Business Update and 2023 Estimates on Serial Acquirer $RCH Richelieu Hardware

Business Update and 2023 Estimates on Serial Acquirer $RCH Richelieu Hardware

2023 is one of those very rare year with 2009 where $RCH is seeing YoY decrease in sales. The pandemic boom were extraordinary for the renovation business that 2023 will not be able to replicate

Will go through Q3 numbers which were released on October 5th 2023 and we will do some projection for the rest of the year 2023, but first lets address the big picture in terms of long term growth in this downturn year.

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

The Big Picture

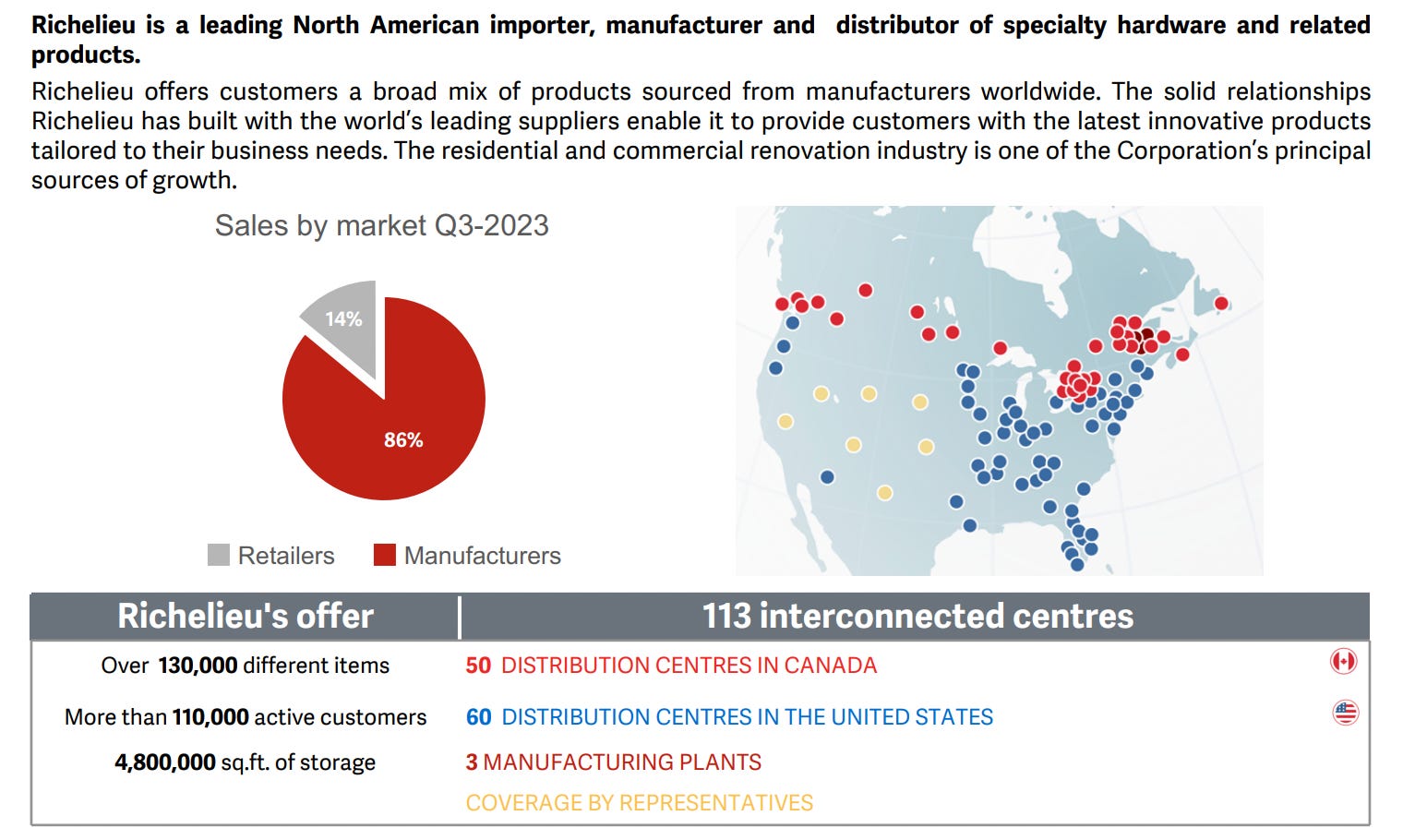

Every quarter, the management includes the latest map of the distribution centers. You can see how little the Pacific and Mountain timezone in USA are covered by Richelieu Hardware. Two of the largest states, Texas and California are barely covered for example. There is still a lot of growth ahead of us.

Richelieu USA represents only 41% of sales, the rest being in Canada. The US is about 8x larger in terms of population than Canada. As such, if Richelieu were to achieve the same dominant market share as in Canada, The US would be 12x larger in terms of sales (8x 59%/41%). As seen in part 2 of my analysis of Richelieu published in Richelieu Hardware Part 2 on Risks ,

there are only a few challengers with a similar product breadth and scale in the very fragmented US market that Richelieu operates in, and my belief is that these players will take a larger and larger piece of the business over time and Richelieu Hardware is in the best position to replicate what it has done in Canada in terms of market dominance.

In Q3, the number of distribution centers are come down from 62 to 60 in the US. Management is always looking for ways to reduce costs and has consolidated two distribution centers - in Atlanta and in Nashville.

Q3 Sales and EBITDA Results and Industry Update

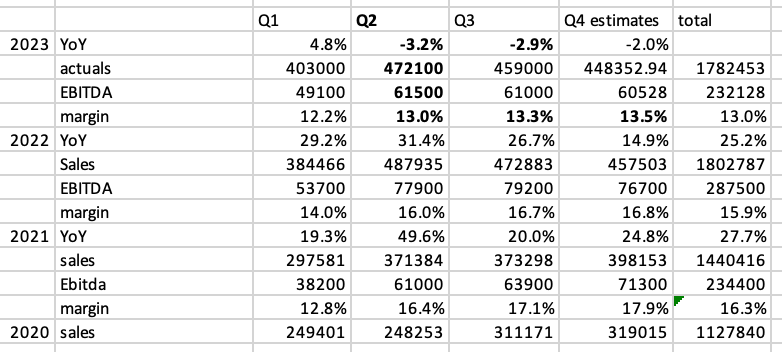

Here are the sales and EBITDA figures for the last 12 quarters including my Q4 estimates for 2023. Figures are in thousands Canadian dollars.

Q3 Sales is down 2.9% from 2022 but up 22% from 2021.

The renovation industry is down significantly from 2022. For example, the leading home improvement retailer Home depot is projecting Sales and comparable sales to decline between 2% and 5% compared to fiscal 2022.

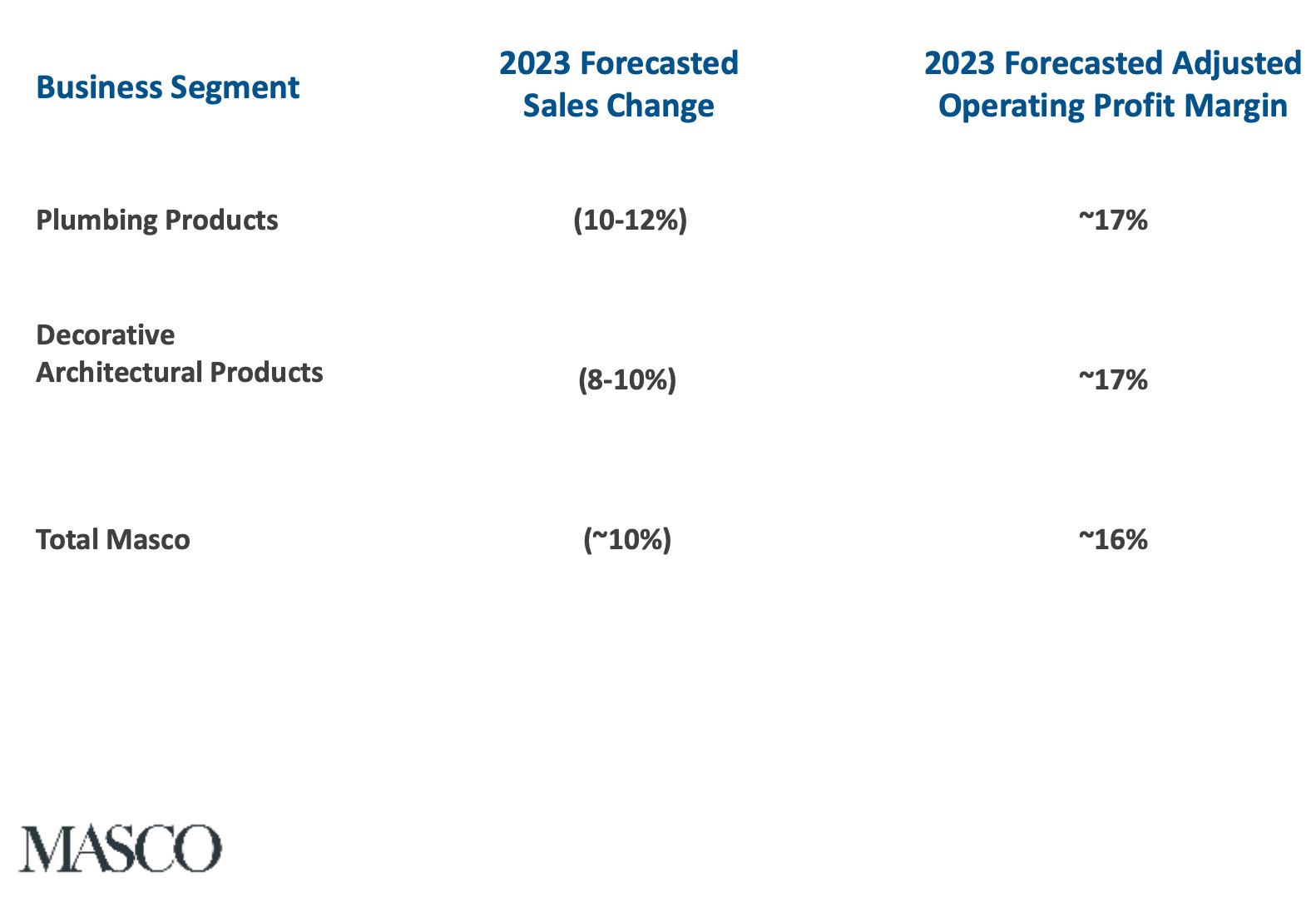

Masco, a leading manufacturer of home improvement and plumbing products is forecasting 10-12% reduction in sales for plumbing product and 8-10% decrease for the decorative segment which includes the Behr® paint; Delta® and Hansgrohe® faucets, bath and shower fixtures; Kichler® decorative and outdoor lighting; and HotSpring® spas.

So, Richelieu is likely outperforming the market with a 2.9% drop in sales.

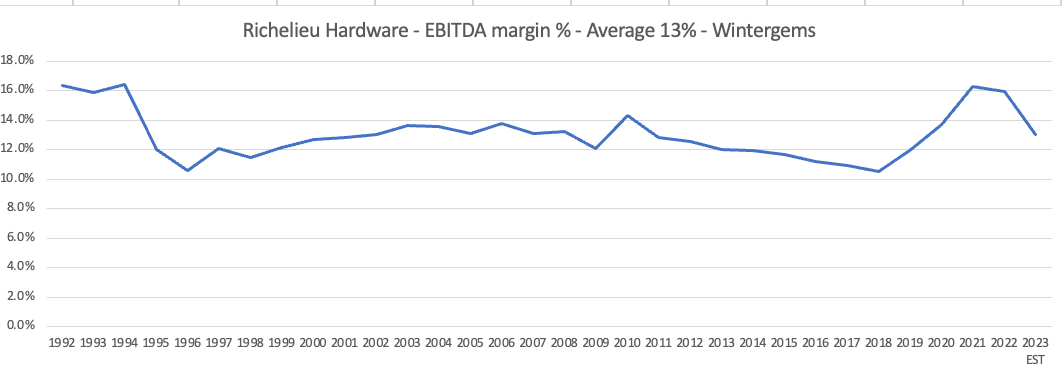

Richelieu has seen a sharp drop in EBITDA margin in Q3 compared to 2022. The pandemic years (2021, 2022) were extraordinary in terms of margin accros the industry. Q3 EBITDA margin is actually up sequentially compared to Q2 (13.3% versus 13.0%), although sales is lower. This is likely due to the sharp reduction in inventory (and temporary warehousing cost) and the operational efficiency implemented during the quarter including the consolidation of distribution centers.

For Q4, I am now projecting a slight decrease of sales YoY (-2%) and some additional improvement in EBITDA margin at 13.5%. Although management is guiding for stable EBITDA margin at around 13.0%. Overall for the year, EBITDA margin will be 13.0% due to seasonal weak Q1.

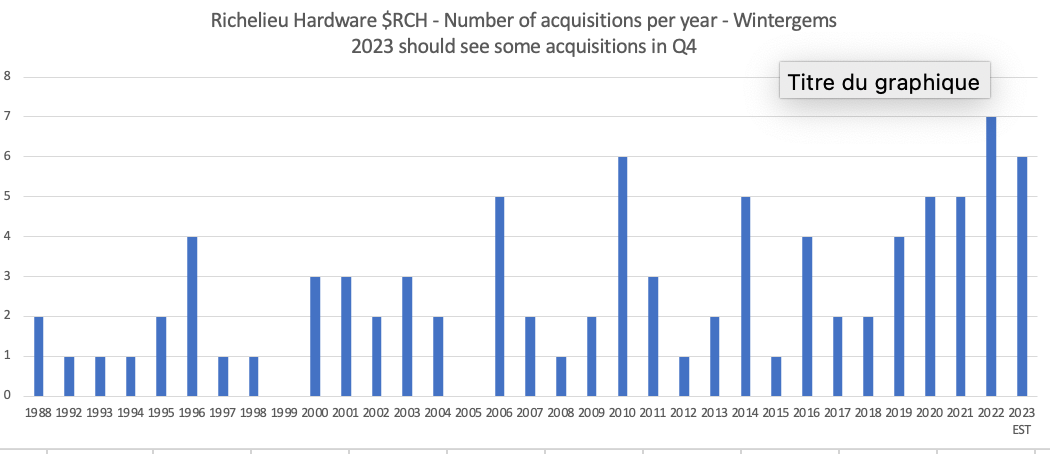

At the call, management is seeing stabilization of sales at least until mid 2024. We should expect renewed activity on the M&A front as bank overdraft is almost back to zero. Management has indicated that the M&A pipeline is strong.

Update on Inventory and Cash Management

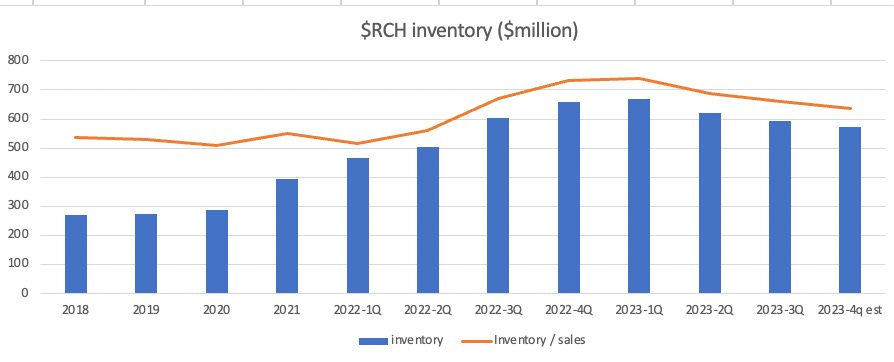

Every quarter since the beginning of the year, management is working hard to reduce inventory. This had a positive effect on operating cash flow as well as reducing extra warehousing costs.

Here is the inventory value in million Canadian dollars for the past 7 quarters and year end inventory from 2018 to 2021. Inventory was at 660m at the end of 2022. It reached a peak of 667m in Q1 2023 and it is now 594m at the end of Q3 - down 66m from the end of 2022. Management had a goal of 60-80m reduction at the beginning of the year. It is now guiding in the upper range and is looking for a reduction of 80-85m for the year.

Q3 was amazing in terms of cash inflow where operating activities represented a cash inflow of 103.5m during the quarter.

As a result, net debt (bank overdraft minus cash plus LT debt) is now -16.8m down from a peak of -139m in Q1.

Projection for Q4 and 2023

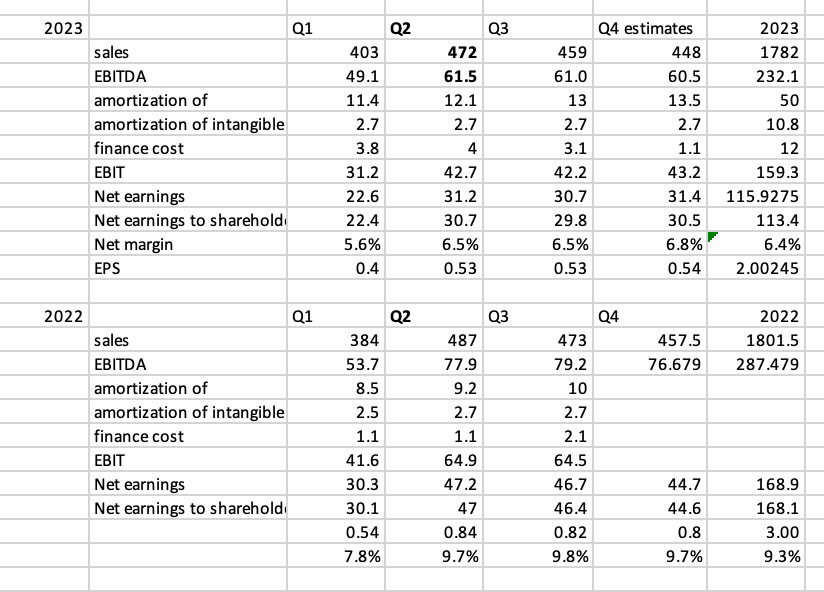

The following shows Sales, EBITDA, amortization, financial expenses and net earnings for the last 7 quarters as well as the my projected figure for Q4 and 2023.

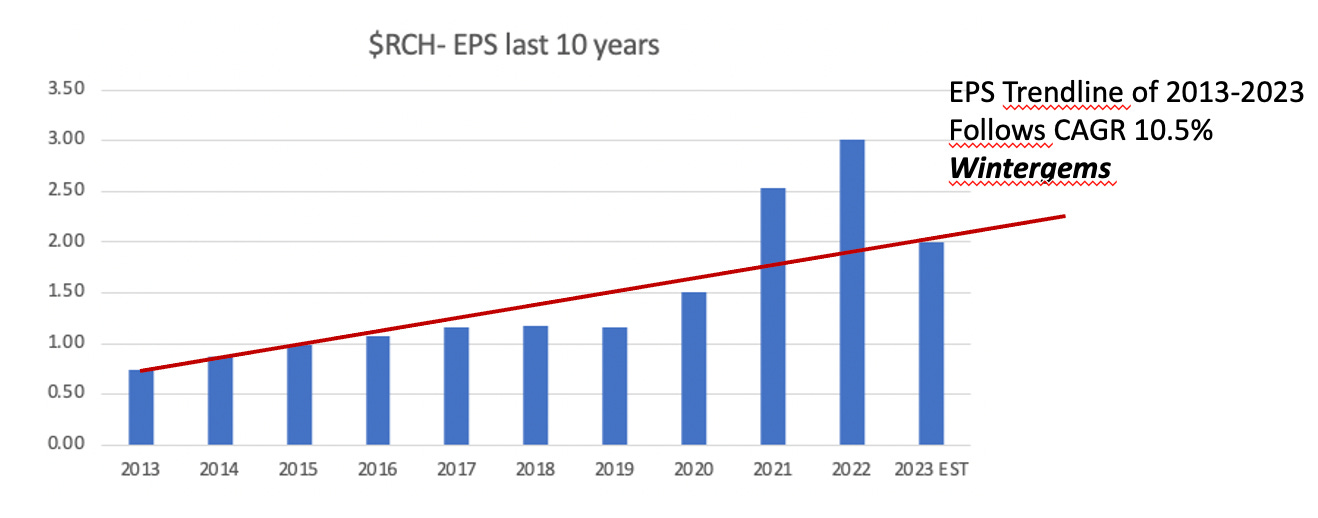

For Q4, I am projecting EBITDA margin of 13.5% as explained earlier, a continued increase in amortization of tangible assets sequentially as current trend, stable amortization of intangible, and a sharp decrease in financial cost. This will result is net earnings margin of 6.8%, up sequentially from Q3 and EPS of 0.54. This will result of an EPS of 2.00 for 2023.

Consensus from the few analysts tracking the stock are projecting 1.97 EPS for 2023.

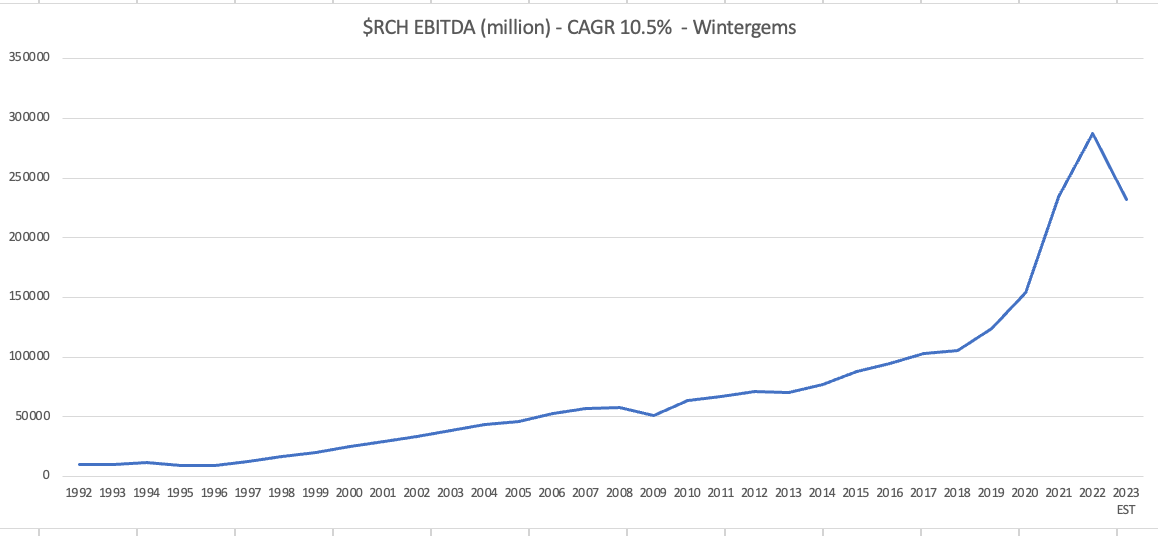

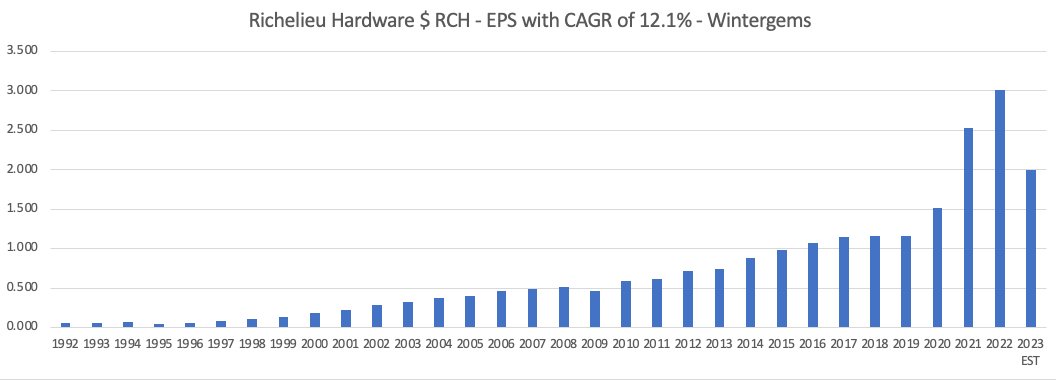

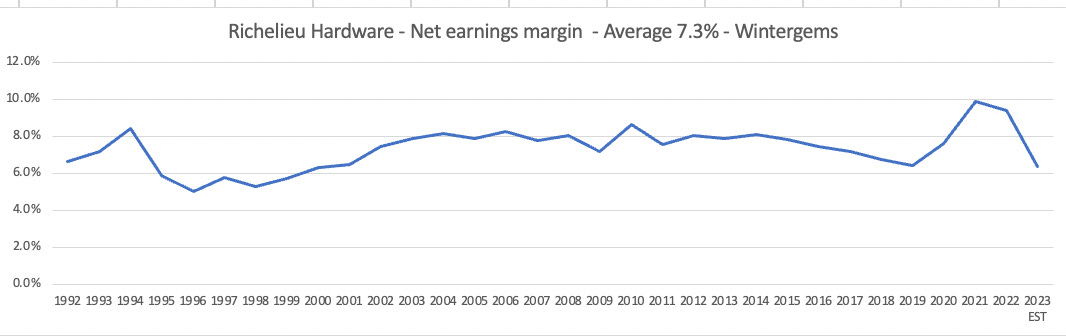

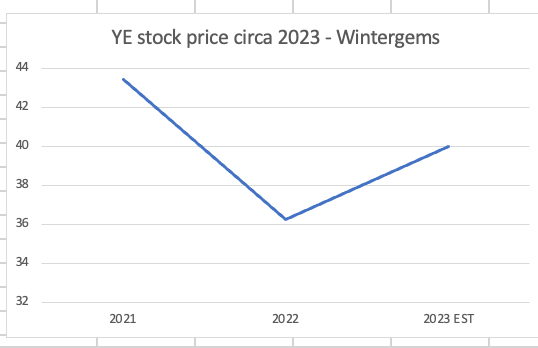

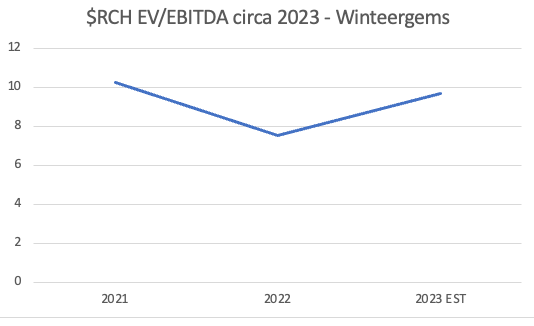

Charts Extravaganza

To complete the analysis, I am providing a list of charts often gathering data over 31 years of historical data that I have preciously constructed. I am adding 2023 numbers using my Q4 projection. Should be close enough.

No comment just data…

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested