Richelieu Hardware $RCH Q2 update

Richelieu Hardware $RCH Q2 update

This serial acquirer and compounder has published Q2 numbers in line with expectations. Navigating post COVID boom flawlessly.

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. Please refer to the disclaimer at the end of this article for more details.

Richelieu hardware $RCH has published good results for Q2.

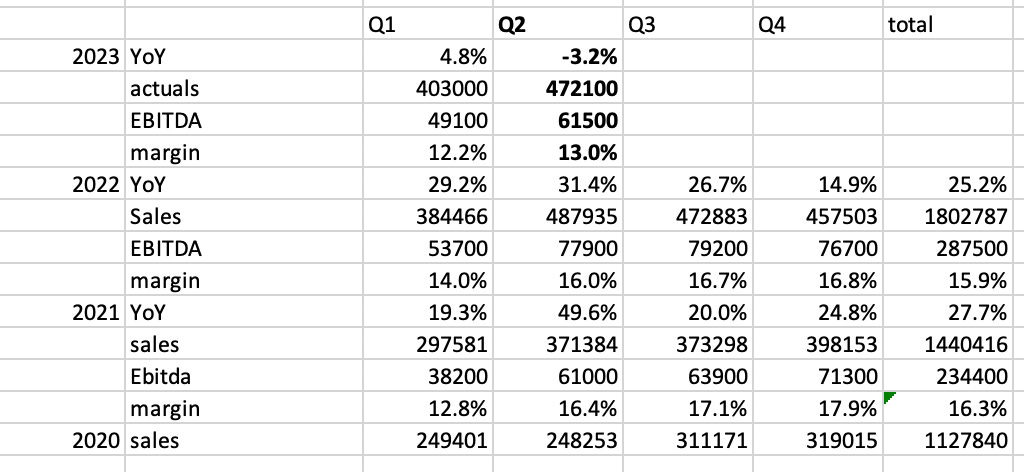

Here are the results of Q2 as well as for the last few years.

Sales

Q2 of last year was the best result in the company history and it was expected that due to deceleration in new homes build and renovation, both Home Depot and Lowes have seen rare negative same store sales in the last quarter, that we would see a reduction in sales in Q2 versus previous year.

The reduction was actually a bit less than what I expected last month as published in my post here :

https://wintergems.substack.com/p/part-3-richelieu-hardware-valuation.

In that post I had projected a -6% reduction of sales versus last year but the reduction was -3.2%.

Margins

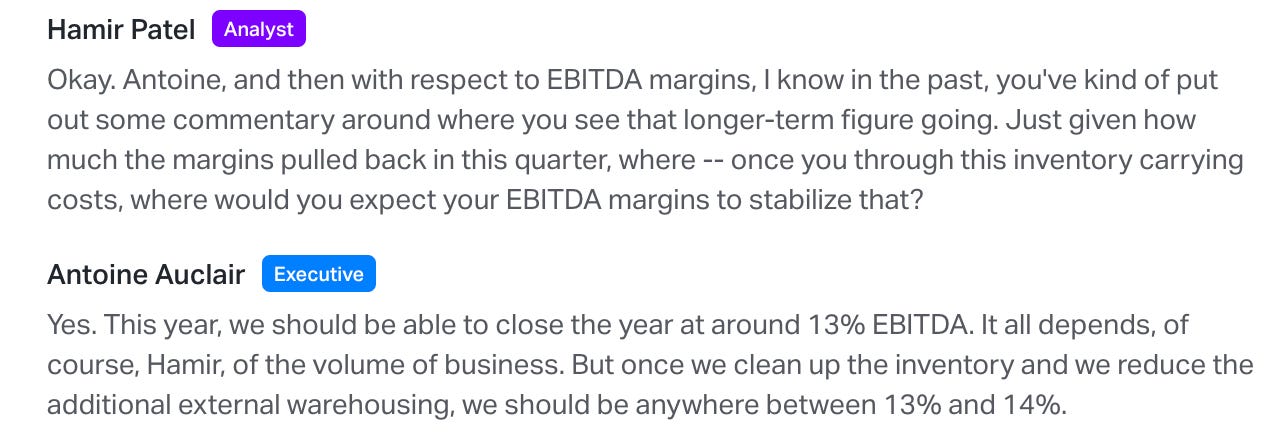

On the margin side, EBITDA margin stood at 13% versus 16% last year. Management has guided margin to be more in line with historical margin of 13-14% range. Last year margin of 16% were exceptional due to the strong demand during the COVID era (and supply constraint).

During the conference call, management has guided to a 13% EBITDA margin for the whole year and somewhere between 13-14% as an ongoing basis.

Surplus of inventory is costing around 6 million per quarter right now. 4 million due to the extra cost of renting temporary location and the additional back and forth and 2 million of extra cost of interest. That 2 million is not impacting EBITDA of course.

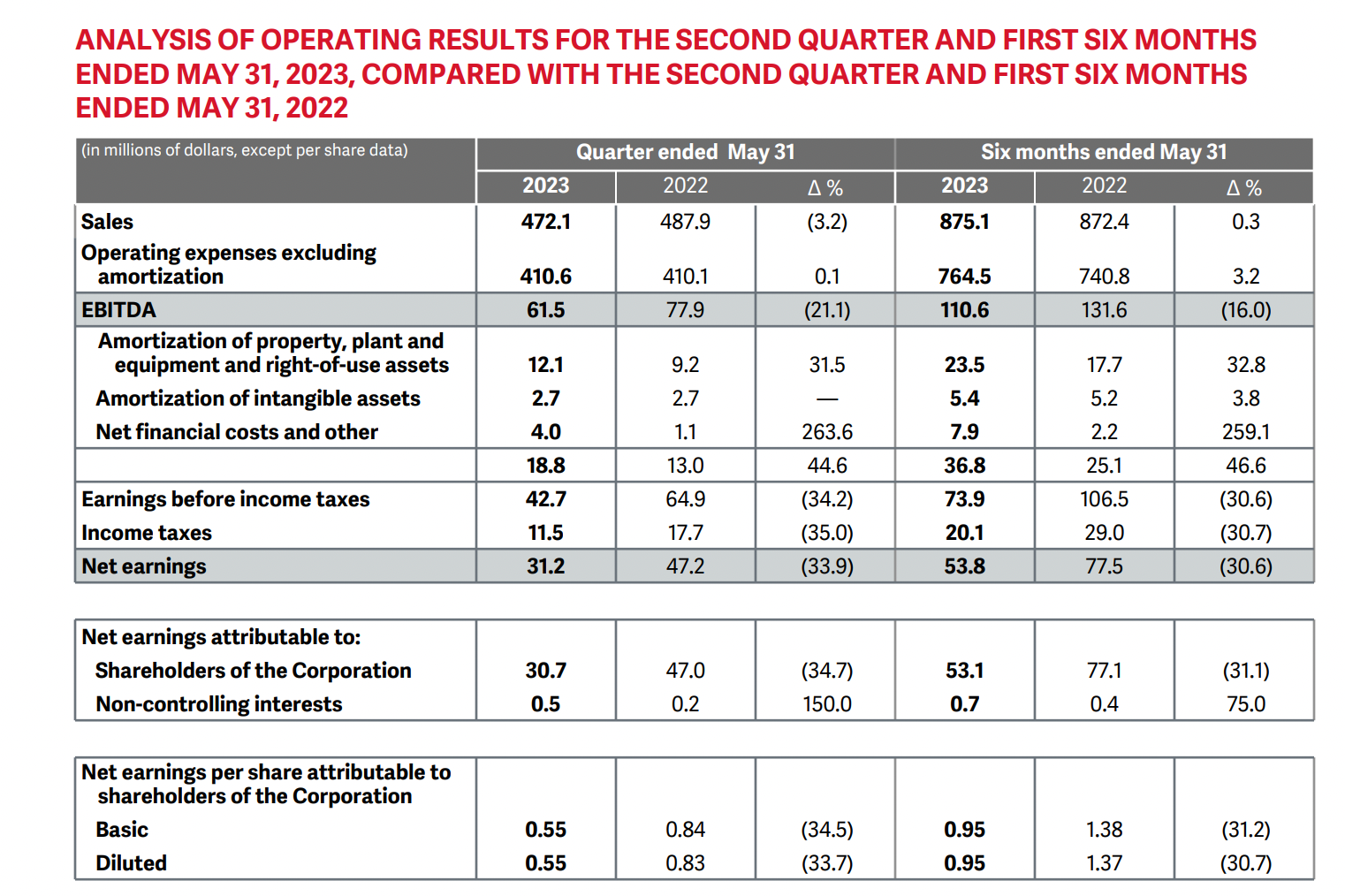

Earnings

The following chart shows the full result including the earnings

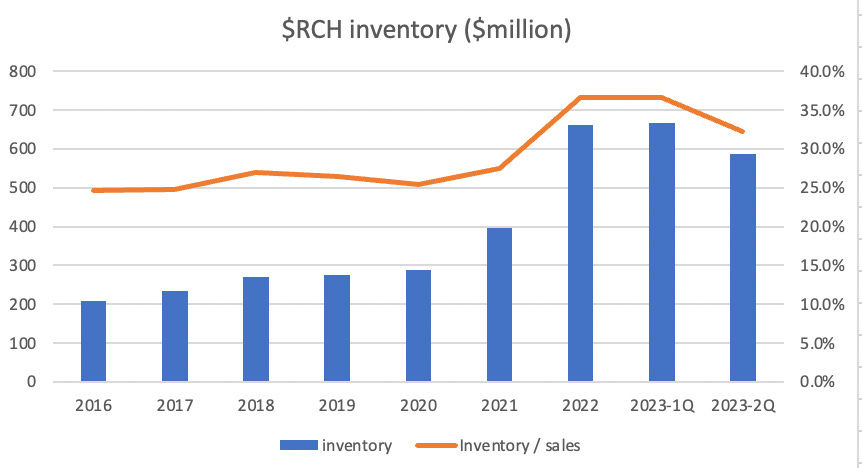

Inventory

We also got a progress status on the inventory reduction. At the last call, they mentioned that they wanted to reduce inventory by 60-80 million. The inventory now stands at 587 million down 80 million from 667 million from last quarter. The main effort of inventory reduction is probably completed.

They mentionned that next year, they will probably reduce inventory by another 50 million to be more in line with historical inventory figures.

The 80 million inventory reduction was very positive from a cash flow perspective. Cash flow from operating activities was 72 million in the last quarter.

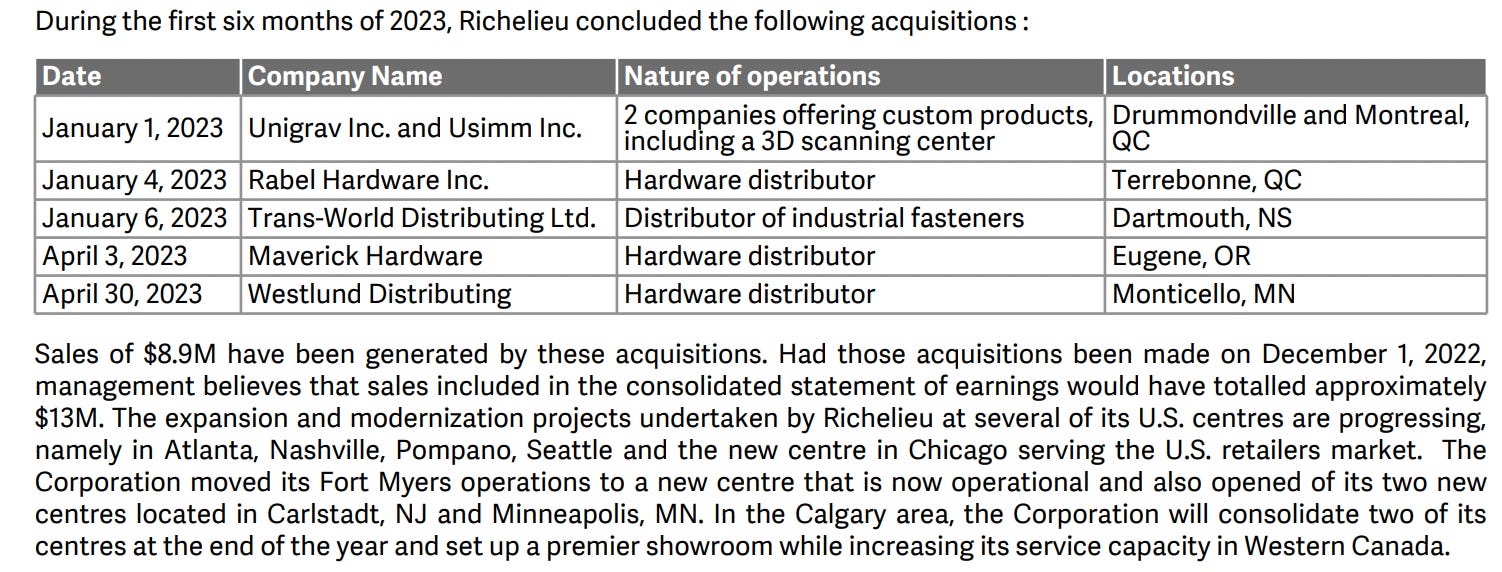

Acquisitions

Richelieu made 6 acquisitions during the first 6 months. 4 in Canada and 2 in USA. I was glad to see an acquisition in Oregon. Richelieu hardware is not strong in the West coast. They bought 2 companies involved in 3D printing. This is interesting.

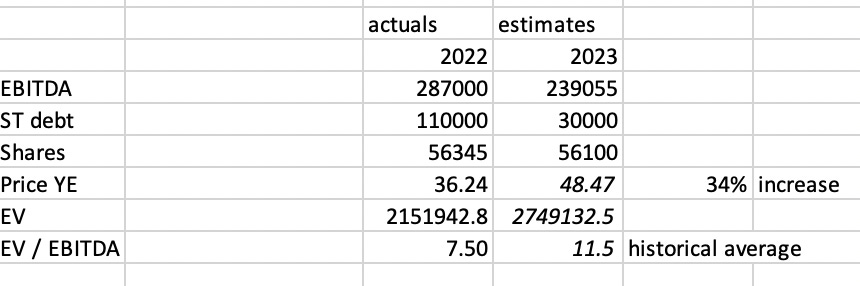

2023 Estimates

I revised a bit my estimates for 2023 with the following assumptions:

Increase sales by 2.5-3% from previous estimates to reflect strong sales in Q2

Reduce EBITDA margin to 13% overall for the year 2023 to align with recent management guidance.

In terms of fair value for 2023, based on projected EBITDA of 239 million, and return to historical EV/EBITDA of 11.5, my fair value is 48$.

Graphe of historical EV/EBITDA for the last 20 years can be found here:

https://wintergems.substack.com/p/part-3-richelieu-hardware-valuation

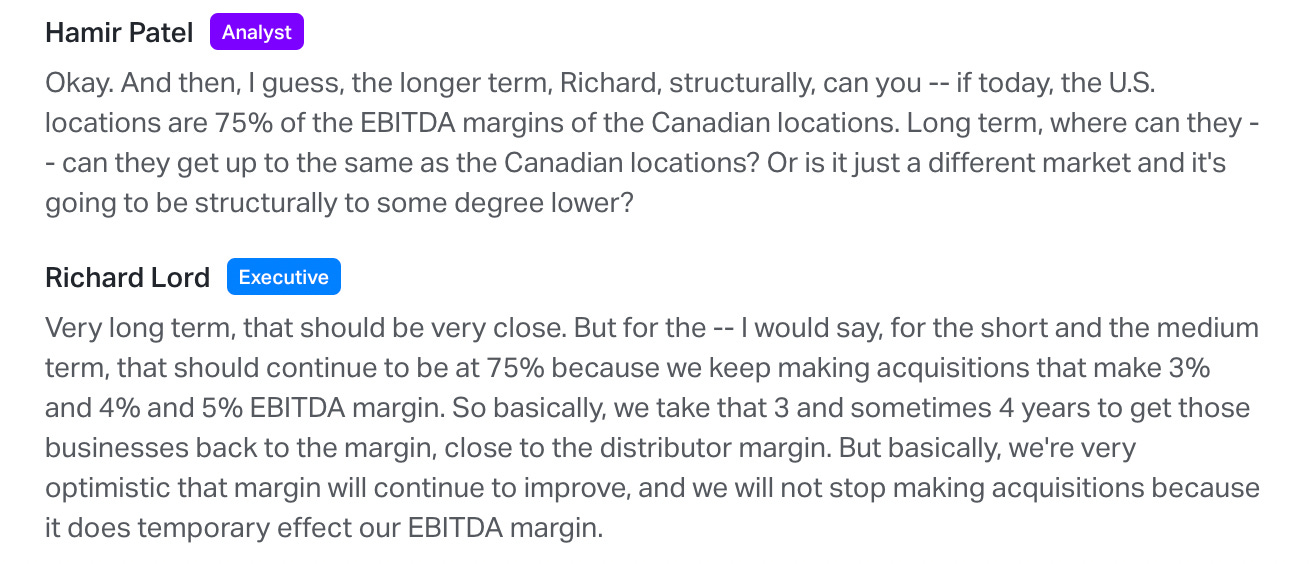

Nuggets of gold during the conference call

During the conference call there was some nuggets of gold:

Not all serial acquirer are equals. Buys a business with a 3-5% EBITDA margin and turns it into a 13-14% EBITDA margin.

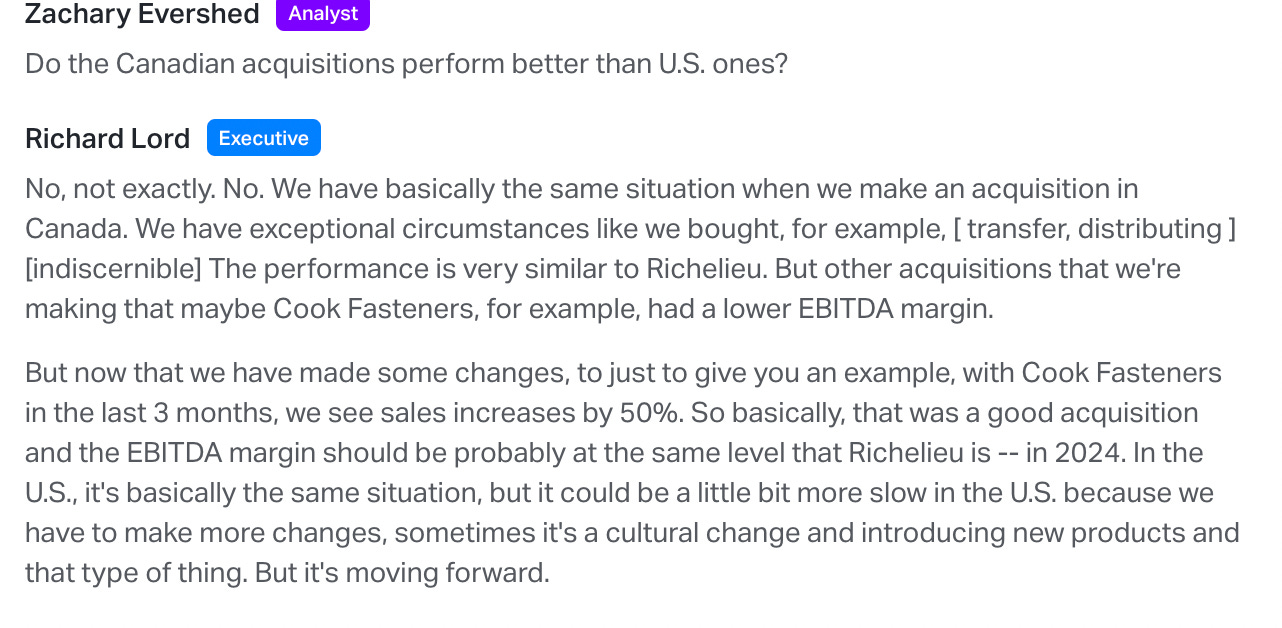

One specific example with Cook Fasteners:

Cheers!

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested

Thanks @govro - I really appreciate you sharing your thoughts!! A couple of things stood out to me and keen to hear how you think about this. 1) the rate of inorganic growth seems to have slowed and the acquisition multiple being paid is higher than historic levels - annualized sales using acquisitions for first half is $26m whereas historically annualized sales for full year has been around the $75m also paid sales multiple 0.8x relative to historic 0.4x - 0.6x. 2) I am surprised that you are anticipating revenue growth in Q3 as management have seen a 10% rev decline in June (from earnings call). 3) keen to hear also what you think is a reasonable normalized EBITDA margin over the longer term (management have recently reduced guidance to 13%-14% although i suspect as US gains scale this could approach 14%-15%) how do you think about this? And lastly do you know if management has set any targets for topline growth and maybe also specifically growth for US bussines? Keen to hear your thoughts and thanks again for sharing - very insightful as always!