2022 have historically high margins.

The US is still fragmented in the US and Richelieu Hardware will continue to take market share, but contrary to Canada, it may not achieve the same dominant position as in Canada.

Part 3 will cover the valuation aspect of Richelieu Hardware.

Feel free to leave some comments and wishlist for PART3!

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested

Google translate is pretty good! I am particularly interested by distribution business, especially distribution business that are addressing the need of restoration, repair, inprovement so non cyclical. My next few write-up will be related to those. I am also watching closely Q1 results of US banks, this should come out in 1-2 weeks. There are good value there. I have followed banks for a very long time.

Again, excellent write up. Great information on the competitors - thank you!