$APN Aplisens a growing industrial sensor manufacturer at a very attractive valuation

$APN Aplisens a growing industrial sensor manufacturer at a very attractive valuation

$APN has seen a surge of sales in 2022 and 2023 (first 6 months) which had a big impact in the profit line where eps has doubled since 2020. Stock trades at a very attractive low 8.8x PE.

Aplisens is a Poland industrial sensor manufacturer trading at the Warsaw Stock Exchange (WSE:APN) who has seen a surge of sales in 2022 and 2023 (first 6 months) which has translated into an even higher increase in profits. My fellow investor @Sutjeinvestor (twitter account) mentioned this name to me in June/July - he also took a position in this stock - and I quickly realized that it ticked all the boxes of a new investment. Many thanks to him!

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

Executive Summary

This stock ticks basically all the boxes of a quality growth company I like to invest in:

An industry I understand with moat: Aplisens designs and manufactures highly accurate sensors in mission critical industrial applications and reports the information through wireless communication. This is an industry that I am very familiar with, as I worked in this industry as a wireless engineer and architect having develop a proprietary wireless communication protocol to carry back sensor information in industrial and harsh environment. Those sensors are very accurate, reliable and can operate in very harsh environment. Once an industrial company adopts such a sensor for a specific application, and is satisfied with the product, it is very unlikely that this company with switch for another product.

Top line growing at a 10-15% rate or more. Recent years match this rate as well as the management estimates for the following years.

Bottom line: A top line growth translates into an equal or larger rate of increase in profit (positive operational leverage).

Skin in the game: Adam Żurawski - the current CEO - has 23.9% of the stocks.

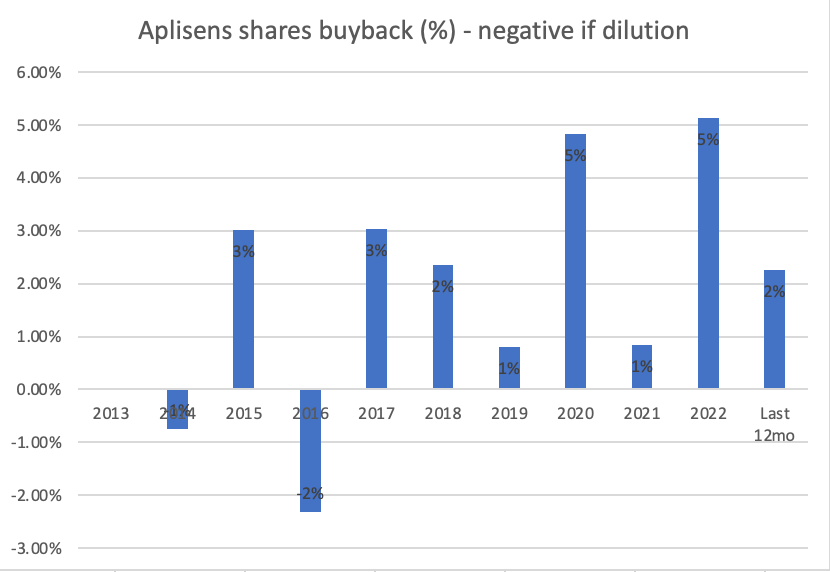

Buying back shares: Aplisens has bought 16% of the shares in the last 4 years and this has actually accelerated to 5% in 2022.

Under-followed small cap priced at a PE below the growth rate. This stock is actually a micro-cap trading at a market value of 220m zloty or 51m USD.

Acceptable RoE which allows to grow without leveraging the balance sheet

Lets revisit those points

The Industry

Aplisens manufactures sensors for industrial applications often mission critical application.

Here is the list of some of the products and their applications:

Pressure sensors: Pressure sensors and transmitters to monitor the pressure in gases, vapors and liquid environment. Applicable in many industry like oil and gaz, petrochemical, Food industry and heavy industrial application. Can sustain up to 1200BAR pressure.

Level sensors: Probe used to measure liquid levels in tanks, deep wells. One application is tank level in vessels.

Temperature sensors: Temperature sensors that can operate in a very wide range of temperature (-70 celsius to 500 celsius) with a high degree of accuracy 0.2 celsius. It comes with a hart transmitter. Hart is a robust low rate wireless protocol for industrial application.

Electromagnetic flow meters: Magnetic flow meters are used in a wide variety of applications. Some common examples include water, process water, wastewater (treated and untreated), custody transfer, chemical and corrosives, slurries, and other general industrial uses. These flow meters are used in many industry including oil and gaz:

Positioner: Electro-pneumatic positioners are used with rotary air actuators to accurately position control valves used in throttling applications.

Automotive products: Aplisens also makes sensor for the automative industry such as a fuel tank theft alarm.

All these products comes with wireless communication capability using the industry standard Hart protocol. In each market it operates, Aplisens must seek proper industry certification.

As I said in the beginning, these sensors must be able to operate in very harsh environment and provide very accurate readings.

Here is an example I was faced during my previous work. Imagine you want to monitor with sensors (temperature or pressure) a rotating hydroturbine surrounded by high pressure water and metallic structures, and you need to relay wirelessly the information back to a control room. These sensors must be ultra robust and reliable. These are mission critical application that monitors the health of the turbine to decide when to do preventive maintenance before a major failure occurs.

There are many applications like this in the field of

Oil and gaz extraction and transport

Power and hydro plant,

Water management industries

Petrochemical site

Shipbuilding

Heavy industries like mining, metallurgy, paper

Food industries

Once an industrial company adopts such a sensor for a specific application, and is satisfied with the product, it is very unlikely that this company with switch for another product. I believe there is a good level of moat in this industry.

Top line growth

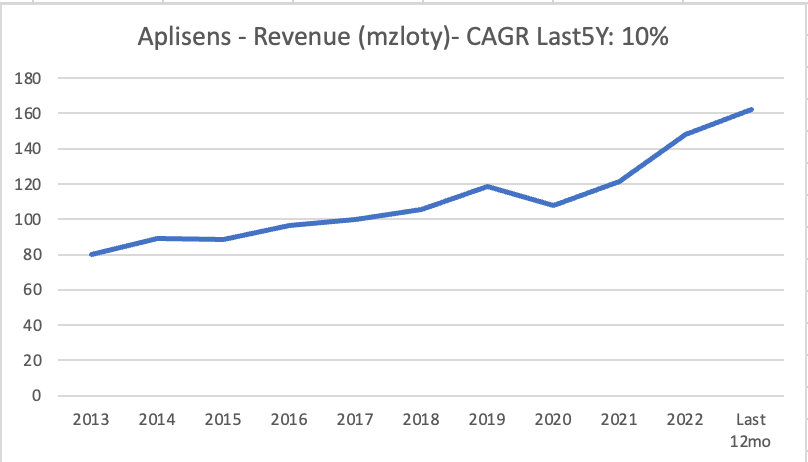

I want to see a top line growth of about 10% or more typically. Aplisens meets this criteria for the last 5 years with 10% growth CAGR. If you look at the last 10 years, this is down to 7%. There is a surge of growth since 2020, if you take the last 2.5 years (until June2023), sales is up 17.7% annually.

What can explain the slow growth from 2013 to 2018 and the acceleration fo growth in the last 5 years?

The first market mentioned by Aplisens in their investor material is oil and gaz extraction. Also the CIS market is very important for Aplisens, which regroups ex-Soviet Union countries very rich in oil and and Gaz.

Here is Brent crude oil price for the last 10 years. So starting in 2014, we have seen a sharp drop in the Brent crude oil price which has not meaningfully recovered until 2018. Extraction often lags crude oil price. So it likely that the #1 market of Aplisens products was impacted by the oil and gaz industry downturn. I am seeing the same phenomena for Logistec, where oil and gaz related cargo have been increasing in the last 2 years.

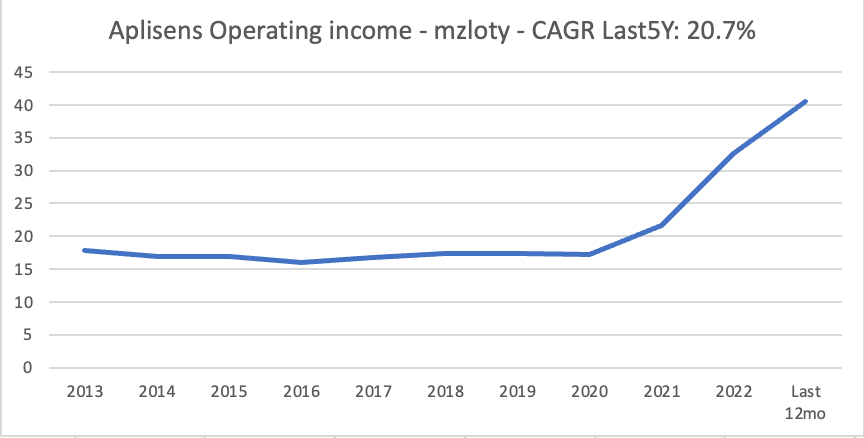

Profit and EBITDA growth

The operating income for the last 10 years is shown below. The last 5 years CAGR is 20.7%, and so we see a positive operational leverage to the profit line, i.e an increase in the top line translates into a larger increase in profit.

Also the operating income margin has ranged from 15% in 2019 to 25% in the first half of 2023. Those are healthy margin.

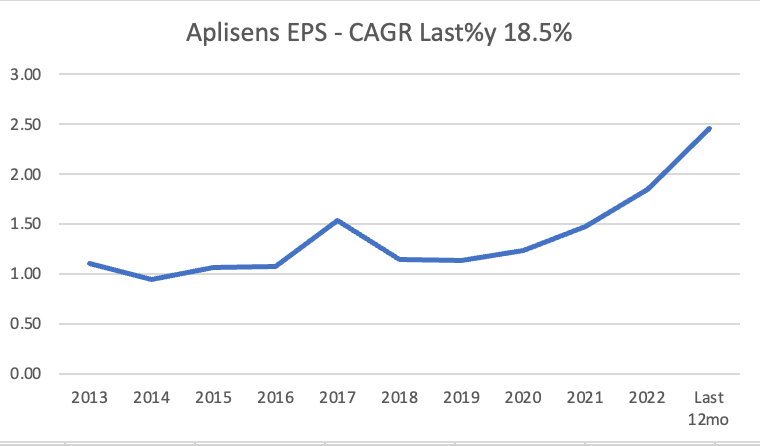

Apliens has made significant buybacks in recent years where Aplisens has bought 16% of the shares in the last 4 years and this has actually accelerated to 5% in 2022. This translates into steady EPS growth as shown below:

Please note that 2017 results were inflated by an extraordinary gain.

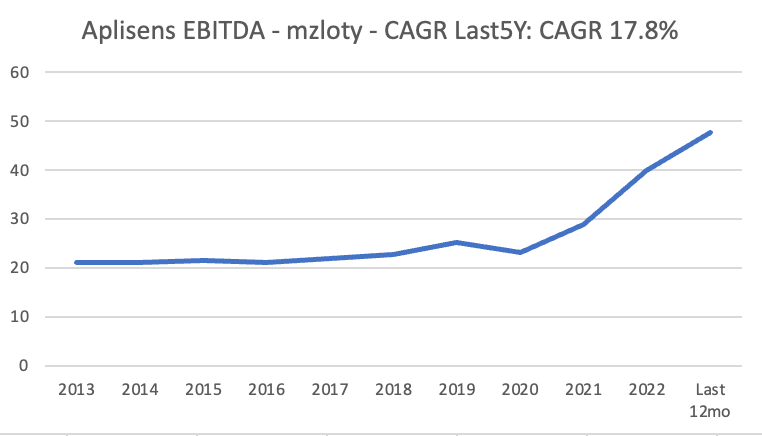

EBITDA has grown steadily in the last 5 years at a CAGR of 17.8%.

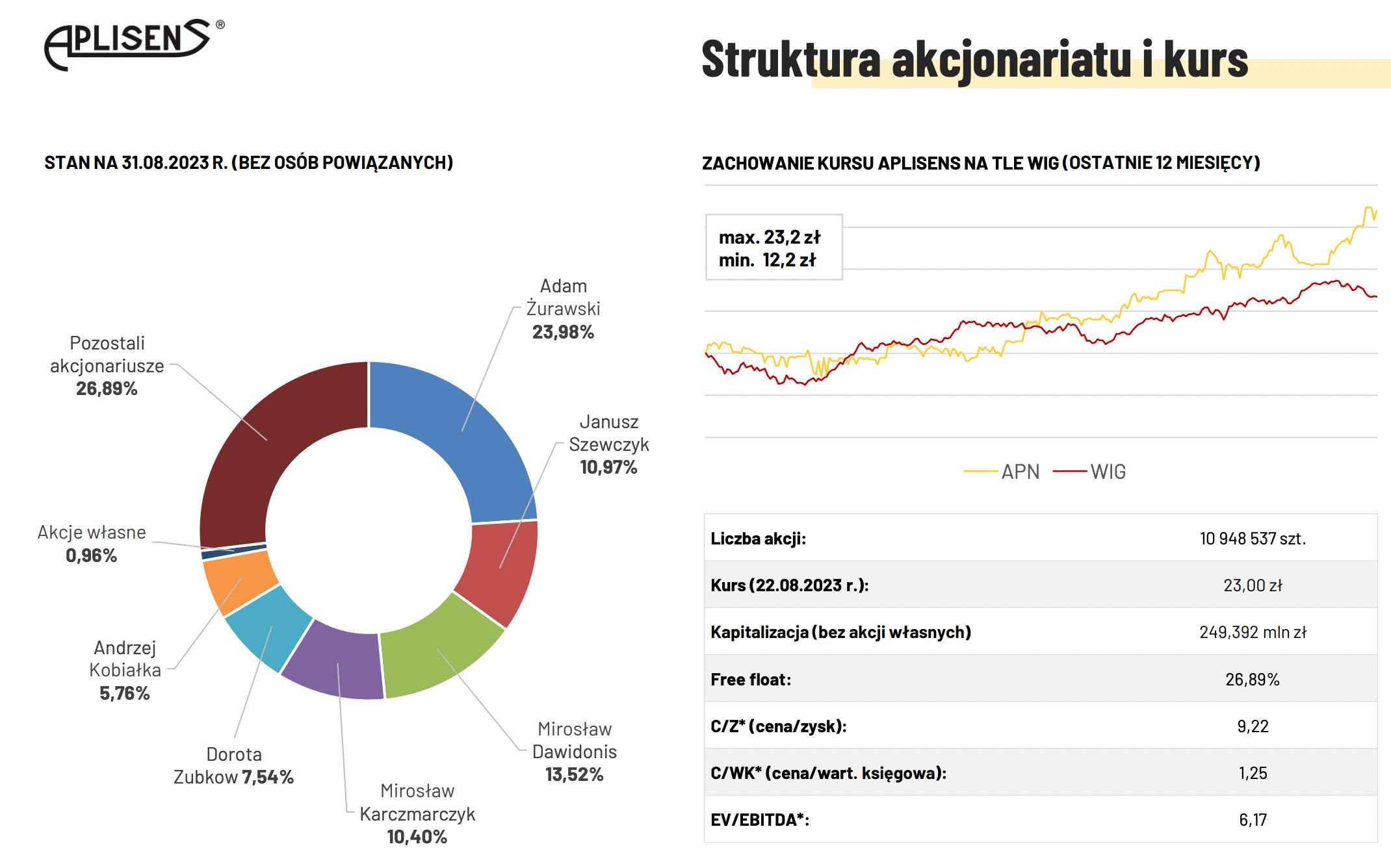

Skin in the game

The following chart is an extract from the latest presentation for investor.

So the majority of the shares are owned by 6 insiders, and the largest owner is Adam Zurawski, the current CEO. 26.99% of the shares are held by the public. 1% of the shares were bought recently and are treasuries shares. The other significant shareholders are on the board. So all insiders have interest well aligned with the general public.

Geographical Sales Split

The domestic market (Poland) is the largest market for Aplisens with 30.7 million zloty in the first half, up 29.2%. This represents 38% of total sales.

In second is the European Union, with 19.8 m zloty up also 29.2%. Then the ex soviet union countries with 16.8 m zloty down 10.4%. Please note that Aplisens has stopped selling sensors to Russia. And finally the Rest of the world with 12.8m up 66%. Aplisens is trying to obtain new certifications to help penetrate the North American market.

Recent Acquisition

Aplisens bought late in the latest semester another manufacturer of sensors namely APAR Control at a buying price of 1x sales (11.6m zloty of revenue) and at about 5.5x earnings. APAR control makes transducers, meters, regulators and recorders. APAR control is based in Poland.

Shares Buyback

Aplisens has been buying back shares steadily especially in the last few years. It bought back 5% of the shares in 2020 and 2022.

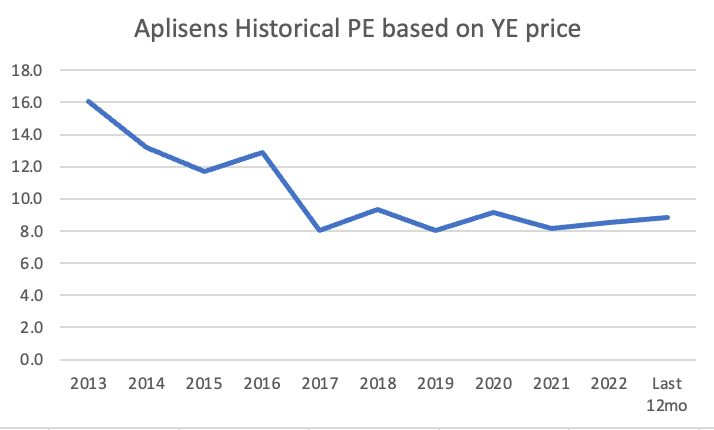

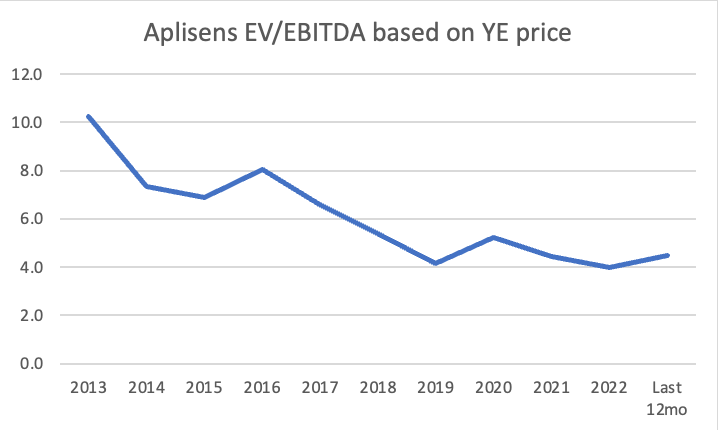

Valuation

The following are historical PE and historical EV/EBITDA. We like to buy a stock at historically low ratio.

PE of last 12 month trailing results is based on current price as the time of writing. The stock is currently trading at 8.9x trailing earnings which is an almost historical low.

The stock is also trading at an historical low in terms of EV/EBITDA:

Very attractive valuation

Aplisens has been growing at 18% operating income CAGR in the last 5 years and is currently trading at less than 9x earnings, and as such it is trading at a PEG of 0.5 - PE Growth ratio. Anything below 1 is very attractive. On top of that, management has been buying back up to 5% of the shares and dividends at current price is around 3.8% (0.80/21.6).

No debt and acceptable RoE

The company carries no debt - it has a current cash balance of 11m zloty and RoE is at an acceptable rate of 13.4% so it can sustain a growth rate of around this level of the top line without leverage.

Final words:

This is an industry I know well, with a good level of moat which I believe can provide good protection from new intrants. As a disclosure, as soon as I became aware of this company in June and its current valuation and growth, I started to build a position. Do your own due diligence. I hope my analysis might help you understanding my thinking process and entertain you in a new industry. This is a micro-cap so if you decide to purchase this stock, trade lightly, sparsely in time, and do not chase up this stock. Aplisens is micro-cap trading at a market value of 220m zloty or 51m USD. There are only 12.5m USD of float.

Cheers,

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested.

Interesting, I wonder if the last two years is a bit of a cyclical high in projects as it seemed that the Ukraine war pushed for industry and construction of Infrastructure in Eastern europe? Any feedback on that?

where do we see future growth. Did you see that in the Annual reports, Thanks

Fascinating company and great write up, thanks! Do you have any insight into the competitive landscape and their competitive advantage?