PART3: Is Logistec a compounder?

Valuation extravaganza (EPS Growth, PE, P/S, RoE, management ownership, debt)

In this last article on Logistec, the author is looking at Logistec from different angles to assess whether this company is a compounder. Compounders are companies that can deliver sustainable and long-term eps growth with a good RoIC.

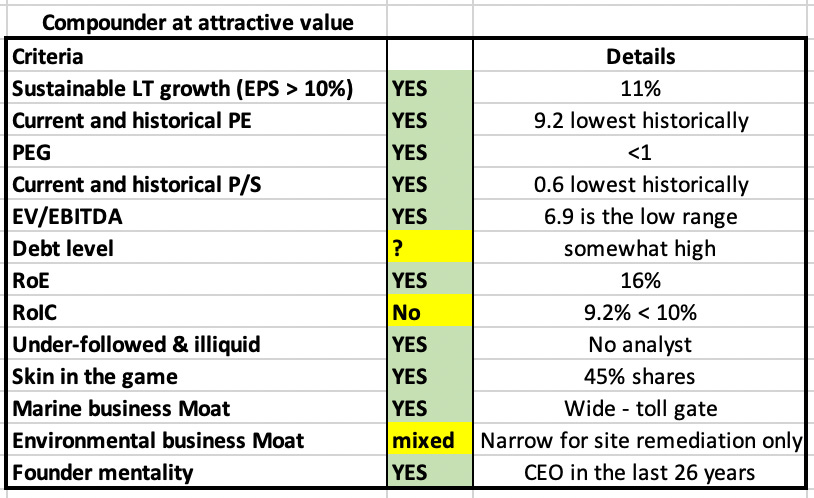

The following is a list of criteria to assess whether the Company is a compounder and is attractively priced.

Sustainable EPS growth discussion (EPS growth > 10% CAGR)

Current and historical PE and PEG

Current and historical P/S

Current and historical EV/EBITDA and Debt level

RoE and RoIC

Under-followed and Illiquid

Competitive advantage and Moat

Skin in the game - Management ownership

This following is a deep dive article on Logistec. The article constitutes the authors’ personal views and is for entertainment purposes only. Please refer to the disclaimer at the end of this article for more details.

Sustainable EPS growth discussion

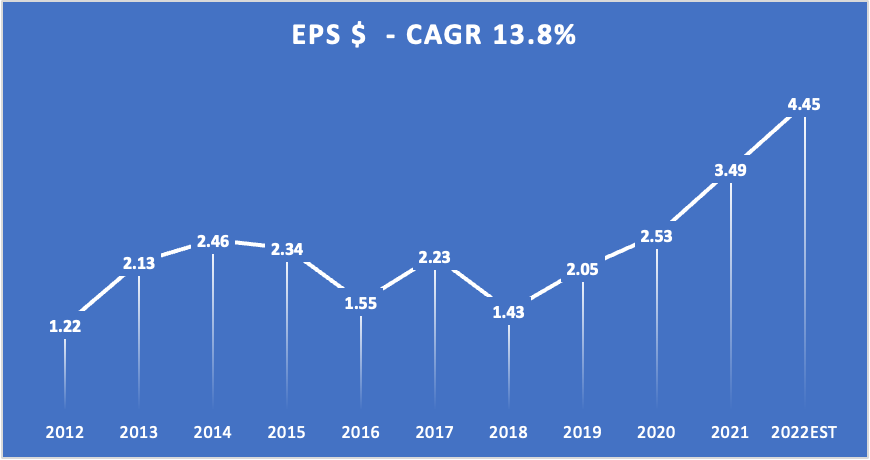

The following figure shows the Earnings per Share (EPS) for Logistec as a whole since 2012.

The 2022 EPS number (4.45$) is based on the author’s estimates. Currently, the trailing 12mo EPS is 4.09$. The marine business is running at a much stronger pace in 2022 than in 2021, as such it is expected that marine EBT in Q42022 will be much higher (estimates $15 million for Q4 2022) than $2.3 million (actuals in Q42021). As mentioned previously in Part1, EBT was penalized by almost $6 million by one time expenses in the 2021 Q4. The environmental business is running a bit slower in 2022 than in 2021, as such the author estimates that this unit will generate $10 millions EBT in Q42022 versus $13.8 million in Q42021. Those estimates are conservative but there is a risk that the drop of EBT generated by the environmental business could be more significant. The Company will publish annual result in mid March.

UPDATE: On March 22nd 2023, The company has released EPS of 4.12 so below my estimates but still much higher than 2021.

2018 EPS was a real low point in terms of earnings, due to the FER-PAL acquisition struggle. 2016 was also difficult where both businesses had seen sales pressure. From 2018, the EPS has grown very steadily at a very high rate. Part 1 demonstrated that the marine business EBT has grown at a rate of 14% + CAGR since 2012. Furthermore, the growth being about 2/3 organic and 1/3 originating from bolt-on acquisition, it is likely to project that the marine business can compound at a rate ranging from 10% to 15% over the next five (5) years. The contribution of the marine business to the overall EPS is projected to be 70% in 2022.

For the environmental business, the author is much more conservative and would expect a mid single digit EPS growth through margin improvement and some revenue growth.

As such, Logistec as a whole could steadily grow its EPS by 10-12% over the next 5 years with some bolt-on acquisitions in the marine business.

Current and historical PE

The following shows the historical PE ratio based on the historical year end stock price. For 2022, the ratio is based on the author’s 2022 estimates and the current price (January 27th closing price).

In the past 10 years, the PE ratio (year end price with trailing 1 year EPS) ranges between 10 and 30.8.

If instead, we derived the PE ratio using the year end price with the trailing 2 year average EPS, we get a smoother curve:

In the past 10 years, the PE ratio (year end price with trailing 2 year EPS) ranges between 9.5 and 23.7.

In any case, we can conclude that with a current PE 9.2 based on the author 2022 estimates, Logistec is currently trading in the lower bound of its historical PE range.

From a classic PEG ratio, Logistec is also trading below 1 based on LT growth of 10-12% and a PE of 9.2.

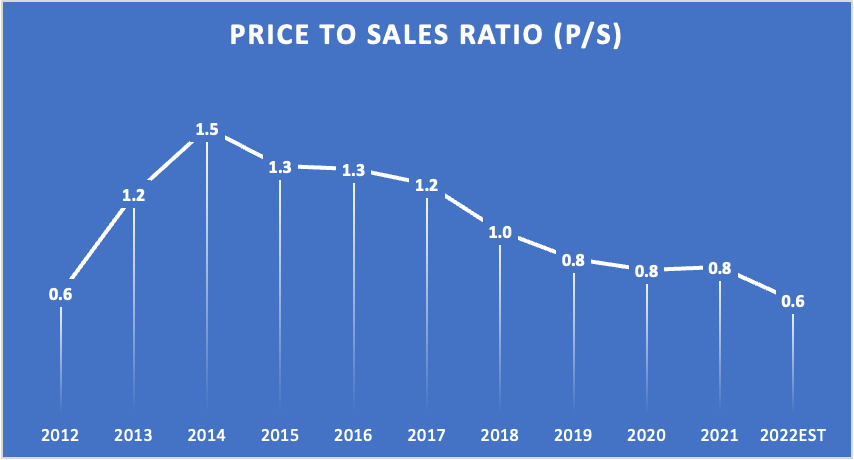

Current and historical P/S

Looking at the historical Price to Sales Ratio (year end price), we also find that Logistec is trading in the lower bound of the P/S range.

Current and historical EV/EBITDA and Debt level

Looking at the historical EV/ adjusted EBITDA ratio, the current EV / adjusted EBITDA is the lower part of the range. However, Logistec has taken a lot of debt to buy the recent acquisitions made during the 2016 to 2021 period (most notably FER-PAL in 2017, GSM in 2018, APG in 2021). As such, the current EV/EBITDA is 6.9 which is low but the author would like to see management using their healthy cash flow to reduce LT Debt.

Long Term Net Debt stands at $246 million as of September 2022.

RoE and RoIC

If we take the trailing 12mo, the Return on Equity (RoE) stands at a healthy 16%.

The Return of Invested Capital stands at 9.2%. This business is capital intensive and a higher RoIC would be desirable.

Under-followed and Illiquid

There is no analyst following this stock and Logistec have not done a secondary offering since the 1970s! The last forward earnings estimates from an analyst was done in 2010.

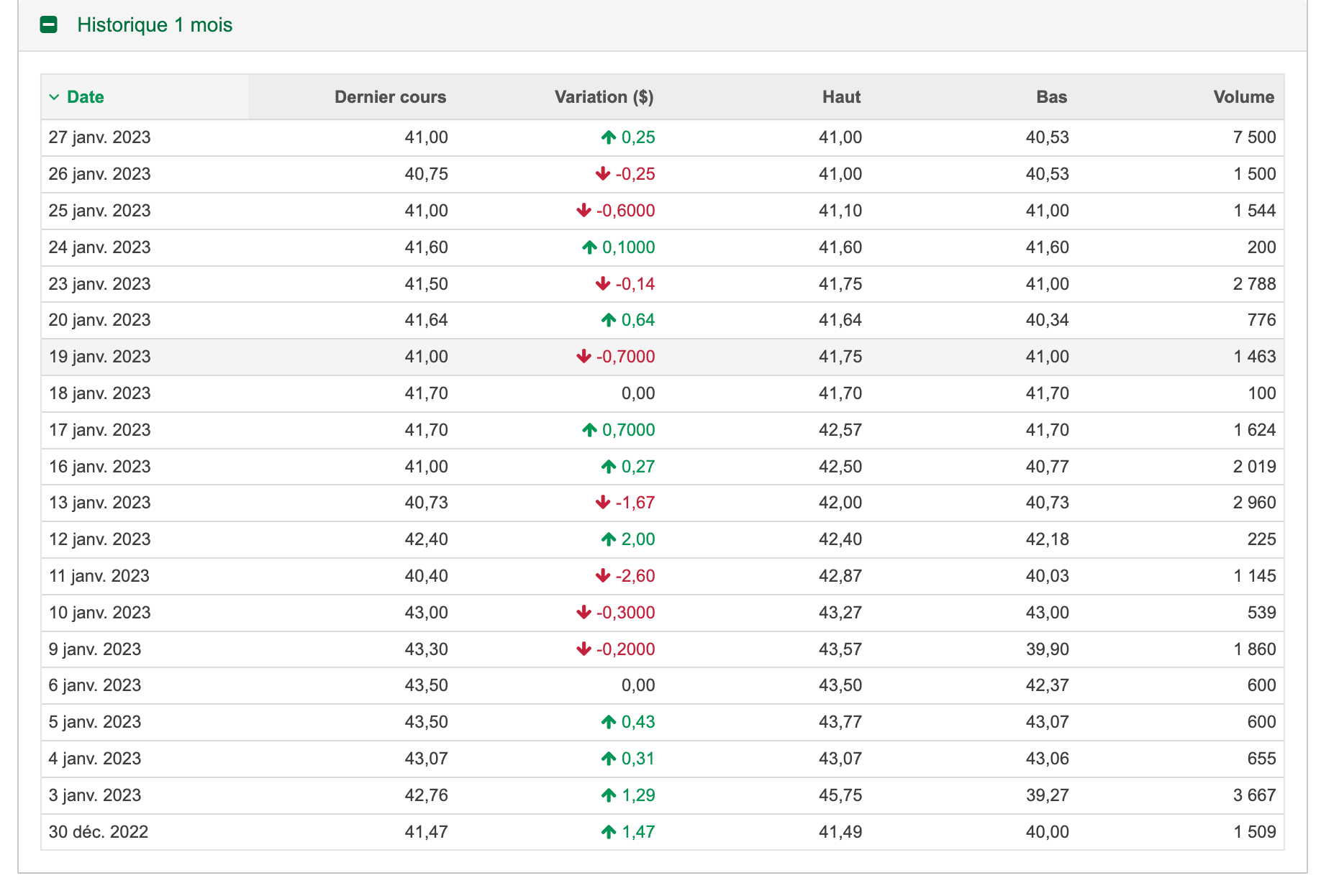

Logistec B shares (LGT.b) is thinly traded in the Toronto stock exchange with an average volume of 2000 shares per day or about $80 000 per day. Some weeks we can get 30000 shares traded. The spread is around 2.5%. So trade carefully.

Historical trades last month.

This stock is illiquid!

Competitive advantage and Moat

As discussed in Part 1 and Part2, the marine services business is very resilient and diversified being spread over 53 ports. This maritime network has taken decades to put together. These ports serves a wide array of different cargos: raw materials, forest product, oil and gaz goods, oversized cargos, containers, and so on, covering the Great Lakes, The St-Lawrence River, the Eastern Canada, the US East Coast and the southern states along the Gulf of Mexico. This is a unique network not easily replicable.

Ports are very nice business, and are often the only way for certain goods to enter a country or a region. It is similar economically to a toll gate or a toll highway. Once the Company has the concession, it can charge for a very long time a fee based on the volume of cargo going through the port. The marine business has a wide moat and is a nice repeatable business.

As for the environmental business, the author concluded in part2 that only the site remediation and the dredging and dewatering sub-segment had a narrow moat.

Skin in the game - Management ownership

Logistec is a family owned operation. The family controls 45% of the total shares and 76.7% of the votes through Sumanic Investment inc. The current CEO, Madeleine Paquin, has been CEO since 1996, and has spearheaded the company for the last 26 years. Madeleine Paquin currently owns 33% of the Sumanic investment shares. The other 2/3 is owned by her sisters.

So is Logistec a Compounder and attractively priced?

The following table summarizes the author findings:

The marine business is a true compounder, although it is not an asset lite business and requires to reinvest a good portion of the profits back into the business to grow. However, the capital reinvested reinforces the moat over the long term and the business is repeatable.

The environmental business is less attractive and requires contracts to be won with long sales cycle.

The marine business is a true compounder business and represents 70% of the Company EPS. Therefore, should Logistec be considered a true compounder as a whole? The author believes so and would hope that the management prioritize the marine segment even more.

Disclaimer: The above article constitutes the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested

Hi, great writeup. One Qeustion: I stumbled across the "putable minority interests" relating to the FER_PAL acquisition (Note 25 of the annual report).

Do you have any idea what the parameters of that deal is ? In 2021, ~25 mn retained earnings disappeared because of this.